IBM 2010 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2010 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

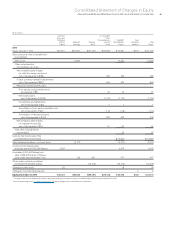

Notes to Consolidated Financial Statements

International Business Machines Corporation and Subsidiary Companies 69

Multiple-Deliverable Arrangements

The company enters into revenue arrangements that may consist

of multiple deliverables of its products and services based on

the needs of its clients. These arrangements may include any

combination of services, software, hardware and/or financing. For

example, a client may purchase a server that includes operating

system software. In addition, the arrangement may include post-

contract support for the software and a contract for post-warranty

maintenance service for the hardware. These types of arrange-

ments can also include financing provided by the company. These

arrangements consist of multiple deliverables, with the hardware

and software delivered in one reporting period and the software

support and hardware maintenance services delivered across

multiple reporting periods. In another example, a client may out-

source the running of its datacenter operations to the company

on a long-term, multiple-year basis and periodically purchase

servers and/or software products from the company to upgrade

or expand its facility. The outsourcing services are provided on a

continuous basis across multiple reporting periods and the hard-

ware and software products are delivered in one reporting period.

To the extent that a deliverable in a multiple-deliverable arrange-

ment is subject to specific guidance that deliverable is accounted

for in accordance with such specific guidance. Examples of such

arrangements may include leased hardware which is subject to

specific leasing guidance or software which is subject to specific

software revenue recognition guidance (see “Software” on page

70) on whether and/or how to separate multiple-deliverable

arrangements into separate units of accounting (separability) and

how to allocate the arrangement consideration among those

separate units of accounting (allocation). For all other deliverables

in multiple-deliverable arrangements, the guidance below is applied

for separability and allocation. A multiple-deliverable arrangement

is separated into more than one unit of accounting if the following

criteria are met:

• The delivered item(s) has value to the client on a stand-alone

basis; and

• If the arrangement includes a general right of return relative to

the delivered item(s), delivery or performance of the undelivered

item(s) is considered probable and substantially in the control

of the company.

If these criteria are not met, the arrangement is accounted for

as one unit of accounting which would result in revenue being

recognized ratably over the contract term or being deferred until the

earlier of when such criteria are met or when the last undelivered

element is delivered. If these criteria are met for each element and

there is a relative selling price for all units of accounting in an

arrangement, the arrangement consideration is allocated to the

separate units of accounting based on each unit’s relative selling

price. The following revenue policies are then applied to each unit

of accounting, as applicable.

Services

The company’s primary services offerings include information

technology (IT) datacenter and business process outsourcing,

application management services, consulting and systems integra-

tion, technology infrastructure and system maintenance, Web

hosting and the design and development of complex IT systems

to a client’s specifications (design and build). These services are

provided on a time-and-material basis, as a fixed-price contract

or as a fixed-price per measure of output contract and the contract

terms range from less than one year to over 10 years.

Revenue from IT datacenter and business process outsourcing

contracts is recognized in the period the services are provided

using either an objective measure of output or on a straight-line

basis over the term of the contract. Under the output method, the

amount of revenue recognized is based on the services delivered

in the period.

Revenue from application management services, technology

infrastructure and system maintenance and Web hosting contracts

is recognized on a straight-line basis over the terms of the contracts.

Revenue from time-and-material contracts is recognized as labor

hours are delivered and direct expenses are incurred. Revenue

related to extended warranty and product maintenance contracts

is recognized on a straight-line basis over the delivery period.

Revenue from fixed-price design and build contracts is recog-

nized under the percentage-of-completion (POC) method. Under

the POC method, revenue is recognized based on the labor costs

incurred to date as a percentage of the total estimated labor costs

to fulfill the contract. If circumstances arise that change the original

estimates of revenues, costs, or extent of progress toward comple-

tion, revisions to the estimates are made. These revisions may

result in increases or decreases in estimated revenues or costs,

and such revisions are reflected in income in the period in which

the circumstances that gave rise to the revision become known

by management.

The company performs ongoing profitability analyses of its

services contracts accounted for under the POC method in order

to determine whether the latest estimates of revenue, costs and

profits require updating. If at any time these estimates indicate that

the contract will be unprofitable, the entire estimated loss for the

remainder of the contract is recorded immediately. For non-POC

method service contracts, losses are recorded as incurred.

In some services contracts, the company bills the client prior

to recognizing revenue from performing the services. Deferred

income of $7,195 million and $7,066 million at December 31, 2010

and 2009, respectively, is included in the Consolidated Statement

of Financial Position. In other services contracts, the company

performs the services prior to billing the client. Unbilled accounts

receivable of $2,244 million and $2,020 million at December 31,

2010 and 2009, respectively, is included in notes and accounts

receivable-trade in the Consolidated Statement of Financial Position.

Billings usually occur in the month after the company performs

the services or in accordance with specific contractual provisions.

Unbilled receivables are expected to be billed within four months.