Capital One 2007 Annual Report Download - page 93

Download and view the complete annual report

Please find page 93 of the 2007 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

|

|

71

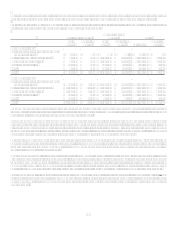

Charge-offs and Delinquencies

Commercial and small business loans are considered past due or delinquent based on contractual terms. Principal amounts charge off

when amounts are deemed uncollectible and interest is reversed and charged against income when the loans are placed on nonaccrual

status.

Credit card loans charge off at 180 days past the statement cycle date and other consumer loans generally charge-off at 120 days past

due or upon repossession of collateral. The entire balance of an account is contractually delinquent if the minimum payment is not

received by the specified due date on the customers billing statement. Bankruptcies charge off within 30 days of notification and

deceased accounts charge off within 60 days of notification. Fraudulent amounts are charged to non-interest expense after a 60 day

investigation period.

Net charge-offs represent principal losses net of current period principal recoveries. Principal losses exclude accrued and unpaid

interest income and fees and fraud losses. Interest income and fees accrued and not collected are reversed when the loan charges off or

when placed in nonaccrual status. Costs to recover previously charged-off loans are recorded as collection expenses in other non-

interest expense.

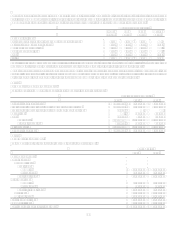

Allowance for Loan and Lease Losses

The allowance for loan and lease losses is maintained at the amount estimated to be sufficient to absorb probable principal losses, net

of principal recoveries (including recovery of collateral), inherent in the existing reported loan portfolios. The provision for loan losses

is the periodic cost of maintaining an adequate allowance. The amount of allowance necessary is based on distinct allowance

methodologies depending on the type of loans which include specifically identified criticized loans, migration analysis, forward loss

curves and historical loss trends. In evaluating the sufficiency of the allowance for loan and lease losses, management takes into

consideration the following factors: recent trends in delinquencies and charge-offs including bankrupt, deceased and recovered

amounts; forecasting uncertainties and size of credit risks; the degree of risk inherent in the composition of the loan portfolio;

economic conditions; legal and regulatory guidance; credit evaluations and underwriting policies; seasonality; and the value of

collateral supporting the loans. To the extent credit experience is not indicative of future performance or other assumptions used by

management do not prevail, loss experience could differ significantly, resulting in either higher or lower future provision for loan and

lease losses, as applicable. The evaluation process for determining the adequacy of the allowance for loan losses and the periodic

provisioning for estimated losses is undertaken on a quarterly basis, but may increase in frequency should conditions arise that would

require the Companys prompt attention. Conditions giving rise to such action are business combinations or other acquisitions or

dispositions of large quantities of loans, dispositions of non-performing and marginally performing loans by bulk sale or any

development which may indicate an adverse trend.

Commercial and small business loans are considered to be impaired in accordance with the provisions of Statement of Financial

Accounting Standards No. 114, Accounting by Creditors for Impairment of a Loan, (SFAS 114) when it is probable that all amounts

due in accordance with the contractual terms will not be collected. Specific allowances are determined in accordance with SFAS 114.

Impairment is measured based on the present value of the loans expected cash flows, the loans observable market price or the fair

value of the loans collateral.

For purposes of determining impairment, consumer loans are collectively evaluated as they are considered to be comprised of large

groups of smaller-balance homogeneous loans and therefore are not individually evaluated for impairment under the provisions of

SFAS 114.

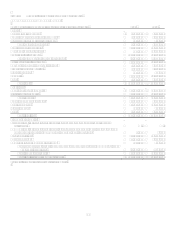

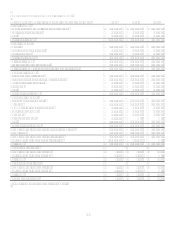

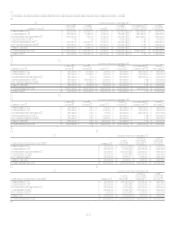

As of December 31, 2007 and 2006, the balance in the allowance for loan and lease losses was $3.0 billion and $2.2 billion,

respectively. See Note 6 for additional detail.

Premises and Equipment

Premises and equipment are stated at cost less accumulated depreciation and amortization. The Company capitalizes direct costs

(including external costs for purchased software, contractors, consultants and internal staff costs) for internally developed software

projects that have been identified as being in the application development stage. Depreciation and amortization expenses are computed

generally by the straight-line method over the estimated useful lives of the assets. Useful lives for premises and equipment are as

follows: buildings and improvements5-39 years; furniture and equipment3-10 years; computers and software3-5 years. See

Note 8 for additional detail.

Goodwill and Other Intangible Assets

The Company performs annual impairment tests on goodwill in accordance with Statement of Financial Accounting Standards

No. 142, Goodwill and Other Intangible Assets (SFAS 142). As of December 31, 2007 and 2006, goodwill of $12.8 billion and

$13.6 billion, respectively, was included in the Consolidated Balance Sheet. See Note 18 for additional detail.