Capital One 2007 Annual Report Download - page 12

Download and view the complete annual report

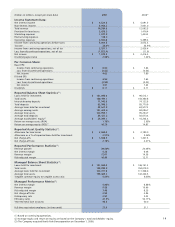

Please find page 12 of the 2007 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

|

|

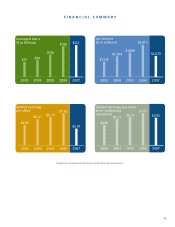

Our national small business franchise is one of the leading providers of small business

credit cards, lines of credit, and Small Business Administration loans in the United States.

Small business continued to perform well in 2007, with outstandings growth of $760

million, solid credit performance, and credit card purchase volumes up 7 percent over

2006. Our installment lending business, which includes our directly marketed installment

loans and our point-of-sale healthcare finance business, delivered profitable growth in

2007. Capital One Home Loans, our direct-to-consumer home loans business, continued

to provide a brand-defining customer experience, even as it shifted its business model

to originate and sell mostly conforming first mortgages. COHL also became the mortgage

origination platform for our bank branches, building scale and volume in footprint

which helps resiliency and improves operating leverage.

The credit environment in the UK has stabilized, and our UK credit card business is

starting to rebound. Canada arguably emerged as the Most Valuable Player in the GFS

portfolio this year, effectively competing against the entrenched, incumbent banks in

the Canadian market with great rates and compelling rewards offers.

GFS delivered strong profits, growth, and risk-adjusted returns on capital in 2007.

With investments in marketing, people, and infrastructure, our GFS businesses are

poised to carry strong momentum into 2008 and beyond.

We Are Becoming “One Bank”

2007 was a big year for the bank. Our transformative banking acquisitions have

diversified our company, insulated us from capital markets volatility, and reduced funding

costs. Our bank provides us with much more than risk mitigation. It has enormous

potential to create value. We now are the fourteenth largest bank in the United States,

with 742 branches and 1,288 ATM locations across our banking footprint. Banking is the

second largest income producer for the company, generating $574 million in net income

in 2007 and returns on allocated capital of 22 percent. And we have scale positions in

some of the most attractive and resilient banking markets in the United States.

During 2007, we assembled a new senior management team to build a winning retail

and commercial bank in all of our markets in New York, New Jersey, Connecticut,

Louisiana, and Texas. The team is led by Lynn Pike as president of our banking division.

Lynn brings a wealth of banking experience to our company from her years at Bank of

America (and Wells Fargo and Fleet Boston before that) and a great eye for talent. Since

10