ICICI Bank 2014 Annual Report Download - page 84

Download and view the complete annual report

Please find page 84 of the 2014 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

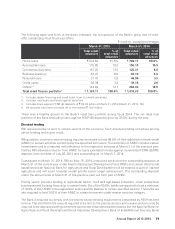

Management’s Discussion & Analysis

82

Management’s Discussion & Analysis

The Bank’s aggregate investments in security receipts issued by asset reconstruction companies were

` 8.84 billion at March 31, 2014 as compared to ` 11.47 billion at March 31, 2013.

During fiscal 2014, the Bank restructured standard loans of 35 corporate and 710 agri borrowers (under a

drought relief restructuring scheme) amounting to ` 57.55 billion (outstanding loans to these borrowers

at March 31, 2014: ` 62.31 billion) as compared to 23 borrowers amounting to ` 16.78 billion during fiscal

2013 (outstanding loans to these borrowers at March 31, 2013: ` 18.14 billion). Net outstanding loans to

borrowers whose facilities have been restructured increased from ` 53.15 billion at March 31, 2013 to

` 105.58 billion at March 31, 2014.

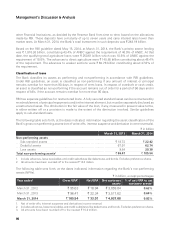

Segment information

RBI in its guidelines on “segmental reporting” has stipulated specified business segments and their

definitions, for the purposes of public disclosures on business information for banks in India.

The standalone segmental report for fiscal 2014, based on the segments identified and defined by RBI,

has been presented as follows:

• Retail Banking includes exposures of the Bank, which satisfy the four qualifying criteria of ‘regulatory

retail portfolio’ as stipulated by RBI guidelines on the Basel II framework.

• Wholesale Banking includes all advances to trusts, partnership firms, companies and statutory bodies,

by the Bank which are not included in the Retail Banking segment, as per RBI guidelines for the Bank.

• Treasury includes the entire investment portfolio of the Bank.

• Other Banking includes leasing operations and other items not attributable to any particular business

segment of the Bank.

Framework for transfer pricing

All liabilities are transfer priced to a central treasury unit, which pools all funds and lends to the business

units at appropriate rates based on the relevant maturity of assets being funded after adjusting for

regulatory reserve requirement and directed lending requirements.

Retail banking segment

The profit before tax of the retail banking segment increased from ` 9.55 billion in fiscal 2013 to ` 18.30

billion in fiscal 2014 primarily due to increase in net interest income and non-interest income, offset, in

part, by increase in non-interest expenses.

Net interest income increased by 37.2% from ` 42.09 billion in fiscal 2013 to ` 57.73 billion in fiscal 2014

primarily due to growth in loan portfolio and increase in average current account and savings account

deposits of the retail banking segment.

Non-interest income increased by 19.0% from ` 30.42 billion in fiscal 2013 to ` 36.21 billion in fiscal 2014,

primarily due to higher level lending linked fees, third party product distribution fees, fees from credit card

portfolio and transaction banking fees.

Non-interest expenses increased by 21.1% from ` 63.22 billion in fiscal 2013 to ` 76.58 billion in fiscal

2014, primarily due to increase in retail lending business and increase in operating expenses due to

expansion in branch network.

In fiscal 2014, there was write-back of ` 0.94 billion compared to write-back of ` 0.24 billion in fiscal 2013

primarily due to write-back/lower provisions for loan losses in the retail asset portfolio.