ICICI Bank 2014 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2014 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

Annual Report 2013-2014 61

Indian equity markets improved during fiscal 2014, though there were periods of high volatility during the

year. The benchmark equity index, the BSE Sensex, increased by 18.8% during fiscal 2014, moving from

18,836 at March 31, 2013 to a low of 17,906 on August 21, 2013 and subsequently rising to 22,386 at

March 31, 2014. As per the Securities and Exchange Board of India, foreign institutional investment (FII)

flows were significantly lower in fiscal 2014 with net inflows of around US$ 9.07 billion compared to net

inflows of US$ 27.58 billion during fiscal 2013. There were net inflows of US$ 13.69 billion in equity and

net outflows of US$ 4.62 billion in debt markets during fiscal 2014. Foreign direct investments improved

marginally to US$ 20.98 billion and external commercial borrowings to US$ 5.81 billion during the first

nine months of fiscal 2014, compared to US$ 19.78 billion and US$ 4.47 billion, respectively, during the

corresponding period of fiscal 2013.

Non-food credit growth remained subdued during fiscal 2014, with a growth of 14.5% year-on-year at

March 21, 2014 compared to 13.9% at March 22, 2013. Based on sector-wise credit data available as of

February 21, 2014, year-on-year growth in credit to industry was 13.2% and to the services sector was

17.1%. Credit to the infrastructure sector grew by 13.1% compared to 19.7% at February 22, 2013. Retail

loan growth increased to 16.5% from 14.6%. Deposit growth was 14.6% year-on-year at March 21, 2014,

compared to 14.2% growth at March 22, 2013. Demand deposit growth improved to 8.8% year-on-year

at March 21, 2014, compared to 5.9% at March 22, 2013.

First year retail premium underwritten in the life insurance sector (on weighted received premium basis)

was ` 454.29 billion in fiscal 2014 as compared to ` 470.19 billion in fiscal 2013. Gross premium of

the non-life insurance sector (excluding specialised insurance institutions) grew by 12.7% to ` 728.53

billion during fiscal 2014 from ` 646.53 billion during fiscal 2013. The average assets under management

of mutual funds increased by 10.8% from ` 8,166.57 billion in March 2013 to ` 9,045.49 billion in

March 2014.

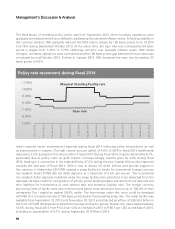

Banking regulation underwent several changes during fiscal 2014 with several more measures proposed

to be implemented going forward. In the second quarter monetary policy review announced on October

29, 2013, RBI outlined five areas that would be the focus for developmental measures to be announced

in the short to medium term. These include the following:

• Strengthening and clarifying the monetary policy framework. In this regard, the recommendations

of the Urjit Patel Committee to Revise and Strengthen Monetary Policy Framework were considered

and implementation was initiated during fiscal 2014. Key proposals include adopting the consumer

price index (CPI) as the key inflation measure for monetary policy action, keeping the economy

on a disinflationary glide path with a target of 8.0% CPI inflation by January 2015 and 6.0% by

January 2016, transition to a bi-monthly monetary policy cycle, and progressive reduction in banking

system access to overnight liquidity under the LAF and corresponding increase in access to liquidity

through term repos.

• Strengthening the banking structure through entry of new banks, branch expansion, encouraging new

varieties of banks, and clarifying an organisational framework for foreign banks. In this regard, two

new banks were given in-principle licenses during fiscal 2014.

• Broadening and deepening financial markets and increasing their liquidity and resilience.

• Expanding access to finance to small and medium enterprises, the unorganised sector, the poor and

the remote underserved areas. RBI appointed a Committee on Comprehensive Financial Services for

Small Businesses and Low-Income Households which submitted its recommendations in March 2014

and has proposed, among other things, allowing setting up of specialised payments and wholesale

banks, and a new framework for priority sector lending.

• Strengthening real and financial restructuring and debt recovery from corporates and improving the

system’s ability to deal with distress.