ICICI Bank 2014 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2014 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

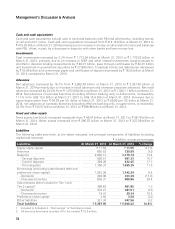

Management’s Discussion & Analysis

62

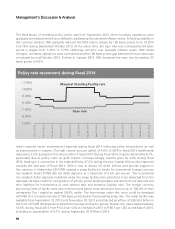

Some important regulatory developments impacting the banking sector during fiscal 2014 were:

• In May 2013, RBI issued guidelines on restructuring of advances. As per the guidelines, loans that are

restructured (other than due to delay in project completion up to a specified period in the infrastructure

sector and non-infrastructure sector) from April 1, 2015 onwards would be classified as non-performing.

General provision on standard accounts restructured after June 1, 2013 was increased to 5.0%. The

general provision required on standard accounts restructured prior to that date has been increased to

3.5% from March 31, 2014, and would further increase to 4.25% from March 31, 2015 and 5.0% from

March 31, 2016;

• In June 2013, prudential norms pertaining to risk weights, provisioning and loan-to-value ratio for

individual housing loans were revised. Accordingly, individual housing loans of up to ` 7.5 million now

attract risk weight of 50.0% with standard asset provisioning of 0.4%. For individual housing loans of

above ` 7.5 million, the loan-to-value ratio was set at 75.0% and risk weight was lowered from 125.0%

to 75.0%;

• A new category of commercial real estate referred to as commercial real estate - residential housing

was created within the commercial real estate category. Commercial real estate - residential housing

attracts risk weight of 75.0% and standard asset provisioning of 0.75%. Commercial real estate

excluding residential housing has risk weight of 100.0% and standard asset provisioning of 1.0%;

• In August 2013, RBI released a discussion paper on the structure of the banking system in India.

The paper envisages changes in the structure of the banking system with a view to address specific

issues such as enhancing competition, financing higher growth, providing specialised services,

and expanding financial inclusion. The paper proposes to allow different types of banks along with

differentiated licensing for niche services. It also proposes to have continuous licensing for entry of

new banks as against the current system of block licensing. The paper also favors migration from the

current bank-led universal banking model to a financial holding company structure;

• In the first half of fiscal 2014, RBI announced measures with regard to gold imports and financing

of gold during the six months ended September 30, 2013. RBI restricted banks’ import of gold on

consignment basis to only meet the needs of exporters of gold jewellery. Further, import of gold under

all categories was mandated to be only on 100.0% cash margin basis. Advances against the security

of gold coins per customer were restricted to gold coins weighing up to 50 grams;

• In October 2013, RBI liberalised the branch authorisation policy, doing away with the requirement of

approvals to open branches in metropolitan regions. However, the total number of branches opened

in Tier 1 centers during a year cannot exceed the total number of branches opened in Tier 2 to Tier 6

centers during a year. It was also specified that at least 25.0% of total new branches opened in a year

should be in unbanked rural Tier 5 and Tier 6 centers;

• In November 2013, RBI decided to include incremental credit made after November 13, 2013, including

export credit, to medium enterprises as part of priority sector advances. The facility was available up

to March 31, 2014;

• In December 2013, RBI mandated banks to create deferred tax liability, or DTL, on Special Reserve,

with the DTL up to March 31, 2013 permitted to be directly adjusted through reserves and DTL from

the financial year ending March 31, 2014 onwards to be charged through the profit and loss account;

• In December 2013, RBI issued a draft framework on capital surcharges for domestic systemically

important banks (D-SIBs). The higher capital requirements applicable to D-SIBs would be implemented

in a phased manner from April 2016 to April 2019. D-SIBs would be required to have additional Common

Equity Tier 1 capital ranging from 0.2% to 0.8 % of risk weighted assets;

Management’s Discussion & Analysis