ICICI Bank 2014 Annual Report Download - page 158

Download and view the complete annual report

Please find page 158 of the 2014 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

F70

SIGNIFICANT ACCOUNTING POLICIES

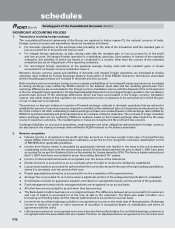

1. Transactions involving foreign exchange

The consolidated financial statements of the Group are reported in Indian rupees (`), the national currency of India.

Foreign currency income and expenditure items are translated as follows:

•For domestic operations, at the exchange rates prevailing on the date of the transaction with the resultant gain or

loss accounted for in the profit and loss account.

•For integral foreign operations, at daily closing rates with the resultant gain or loss accounted for in the profit

and loss account. An integral foreign operation is a subsidiary, associate, joint venture or branch of the reporting

enterprise, the activities of which are based or conducted in a country other than the country of the reporting

enterprise but are an integral part of the reporting enterprise.

•For non-integral foreign operations, at the quarterly average closing rates with the resultant gains or losses

accounted for as foreign currency translation reserve.

Monetary foreign currency assets and liabilities of domestic and integral foreign operations are translated at closing

exchange rates notified by Foreign Exchange Dealers’ Association of India (FEDAI) relevant to the balance sheet date

and the resulting gains/losses are included in the profit and loss account.

Both monetary and non-monetary foreign currency assets and liabilities of non-integral foreign operations are translated

at closing exchange rates notified by FEDAI relevant to the balance sheet date and the resulting gains/losses from

exchange differences are accumulated in the foreign currency translation reserve until the disposal of the net investment

in the non-integral foreign operations. On the disposal/partial disposal of a non-integral foreign operation, the cumulative/

proportionate amount of the exchange differences which has been accumulated in the foreign currency translation

reserve and which relates to that operation are recognised as income or expenses in the same period in which the gain

or loss on disposal is recognised.

The premium or discount arising on inception of forward exchange contracts in domestic operations that are entered to

establish the amount of reporting currency required or available at the settlement date of a transaction is amortised over the

life of the contract. All other outstanding forward exchange contracts are revalued based on the exchange rates notified by

FEDAI for specified maturities and at interpolated rates for contracts of interim maturities. The contracts of longer maturities

where exchange rates are not notified by FEDAI are revalued, based on the forward exchange rates implied by the swap

curves in respective currencies. The resultant gains or losses are recognised in the profit and loss account.

Contingent liabilities on account of guarantees, endorsements and other obligations denominated in foreign currency

are disclosed at the closing exchange rates notified by FEDAI relevant to the balance sheet date.

2. Revenue recognition

zInterest income is recognised in the profit and loss account as it accrues except in the case of non-performing

assets (NPAs) where it is recognised upon realisation, as per the income recognition and asset classification norms

of RBI/NHB/other applicable guidelines.

zIncome from finance leases is calculated by applying the interest rate implicit in the lease to the net investment

outstanding on the lease over the primary lease period. Finance leases entered into prior to April 1, 2001 have been

accounted for as per the Guidance Note on Accounting for Leases issued by ICAI. The finance leases entered post

April 1, 2001 have been accounted for as per Accounting Standard 19 - Leases.

zIncome on discounted instruments is recognised over the tenure of the instrument.

zDividend income is accounted on an accrual basis when the right to receive the dividend is established.

zLoan processing fee is accounted for upfront when it becomes due except in the case of foreign banking subsidiaries,

where it is amortised over the period of the loan.

zProject appraisal/structuring fee is accounted for on the completion of the agreed service.

zArranger fee is accounted for as income when a significant portion of the arrangement/syndication is completed.

zCommission received on guarantees issued is amortised on a straight-line basis over the period of the guarantee.

zFund management and portfolio management fees are recognised on an accrual basis.

zAll other fees are accounted for as and when they become due.

zThe Bank deals in bullion business on a consignment basis. The difference between price recovered from customers

and cost of bullion is accounted for at the time of sale to the customers. The Bank also deals in bullion on a

borrowing and lending basis and the interest paid/received is accounted on accrual basis.

zIncome from securities brokerage activities is recognised as income on the trade date of the transaction. Brokerage

income in relation to public or other issuances of securities is recognised based on mobilisation and terms of

agreement with the client.

zLife insurance premium is recognised as income when due from policyholders. For unit linked business, premium is

recognised when the associated units are created. Premium on lapsed policies is recognised as income when such

forming part of the Consolidated Accounts (Contd.)

schedules