ICICI Bank 2014 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2014 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

Annual Report 2013-2014 63

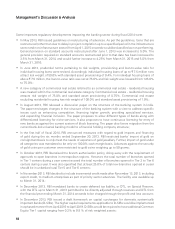

• In December 2013, RBI issued draft guidelines on implementation of counter-cyclical capital buffer

(CCCB). According to the guidelines, the CCCB would range from 0% to 2.5% of risk weighted assets

of the bank. The variation in the credit-to-GDP ratio from its long-term trend would be a key parameter

for identifying business cycles

• In December 2013, RBI issued updated guidelines on stress testing. As per the guidelines, banks would

have to carry out stress tests for credit risk and market risk to assess their ability to withstand shocks.

Banks should be classified into three categories based on size of risk weighted assets. Complex and

severe stress testing would be carried out by banks falling under Group A with risk weighted assets

of more than ` 2,000 billion

• In January 2014, RBI issued a Framework for Revitalising Distressed Assets in the Economy. The

framework outlines an action plan for early identification of problem cases, timely restructuring of

accounts which are considered to be viable, and taking prompt steps by banks for recovery or sale

of unviable accounts. Accounts have to be categorised into ‘special mention accounts’ based on

certain criteria. Formation of Joint Lenders’ Forum (JLF) would be mandatory which would formulate

a corrective action plan. In case the JLF fails to agree on an action plan, it would result in accelerated

provisioning. An independent evaluation of large value restructuring with a focus on viability and fair

sharing of gains and losses between promoters and creditors have been mandated. The framework

is effective from April 1, 2014

• In January 2014, RBI introduced incremental provisioning and capital requirements for banks’ exposure

to entities with unhedged foreign currency exposure. Banks are required to make incremental

provisioning (over and above standard asset provisioning) that would range between 0-80 basis points

based on the likely loss due to exchange rate movement as a percentage of earnings before interest

and depreciation (EBID). An additional risk weight of 25% would be applicable if the expected loss

exceeds 75% of EBID, while for losses less than 75% there is no additional capital requirement. This

guideline is effective from April 1, 2014

• In February 2014, RBI allowed banks to utilise up to 33% of counter-cyclical provisioning buffer/ floating

provisions held by them as on March 31, 2013, for making specific provisions for non-performing

assets. This would be over and above the utilisation for the purpose of making accelerated/additional

provisions as proposed in the framework for Revitalising Distressed Assets in the Economy

• In February 2014, RBI issued guidelines indicating limits on intra-group transactions and exposures

for banks’ transactions and exposures to the entities belonging to the bank’s own group. RBI

has prescribed a single group entity exposure limit of 5.0% of paid-up capital and reserves for

non-financial companies and 10.0% in case of regulated financial entities. Aggregate group exposure

cannot exceed 20.0% of paid up capital and reserves

• In March 2014, RBI released a notification amending the Basel III implementation schedule. The

introduction of capital conservation buffer (CCB) was deferred by a year to March 31, 2016, and full

implementation of Basel III capital regulations would be by March 31, 2019 from the earlier schedule

of March 31, 2018. Additional Tier-1 (AT1) capital instruments issued before March 31, 2019 will have

two specified triggers: 1) a lower pre-specified trigger at Common Equity Tier 1 (CET1) of 5.5% of risk

weighted assets will apply before March 31, 2019; 2) trigger would be raised to CET1 of 6.125% of

risk weighted assets (RWA) on or after March 31, 2019. Going forward, banks may issue AT1 capital

instruments with conversion / permanent write-down features only. Similarly, with regard to write-off

feature at point of non-viability (PONV) trigger, all non-equity capital instruments will have permanent

write-off feature only