The Hartford 2007 Annual Report Download - page 22

Download and view the complete annual report

Please find page 22 of the 2007 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

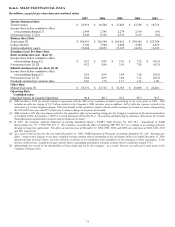

22

cause significant volatility in global financial markets, disruptions to commerce and reduced economic activity. These consequences

could have an adverse effect on the value of the assets in our investment portfolio as well as those in our separate accounts. The

continued threat of terrorism also could result in increased reinsurance prices and potentially cause us to retain more risk than we

otherwise would retain if we were able to obtain reinsurance at lower prices. Terrorist attacks also could disrupt our operations centers

in the U.S. or abroad. As a result, it is possible that any, or a combination of all, of these factors may have a material adverse effect on

our business, consolidated operating results, financial condition and liquidity.

We may incur losses due to our reinsurers’ unwillingness or inability to meet their obligations under reinsurance contracts and the

availability, pricing and adequacy of reinsurance may not be sufficient to protect us against losses.

As an insurer, we frequently seek to reduce the losses that may arise from catastrophes or mortality, or other events that can cause

unfavorable results of operations, through reinsurance. Under these reinsurance arrangements, other insurers assume a portion of our

losses and related expenses; however, we remain liable as the direct insurer on all risks reinsured. Consequently, ceded reinsurance

arrangements do not eliminate our obligation to pay claims, and we are subject to our reinsurers’ credit risk with respect to our ability to

recover amounts due from them. Although we evaluate periodically the financial condition of our reinsurers to minimize our exposure

to significant losses from reinsurer insolvencies, our reinsurers may become financially unsound or choose to dispute their contractual

obligations by the time their financial obligations become due. The inability or unwillingness of any reinsurer to meet its financial

obligations to us could negatively affect our consolidated operating results. In addition, market conditions beyond our control

determine the availability and cost of the reinsurance we are able to purchase. Historically, reinsurance pricing has changed

significantly from time to time. No assurances can be made that reinsurance will remain continuously available to us to the same extent

and on the same terms as are currently available. If we were unable to maintain our current level of reinsurance or purchase new

reinsurance protection in amounts that we consider sufficient and at prices that we consider acceptable, we would have to either accept

an increase in our net liability exposure, reduce the amount of business we write, or develop other alternatives to reinsurance.

We are exposed to significant financial and capital markets risk, including changes in interest rates, credit spreads, equity prices, and

foreign exchange rates which may adversely affect our results of operations, financial condition or liquidity.

We are exposed to significant financial and capital markets risk, including changes in interest rates, credit spreads, equity prices and

foreign currency exchange rates. Our exposure to interest rate risk relates primarily to the market price and cash flow variability

associated with changes in interest rates. A rise in interest rates will increase the net unrealized loss position of our investment

portfolio and, if long-term interest rates rise dramatically within a six to twelve month time period, certain of our Life businesses may

be exposed to disintermediation risk. Disintermediation risk refers to the risk that our policyholders may surrender their contracts in a

rising interest rate environment, requiring us to liquidate assets in an unrealized loss position. Due to the long-term nature of the

liabilities associated with certain of our Life businesses, such as structured settlements and guaranteed benefits on variable annuities,

sustained declines in long term interest rates may subject us to reinvestment risks and increased hedging costs. Our exposure to credit

spreads primarily relates to market price and cash flow variability associated with changes in credit spreads. A widening of credit

spreads will increase the net unrealized loss position of the investment portfolio, will increase losses associated with credit based non-

qualifying derivatives where the Company assumes credit exposure, and, if issuer credit spreads increase significantly or for an

extended period of time, would likely result in higher other-than-temporary impairments. Credit spread tightening will reduce net

investment income associated with new purchases of fixed maturities. In addition, market volatility can make it difficult to value

certain of our securities if trading becomes less frequent. As such, valuations may include assumptions or estimates that may have

significant period to period changes which could have a material adverse effect on our consolidated results of operations or financial

condition.

Our primary exposure to equity risk relates to the potential for lower earnings associated with certain of our Life businesses, such as

variable annuities, where fee income is earned based upon the fair value of the assets under management. In addition, certain of our

Life products offer guaranteed benefits which increase our potential benefit exposure should equity markets decline. We are also

exposed to interest rate and equity risk based upon the discount rate and expected long-term rate of return assumptions associated with

our pension and other post-retirement benefit obligations. Sustained declines in long-term interest rates or equity returns likely would

have a negative effect on the funded status of these plans. Our primary foreign currency exchange risks are related to net income from

foreign operations, non–U.S. dollar denominated investments, investments in foreign subsidiaries, our yen-denominated individual

fixed annuity product, and certain guaranteed benefits associated with the Japan variable annuity. These risks relate to potential

decreases in value and income resulting from a strengthening or weakening in foreign exchange rates versus the U.S. dollar. In general,

the weakening of foreign currencies versus the U.S. dollar will unfavorably affect net income from foreign operations, the value of non-

U.S. dollar denominated investments, investments in foreign subsidiaries and realized gains or losses on the yen denominated

individual fixed annuity product. In comparison, a strengthening of the Japanese yen in comparison to the U.S. dollar and other

currencies may increase our exposure to the guarantee benefits associated with the Japan variable annuity. If significant, declines in

equity prices, changes in U.S. interest rates, changes in credit spreads and the strengthening or weakening of foreign currencies against

the U.S. dollar or in combination, could have a material adverse effect on our consolidated results of operations, financial condition or

liquidity.