The Hartford 2007 Annual Report Download - page 122

Download and view the complete annual report

Please find page 122 of the 2007 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

122

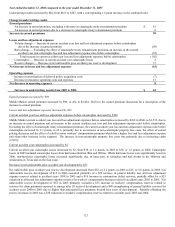

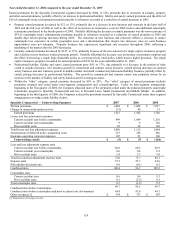

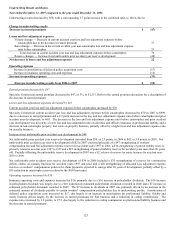

Operating expenses decreased by $8

The expense ratio decreased by 1.8 points, to 26.7, primarily due to a decrease in insurance operating costs and expenses. Insurance

operating costs decreased by $15, largely because of a $12 decrease in estimated Citizens’ assessments in 2006 compared to a $17

increase in Citizens assessments in 2005 and a reduction in estimated contingent commissions. Partially offsetting the improvement due

to changes in the Citizens’ assessments was an increase non-deferred operating expenses commensurate with the increase in earned

premium. Amortization of deferred policy acquisition costs increased by $7, due largely to the increase in earned premium.

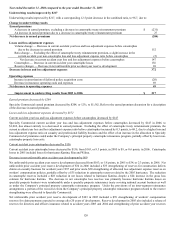

Outlook

Management expects written premium to be 1% to 4% lower in 2008 as the Company takes a disciplined approach to evaluating and

pricing risks in the face of declines in written pricing. Contributing to the expected decline in Middle Market written premium is the

effect of state-mandated rate reductions in workers' compensation and increased competition in specific geographic markets and lines.

For both workers’ compensation and commercial auto products, the Company will improve the sophistication of its pricing models,

resulting in an expanded underwriting appetite in selected industries and regions of the country. Targeting those agents and brokers

with the greatest opportunity for writing new profitable business, management plans to offer key agents added value through agency

service and sales support. Including supplemental commissions, the Company has increased commissions paid to agents and expects

that this will help it achieve its growth objectives in 2008.

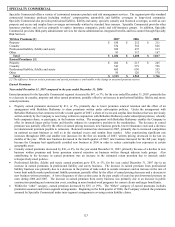

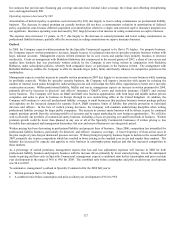

Written pricing has been affected by increased competition for new business as evidenced by 5% written pricing decreases in 2007.

Market conditions in the commercial lines industry continue to be soft with written pricing likely to decline further in 2008, more so on

the larger accounts. The Hartford’s new business has been declining due to the increased competition and written pricing decreases; in

2008, the Company will continue to focus on protecting its renewals.

Consistent with claims experience for the 2007 accident year, during 2008, management expects an increase in claim costs due to rising

claim cost severity as an expected increase in severity will likely more than offset the effect of an expected reduction in claim frequency.

Loss costs are expected to continue to increase across most lines of business in Middle Market, including on workers’ compensation

claims and on non-catastrophe property claims covered under property, marine and commercial auto policies. Based on anticipated

trends in earned pricing and loss costs, the combined ratio before catastrophes and prior accident year development is expected to be in

the range of 94.5 to 97.5 in 2008. The combined ratio before catastrophes and prior accident year development was 93.8 in 2007.

To summarize, management’ s outlook in Middle Market for the 2008 full year is:

• Written premium 1% to 4% lower

• A combined ratio before catastrophes and prior accident year development of 94.5 to 97.5