The Hartford 2007 Annual Report Download - page 203

Download and view the complete annual report

Please find page 203 of the 2007 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

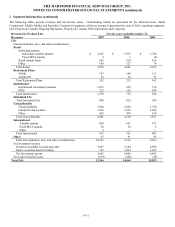

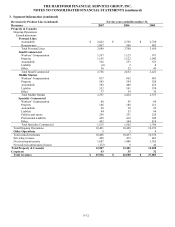

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (continued)

F-26

1. Basis of Presentation and Accounting Policies (continued)

Property & Casualty — The Hartford establishes property and casualty reserves to provide for the estimated costs of paying claims

under insurance policies written by the Company. These reserves include estimates for both claims that have been reported and those

that have been incurred but not reported, and include estimates of all losses and loss adjustment expenses associated with processing

and settling these claims. Estimating the ultimate cost of future losses and loss adjustment expenses is an uncertain and complex

process. This estimation process is based significantly on the assumption that past developments are an appropriate predictor of future

events, and involves a variety of actuarial techniques that analyze experience, trends and other relevant factors. The uncertainties

involved with the reserving process have become increasingly difficult due to a number of complex factors including social and

economic trends and changes in the concepts of legal liability and damage awards. Accordingly, final claim settlements may vary from

the present estimates, particularly when those payments may not occur until well into the future.

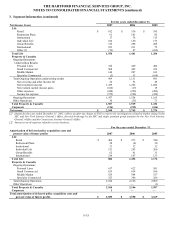

The Hartford regularly reviews the adequacy of its estimated losses and loss adjustment expense reserves by line of business within the

various reporting segments. Adjustments to previously established reserves are reflected in the operating results of the period in which

the adjustment is determined to be necessary. Such adjustments could possibly be significant, reflecting any variety of new and adverse

or favorable trends.

Most of the Company’ s property and casualty reserves are not discounted. However, certain liabilities for unpaid losses for

permanently disabled claimants have been discounted to present value using an average interest rate of 5.5% and 5.6% in 2007 and

2006, respectively. As of December 31, 2007 and 2006, such discounted reserves totaled $647 and $707, respectively (net of discounts

of $483 and $510, respectively). In addition, certain structured settlement contracts that fund loss run-offs for unrelated parties having

payment patterns that are fixed and determinable have been discounted to present value using an average interest rate of 5.5% in both

2007 and 2006. As of December 31, 2007 and 2006, such discounted reserves totaled $282 and $273, respectively (net of discounts of

$85 and $95, respectively). Accretion of discounts totaled $31, $32 and $30 in 2007, 2006 and 2005, respectively.

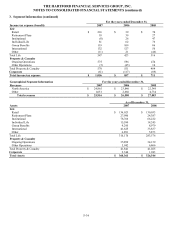

Other Policyholder Funds and Benefits Payable

The Company has classified its fixed and variable annuities, 401(k), certain governmental annuities, private placement life insurance

(“PPLI”), variable universal life insurance, universal life insurance and interest sensitive whole life insurance as universal life-type

contracts. The liability for universal life-type contracts is equal to the balance that accrues to the benefit of the policyholders as of the

financial statement date (commonly referred to as the account value), including credited interest, amounts that have been assessed to

compensate the Company for services to be performed over future periods, and any amounts previously assessed against policyholders

that are refundable on termination of the contract.

The Company has classified its institutional and governmental products, without life contingencies, including funding agreements,

certain structured settlements and guaranteed investment contracts, as investment contracts. The liability for investment contracts is

equal to the balance that accrues to the benefit of the contract holder as of the financial statement date, which includes the accumulation

of deposits plus credited interest, less withdrawals and amounts assessed through the financial statement date. Contract holder funds

include funding agreements held by Variable Interest Entities issuing medium-term notes.

Revenue Recognition

Life — For investment and universal life-type contracts, the amounts collected from policyholders are considered deposits and are not

included in revenue. Fee income for universal life-type contracts consists of policy charges for policy administration, cost of insurance

charges and surrender charges assessed against policyholders’ account balances and are recognized in the period in which services are

provided. For the Company’ s traditional life and group disability products premiums are recognized as revenue when due from

policyholders.

Property & Casualty — Property and casualty insurance premiums are earned on a pro rata basis over the lives of the policies and

include accruals for ultimate premium revenue anticipated under auditable and retrospectively rated policies. Unearned premiums

represent the premiums applicable to the unexpired terms of policies in-force. An estimated allowance for doubtful accounts is

recorded on the basis of periodic evaluations of balances due from insureds, management’ s experience and current economic

conditions. The allowance for doubtful accounts included in premiums receivable and agents’ balances in the consolidated balance

sheets was $126 and $114 as of December 31, 2007 and 2006, respectively. Other revenue consists primarily of revenues associated

with the Company’ s servicing businesses.

Foreign Currency Translation

Foreign currency translation gains and losses are reflected in stockholders’ equity as a component of accumulated other comprehensive

income. The Company’ s foreign subsidiaries’ balance sheet accounts are translated at the exchange rates in effect at each year end and

income statement accounts are translated at the average rates of exchange prevailing during the year. The national currencies of the

international operations are generally their functional currencies.