The Hartford 2007 Annual Report Download - page 159

Download and view the complete annual report

Please find page 159 of the 2007 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

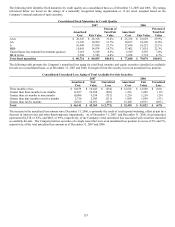

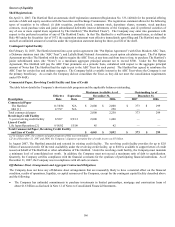

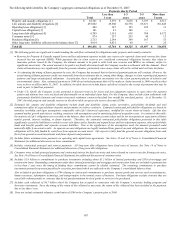

159

current relationship between short-term and long-term interest rates will remain constant over time. As a result, these calculations may

not fully capture the impact of portfolio re-allocations, significant product sales or non-parallel changes in interest rates.

Equity Risk

The Company’s operations are significantly influenced by changes in the equity markets, primarily in the U.S., but increasingly in Japan

and other global markets. The Company’ s profitability in its investment products businesses depends largely on the amount of assets

under management, which is primarily driven by the level of deposits, equity market appreciation and depreciation and the persistency

of the in-force block of business. Prolonged and precipitous declines in the equity markets can have a significant effect on the

Company’s operations, as sales of variable products may decline and surrender activity may increase, as customer sentiment towards the

equity market turns negative. Lower assets under management will have a negative effect on the Company’ s financial results, primarily

due to lower fee income related to the Retail, Retirement Plans, Institutional and International and, to a lesser extent, the Individual Life

segment, where a heavy concentration of equity linked products are administered and sold.

Furthermore, the Company may experience a reduction in profit margins if a significant portion of the assets held in the U.S. variable

annuity separate accounts move to the general account and the Company is unable to earn an acceptable investment spread, particularly

in light of the low interest rate environment and the presence of contractually guaranteed minimum interest credited rates, which for the

most part are at a 3% rate.

In addition, immediate and significant declines in one or more equity markets may also decrease the Company’ s expectations of future

gross profits in one or more product lines, which are utilized to determine the amount of DAC to be amortized in reporting product

profitability in a given financial statement period. A significant decrease in the Company’ s future estimated gross profits would require

the Company to accelerate the amount of DAC amortization in a given period, which, particularly in the case of U.S. variable annuities,

could potentially cause a material adverse deviation in that period’ s net income. Although an acceleration of DAC amortization would

have a negative effect on the Company’s earnings, it would not affect the Company’ s cash flow or liquidity position.

The Company sells variable annuity contracts that offer one or more living benefits, the value of which, to the policyholder, generally

increases with declines in equity markets. As is described in more detail below, the Company manages the equity market risks

embedded in these guarantees through reinsurance, product design and hedging programs. The Company believes its ability to manage

equity market risks by these means gives it a competitive advantage; and, in particular, its ability to create innovative product designs

that allow the Company to meet identified customer needs while generating manageable amounts of equity market risk. The Company’ s

relative sales and variable annuity market share in the U.S. have generally increased during periods when it has recently introduced new

products to the market. In contrast, the Company’ s relative sales and market share have generally decreased when competitors introduce

products that cause an issuer to assume larger amounts of equity and other market risk than the Company is confident it can prudently

manage. The Company believes its long-term success in the variable annuity market will continue to be aided by successful innovation

that allows the Company to offer attractive product features in tandem with prudent equity market risk management. In the absence of

this innovation, the Company’ s market share in one or more of its markets could decline. At times, the Company has experienced lower

levels of U.S. variable annuity sales as competitors continue to introduce new equity guarantees of increasing risk and complexity. New

product development is an ongoing process. During the first quarter of 2007, the Company launched a new product in its Japan

variable annuity business (“3 Win”) which provides three different potential outcomes for the contract holder. The first outcome allows

the contract holder to lock-in gains on their account value after a 5-year waiting period and upon reaching a specified appreciation target

chosen by the policyholder. Upon reaching the target and after a 5-year waiting period, contract holder funds are transferred out of the

underlying funds and into the Company’ s general account from which the contract holder can access their account value without

penalty. The second outcome provides a “safety-net” that provides the contract holder a guaranteed minimum income benefit (“GMIB”)

returning the contract holder’ s original deposit over 15 years, if the contract holder’ s account value drops by more than 20% from the

original deposit. The third outcome provides the contract holder a guaranteed minimum accumulation benefit (“GMAB”) of the contract

holder’ s original deposit in a lump sum if the first two outcomes are not met after a ten-year waiting period. This is the Company’ s first

GMAB issuance. GMABs are accounted for differently from GMIBs, as described below. Due to the structure of this product,

significant equity market movements, either up, to a level that the specified appreciation target is reached, or down by more than 20% of

the actual deposit, can result in significant DAC charges as the life of the product will have expired upon reaching either target. There is

also a return of premium death benefit attached to this product. In addition, the Company expects to make further changes in its living

benefit offerings from time to time. Depending on the degree of consumer receptivity and competitor reaction to continuing changes in

the Company’ s product offerings, the Company’ s future level of sales will continue to be subject to a high level of uncertainty. As of

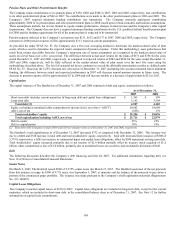

December 31, 2007, account values associated with 3 Win were $2.7 billion. In addition, as of December 31, 2007, guaranteed balances

associated with 3 Win were $2.8 billion.

The accounting for various benefit guarantees offered with variable annuity contracts can be significantly different. Those accounted for

under SFAS 133 (such as GMWBs or GMABs) are subject to significant fluctuation in value, which is reflected in net income, due to

changes in interest rates, changes in the risk-free rate used for discounting equity markets and equity market volatility as use of those

capital market rates are required in determining the liability’ s fair value at each reporting date. Benefit guarantee liabilities accounted

for under SOP 03-1 (such as GMIBs and GMDBs) may also change in value; however, the change in value is not immediately reflected

in net income. Under SOP 03-1, the income statement reflects the current period increase in the liability due to the deferral of a

percentage of current period revenues. The percentage is determined by dividing the present value of claims by the present value of

revenues using best estimate assumptions over a range of market scenarios and discounted at a rate consistent with that used in the