The Hartford 2007 Annual Report Download - page 206

Download and view the complete annual report

Please find page 206 of the 2007 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (continued)

F-29

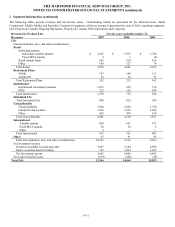

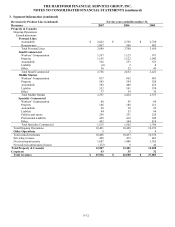

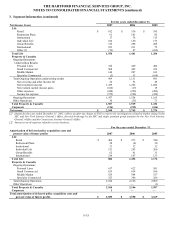

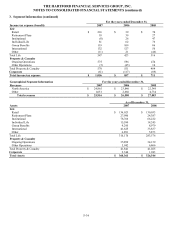

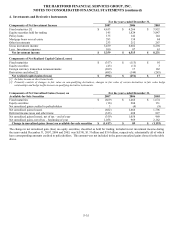

3. Segment Information

The Hartford is organized into two major operations: Life and Property & Casualty, each containing reporting segments. Within the

Life and Property & Casualty operations, The Hartford conducts business principally in eleven reporting segments. Corporate

primarily includes the Company’ s debt financing and related interest expense, as well as other capital raising activities and purchase

accounting adjustments.

Life

Life’ s business is conducted by Hartford Life, Inc. (“Hartford Life” or “Life”), an indirect subsidiary of The Hartford, headquartered in

Simsbury, Connecticut, and is a leading financial services and insurance organization. Life includes six reporting segments: Retail

Products Group (“Retail”), Retirement Plans, Institutional Solutions Group (“Institutional”), Individual Life, Group Benefits and

International. In 2007, Life changed its reporting for realized gains and losses, as well as credit risk charges previously allocated

between Life Other and each of Life’s reporting segments. All segment data for prior reporting periods have been adjusted to reflect

the current segment reporting.

Retail offers individual variable and fixed market value adjusted (“MVA”) annuities, retail mutual funds, 529 college savings plans,

Canadian and offshore investment products.

Retirement Plans provides products and services to corporations pursuant to Section 401(k) and products and services to municipalities

and not-for-profit organizations under Section 457 and 403(b) of the IRS code.

Institutional primarily offers institutional liability products, including stable value products, structured settlements and institutional

annuities (primarily terminal funding cases), as well as variable Private Placement Life Insurance (“PPLI”) owned by corporations and

high net worth individuals. Institutional also offers mutual funds to institutional investors. Furthermore, Institutional offers additional

individual products including structured settlements, single premium immediate annuities and longevity assurance.

Individual Life sells a variety of life insurance products, including variable universal life, universal life, interest sensitive whole life and

term life.

Group Benefits provides individual members of employer groups, associations, affinity groups and financial institutions with group

life, accident and disability coverage, along with other products and services, including voluntary benefits, and group retiree health.

International, which has operations located in Japan, Brazil, Ireland and the United Kingdom, provides investments, retirement savings

and other insurance and savings products to individuals and groups outside the United States and Canada.

Life includes in an Other category its leveraged PPLI product line of business; corporate items not directly allocated to any of its

reportable operating segments; inter-segment eliminations and the mark-to-market adjustment for the International variable annuity

assets that are classified as equity securities held for trading reported in net investment income and the related change in interest

credited reported as a component of benefits, losses and loss adjustment expenses since these items are not considered by the

Company’ s chief operating decision maker in evaluating the International results of operations.

Life charges direct operating expenses to the appropriate segment and allocates the majority of indirect expenses to the segments based

on an intercompany expense arrangement. Inter-segment revenues primarily occur between Life’s Other category and the reporting

segments. These amounts primarily include interest income on allocated surplus and interest charges on excess separate account

surplus.

The accounting policies of the reporting segments are the same as those described in the summary of significant accounting policies in

Note 1. Life evaluates performance of its segments based on revenues, net income and the segment’ s return on allocated capital. Each

reporting segment is allocated corporate surplus as needed to support its business.

Property & Casualty

Property & Casualty is organized into five reporting segments: the underwriting segments of Personal Lines, Small Commercial,

Middle Market and Specialty Commercial (collectively “Ongoing Operations”); and the Other Operations segment. In 2007, Property

& Casualty changed its reporting segments to reflect the current manner by which its chief operating decision maker views and

manages the business. All segment data for prior reporting periods have been adjusted to reflect the current segment reporting.

Personal Lines provides automobile, homeowners’ and home-based business coverages to the members of AARP through a direct

marketing operation and to individuals who prefer local agent involvement through a network of independent agents in the standard

personal lines market. Up until the sale of the business on November 30, 2006, the Company also sold non-standard auto insurance

through the Company’ s Omni Insurance Group, Inc. (“Omni”) subsidiary (refer to Note 20 for further discussion). Personal Lines also

operates a member contact center for health insurance products offered through the AARP Health program. AARP accounts for earned

premiums of $2.7 billion, $2.5 billion and $2.3 billion in 2007, 2006 and 2005, respectively, which represented 26%, 24% and 23% of

total Property & Casualty earned premiums in 2007, 2006 and 2005, respectively.