Travelers 2005 Annual Report Download - page 16

Download and view the complete annual report

Please find page 16 of the 2005 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

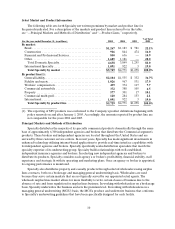

|

|

4

emphasis on guaranteed cost programs. A key objective of Commercial Accounts is continued focus on

first party product lines of business, which cover risks of loss to property of the insured

Beyond the traditional middle market network, dedicated underwriting units exist to complement the

middle market or specifically respond to the unique or unusual business client insurance needs. These

units are as follows:

•National Property provides insurance coverage for large commercial property schedules and mid-

sized risks covering losses onbuildings, business assets and business interruption exposures.

•Transportation provides auto liability, damage coverage, cargo and general liability coverages to the

trucking industry. Products have been developed for Non-fleet (generally 1-10 units) and Fleet

(11+ units) customers and are distributed through general agents.

•Boiler and Machinery provides comprehensive breakdown coverages for equipment including

property and business interruption coverages. Through the BoilerRe unit, Boiler and Machinery

also provides reinsurance, underwriting, engineering, claim handlingand risk management services

to other property casualty carriers that do not have in-house expertise.

•Inland Marine provides insurance which generally covers articles that may be transported from one

place to another, goods in transit (other than transoceanic) and movable objects. Coverages include

builder’s risk, contractor’s equipment, fine arts, jewelers, motor truck cargo and transportation

risks.

•Agribusiness offers property and liability coverages other than workers’ compensation for farms,

ranches and larger commercial growers of agricultural products.

•Excess and Surplus coverages are written on a non-admitted basis through established wholesalers.

Coverages typically underwritten include commercial auto and general liability.

•National Programs offers tailored insurance products to commercial insureds with similar risk

characteristics, underwritten on a program basis. Programs are typically marketed through a single

distribution channel. The targeted industries include entertainment,leisure, service, retail and

sports.

Select Accounts is a leading provider of property casualty products to small businesses. It serves firms

with generally fewer than 50 employees. Products offered by Select Accounts are guaranteed cost policies,

often a packaged product covering property and liability exposures. Products are sold through independent

agents and brokers, who are often the same agents and brokers that sell the Company’s Commercial

Accounts, Specialty and Personal products. In addition to the traditional small commercial agency

network, Select Accounts has a dedicated servicing unit that serves unique customer needs, including small

national programs, architects and engineers, and emerging distribution markets.

Select Accounts offers its independent agents a system for small businesses that helps them connect

all aspects of sales and service through a comprehensive service platform. Components of the platform

include agency automation capabilities and service centers that function as an extension of an agency’s

customer service operations, both of which are highly utilized by agencies. More than86% of Select

Accounts’ eligible business volume is processed by agencies using its automated issuance systems, which

allow agents to quote and issue policies from agency offices. Approximately 4,600 agencies have chosen to

take advantage of Select Accounts’ service centers, which offer agencies a wide range of services, including

coverage and billinginquiries, policy changes, the assistance of licensed service professionals and extended

hours of operations.

National Accounts sells a variety of casualty products and services to large companies. National

Accounts clients generally select loss-sensitive products in connection with a large deductible or self-