Travelers 2005 Annual Report Download - page 118

Download and view the complete annual report

Please find page 118 of the 2005 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

|

|

106

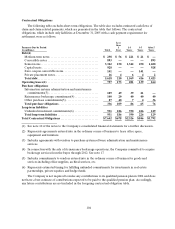

The amounts reported in the table are presented on a nominal basis and have not been adjusted to

reflect the time value of money. Accordingly, the amounts above will differ from the Company’s

balance sheet to the extent that the liability for claims and claim adjustment expenses has been

discounted in the balance sheet. (See note 1of the financial statements.)

(2) Workers’ compensation large deductible policies provide third party coverage in which the Company

typically is responsible for paying the entire loss under such policies and then seeks reimbursement

from the insured for the deductible amount. “Claims from large deductible policies” represent the

estimated future payment for claims and claim related expenses below the deductible amount, net of

the estimated recovery of the deductible. The liability and the related deductible receivable for unpaid

claims are presented in the consolidated balance sheet as “contractholder payables” and

“contractholder receivables,” respectively. Most deductibles for suchpolicies are paid directly from

the policyholder’s escrow which is periodically replenished by the policyholder. The payment of the

loss amounts above the deductible are reported within “Claims and claim adjustment expenses” in the

above table. Because the timing of the collection of the deductible (contractholder receivables) occurs

shortly after the payment of the deductible to a claimant (contractholder payables), these cash flows

offset each other in the table.

The estimated timing of the payment of the contractholder payables and the collection of

contractholder receivables for workers’ compensation policies is presented below:

(in millions) Total

Less than 1

Year

1-3

Years

3-5

Years

After 5

Years

Contractholder payables/ receivables ......... $ 5 ,516 $ 1,362 $ 1,492 $ 755 $1,907

(3) The amounts in “Loss-based assessments” relate to estimated future payments of second-injury fund

assessments which would result from payment of current claim liabilities. Second injury funds cover

the cost of any additional benefits for aggravation of apre-existing condition. For loss-based

assessments, the cost is shared by the insurance industry and self-insureds, funded through

assessments to insurance companies and self-insureds based on losses. Amounts relating to second-

injury fund assessments are included in “other liabilities” in the consolidated balance sheet.

(4) The amounts in “Reinsurance contracts accounted for as deposits” represent estimated future

nominal payments for reinsurance agreements that are accounted for as deposits. Amounts payable

under deposit agreements are included in “other liabilities” in the consolidated balance sheet. The

amounts reported in the table are presented on a nominal basis and have not been adjusted to reflect

the time value of money. Accordingly, the amounts above will differ from the Company’s balance

sheet to the extent that deposit values in the balance sheet have been discounted using deposit

accounting.

(5) The amounts in “Payouts from ceded funds withheld” represent estimated payments for losses and

return of funds held related to certain reinsurance arrangements whereby the Company holds a

portion of the premium due to the reinsurer and is allowed to pay claims from the amounts held.

The above table does not include an analysis of liabilities reported for structured settlements for

which the Company has purchased annuities and remains contingently liable in the event of default by the

company issuing the annuity. The Company is not reasonably likely to incur future payment obligations

under such agreements. See note 9 of the Company’s consolidated financial statements for a further

discussion.

Dividend Availability

The Company’s principal insurance subsidiaries are domiciled in the states of Connecticut and

Minnesota. The insurance holding company laws of both states applicable to the Company’s subsidiaries