Travelers 2005 Annual Report Download - page 138

Download and view the complete annual report

Please find page 138 of the 2005 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

|

|

126

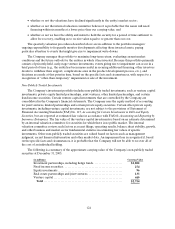

The primary market risk for all of the Company’s debt is interest rate risk at the time of refinancing.

The Company monitors the interest rate environment and evaluates refinancing opportunitiesas maturity

dates approach. For additional information regarding the Company’s debt see note 10 to the Company’s

consolidated financial statements as well as the Liquidity and Capital Resources section of Management’s

Discussion and Analysis.

The Company’s foreign exchange market risk exposure is concentrated in the Company’s invested

assets and insurance reserves denominated in foreign currencies. Cash flows from the Company’s foreign

operations are the primary source of funds for the purchase of investments denominated in foreign

currencies. The Company purchases these investments primarily to fund insurance reserves and other

liabilities denominated in the same currency, effectively reducing its foreign currency exchange rate

exposure. Invested assets denominated in the British Pound Sterling comprised approximately 2.4% and

3.5% of the total invested assets at December 31, 2005 and 2004, respectively. No other individual foreign

currency accounted for more than 1.8% of the Company’s invested assets at December 31, 2005 or 2004.

There were no other significant changes in the Company’s primary market risk exposures or in how

those exposures were managed for the year ended December 31, 2005 compared to the year ended

December 31, 2004. The Company does not currently anticipate significant changes in its primary market

risk exposures or in how those exposures are managed in future reporting periods based upon what is

known or expected to be in effect in future reporting periods.

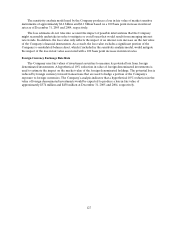

SENSITIVITY ANALYSIS

Sensitivity analysis is defined as the measurement of potential loss in future earnings, fair values or

cash flows ofmarket sensitive instruments resulting from one or more selected hypothetical changes in

interest rates and other market rates or prices over a selected time. In the Company’s sensitivity analysis

model, a hypothetical change in market rates is selected that is expected to reflect reasonably possible

near-term changes in those rates. “Near-term” means a period of time going forward up to one year from

the date of the consolidated financial statements. Actual results may differ from the hypothetical change in

market rates assumed in this disclosure, especially since this sensitivity analysis does not reflect the results

of any actions that would be taken by the Company to mitigate such hypothetical losses in fair value.

Interest RateRisk

In this sensitivity analysis model, the Company uses fair values to measure its potential loss. The

sensitivity analysis model includes the following financial instruments entered intofor purposes other than

trading: fixed maturities, non-redeemable preferred stocks, mortgage loans, short-term securities, debt and

derivative financial instruments. The primary market risk to the Company’s market sensitive instruments is

interest rate risk. The sensitivity analysis model uses a 100 basis point change in interest rates to measure

the hypothetical change in fair value of financial instruments included in the model.

For invested assets with primary exposure to interest rate risk, estimates of portfolio duration and

convexity are used to model the loss of fair value that would be expected to result from a parallel increase

in interest rates. Durations on invested assets are adjusted for call, put and interest rate reset features.

Durations on tax-exempt securities are adjusted for the fact that the yields on such securities do not

normally move in lockstep with changes in the U.S. Treasury curve. Fixed maturity portfolio durations are

calculated ona market value weighted basis, including accrued interest, using holdings as of December 31,

2005 and 2004.

For debt, the change in fair value is determined by calculating hypothetical December 31, 2005 and

2004 ending prices based on yields adjusted to reflect a 100basis point change, comparing such

hypothetical ending prices to actual ending prices, and multiplying the difference by the par or securities

outstanding.