Travelers 2005 Annual Report Download - page 108

Download and view the complete annual report

Please find page 108 of the 2005 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

|

|

96

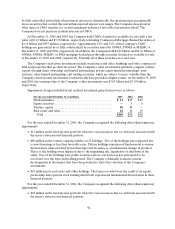

Following are the pretax realized losses on investments sold during the year ended December 31,

2005:

(in millions) Loss Fair Value

Fixed maturities ............................................. $118 $ 3,274

Equity securities ............................................. 9 166

Other...................................................... 18 242

Total....................................................... $145 $ 3,682

Resulting purchases and sales of investments are based on cash requirements, the characteristics of

the insurance liabilities and current market conditions. The Company identifies investments to be sold to

achieve its primary investment goals of assuring the Company’s ability to meet policyholder obligations as

well as to optimize investment returns, given these obligations.

OUTLOOK

The Company’s strategic objective is to enhance its position as a consistently profitable market leader

and a cost-effective provider of property and casualty insurance in the United States. A variety of factors

continue to affect the property and casualty insurance market and the Company’s core business outlook for

2006, including increasingly competitive conditions throughout the majority of markets served by the

Company’s business segments, loss cost trends (including medical inflation and auto loss costs), asbestos-

related developments and rising reinsurance and litigation costs.

The Company expects property casualty market conditions to continue to be competitive throughout

2006. Relative to 2005, within the Commercial and Specialty segments, the Company expects renewal price

changes to increase and terms, conditions and insured values to improve for exposures susceptible to

catastrophe losses, such as coastal property and oil and gas-related exposures, while renewal price changes

for non-catastrophe exposures are expected to be subject to modest declines. Also relative to 2005, within

the Personal segment, the Company expects renewal price changes in the automobile market to remain

relatively stable or decline modestly, while the homeowners market is expected to remain relatively stable.

The Company expects that the trend of increased severity and frequency of storms experienced in

2005 and 2004 will continue into 2006. Given the increased severity and frequency of storms, the Company

is reassessing its definition of and exposure to coastal risks, as well as the impact, if any, on its reinsurance

program. Accordingly, the Company is reviewing its pricing, exposures, return thresholds and terms and

conditions it offers in coastal areas. In part as a result of the severity and frequency of storms in 2005 and

2004, the Company expects the cost of reinsurance to increase, and there may be reduced availability of

reinsurance coverage. To the extent that the Company is not able to reflect the potentially increased costs

of increased severity and frequency of storms or reinsurance in its pricing, the Company’s results of

operations will be adversely impacted. In particular, in the Personal segment, the Company expects a delay

in its ability to increase pricing to offset these potentially increased costs since the Company cannot

increase rates to the extentnecessary without the approval of the regulatory authorities of certain states.

Also, particularly in light of the frequency and severity of storms in the past two years, rating agencies may

increase their capital requirements for the Company.

With respect to non-catastrophe claim frequency, the industry has experienced unprecedented low

levels over the last several years, a trend that the Company does not expect to change materially in 2006.

The Company expects severity trend, the other component of loss trend, to continue to remain stable for

non-catastrophe claims. Nevertheless, with continued pressure on pricing, it is possible that margins will

contract in certain parts of the Company’s business in 2006.