Travelers 2005 Annual Report Download - page 158

Download and view the complete annual report

Please find page 158 of the 2005 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

|

|

THE ST. PAUL TRAVELERS COMPANIES, INC.AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

146

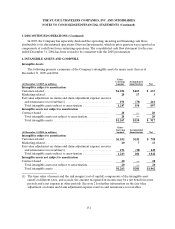

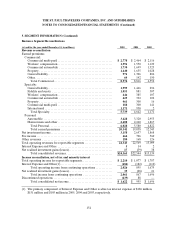

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Cont inued)

insureds to access portions of the impacted areas, the complexity of factors contributing to the losses, the

legal and regulatory uncertainties and the nature of the information available to establish the reserves.

Complex factors include, but are not limited to: determining whether damage was caused by flooding

versus wind; evaluating general liability and pollution exposures; estimating additional living expenses; the

impact of demand surge; infrastructure disruption; fraud; the effect of mold damage and business

interruption costs; and reinsurance collectibility. The timing of a catastrophe’s occurrence, such as at or

near the end of a reporting period, can also affect the information available to the Company in estimating

reserves for that reporting period. The estimates related to catastrophes are adjusted as actual claims

emerge.

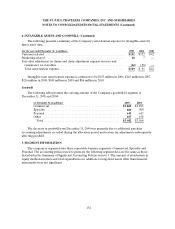

Terrorism Risk Insurance Act of 2002 and Terrorism Risk Insurance Extension Act of 2005

On November 26, 2002, the Terrorism Risk Insurance Act of 2002 (the Terrorism Act) was enacted

into Federal law and established the Terrorism Risk Insurance Program (the Program), a temporary

Federal program in the Department of the Treasury, that provided fora system of shared public and

private compensation for insured losses resulting from acts of terrorism or war committed by or on behalf

of a foreign interest. The Program was scheduled to terminate on December 31, 2005. On December 22,

2005, the Terrorism Risk Insurance Extension Act of 2005 (theTerrorism Extension Act) was enacted into

Federal law, reauthorizing the Program through December 31, 2007, while reducing the Federal role under

the Program. In order for a loss to be covered under the Program (subject losses), the loss must meet

certain aggregate industry loss minimums that vary by Program year of amounts $100 million or less, and

must be the result of an event that is certified as an act of terrorism by the U.S. Secretary of the Treasury.

The original Program excluded from participation certain of the following types of insurance: Federal crop

insurance, private mortgage insurance, financial guaranty insurance, medical malpractice insurance, health

or life insurance, flood insurance, and reinsurance. The Terrorism Extension Act exempted from coverage

certain additional types of insurance, including commercial automobile, professional liability (other than

directors and officers’), surety, burglary and theft, and farm-owners multi-peril. In the case of a war

declared by Congress, only workers’ compensation losses are covered by the Terrorism Act and the

Terrorism Extension Act. Both Acts generally require that all commercial property casualty insurers

licensed in the United States participate in the Program.Under the Program, a participating insurer is

entitled to be reimbursed by the Federal Government for a percentage of subject losses, after an insurer

deductible, subject to an annual cap. The Federal reimbursement percentage remains at 90% for 2006, but

decreases to 85% in 2007. In each case, the deductible is calculated by applying the deductible percentage

to the insurer’s direct earned premiums for covered lines from the calendar year immediately preceding

the applicable year. The deductible under the Program was 7% for 2003, 10% for 2004 and 15% for 2005,

and will be 17.5% for 2006 and 20% for 2007. The Company’s estimated deductible under the Program is

$1.91 billion for 2006. The annual cap limits the amountof aggregate subject losses for all participating

insurers to $100 billion. Once subject losses have reached the $100 billion aggregate during a program year,

there is no additional reimbursement from the U.S. Treasury and an insurer that has met its deductible for

the program year is not liable for any losses (or portion thereof) that exceed the $100 billion cap. The

Company had no terrorism-related losses in 2005, 2004 or 2003.