Travelers 2005 Annual Report Download - page 119

Download and view the complete annual report

Please find page 119 of the 2005 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

|

|

107

requires notice to, and approval by, the state insurance commissioner for the declaration or payment of

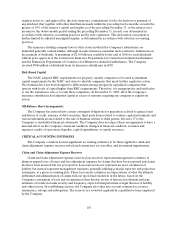

any dividend, that together withother distributions made within the preceding twelve months, exceeds the

greater of 10% of the insurer’s capital and surplus as of the preceding December 31, or the insurer’s net

income for the twelve-month period ending the preceding December 31, in each case determined in

accordance with statutory accounting practices and by state regulation. This declaration or payment is

further limited by adjusted unassigned surplus, as determined in accordance with statutory accounting

practices.

The insurance holding company laws of other states in which the Company’s subsidiaries are

domiciled generally contain similar, although in some instances somewhat more restrictive, limitations on

the payment of dividends. A maximum of$2.56 billion is available by the end of 2006 for such dividends

without prior approval of the Connecticut Insurance Department for Connecticut-domiciled subsidiaries

and the Minnesota Department of Commerce for Minnesota-domiciled subsidiaries. The Company

received $968 million of dividends from its insurance subsidiaries in2005.

Risk-Based Capital

The NAIC adopted RBC requirements for property casualty companies to be used as minimum

capital requirements by the NAIC and states to identify companies that merit further regulatory action.

The formulas have not been designed to differentiate among adequately capitalized companies that

operate with levels of capital higher than RBC requirements. Therefore, it is inappropriate and ineffective

to use the formulas to rate or to rank these companies. At December 31, 2005, all of the Company’s

insurance subsidiaries had adjusted capital in excess of amounts requiring any company or regulatory

action.

Off-Balance Sheet Arrangements

The Company has entered into certain contingent obligations for guarantees related to agency loans

and letters of credit, issuance of debt securities, third party loans related to venture capital investments and

various indemnifications related to the sale of business entities to third parties. See note 17 to the

Company’s consolidated financial statements. The Company does not expect these arrangements to have a

material effect on the Company’s financial condition, changes in financial condition, revenues and

expenses, results of operations, liquidity, capital expenditures or capital resources.

CRITICAL ACCOUNTING ESTIMATES

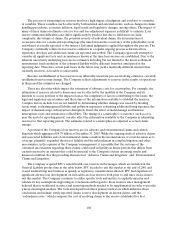

The Company considers its most significant accountingestimates to be those applied to claim and

claim adjustment expense reserves and related reinsurance recoverables, and investment impairments.

Claim and Claim Adjustment Expense Reserves

Claim and claim adjustment expense reserves (loss reserves) represent management’s estimate of

ultimate unpaid costs of losses and loss adjustment expenses for claims that have been reported and claims

that have been incurred but not yet reported. Loss reserves do not represent an exact calculation of

liability, but instead represent management estimates, generally utilizing actuarial expertise and projection

techniques, at a given accounting date. These loss reserve estimates are expectations of what the ultimate

settlement and administration of claims will cost upon final resolution in the future, based on the

Company’s assessment of facts and circumstances then known, review of historical settlement patterns,

estimates of trends in claims severity and frequency, expected interpretations of legal theories of liability

and other factors. In establishing reserves, the Company also takes into account estimated recoveries,

reinsurance, salvage and subrogation. The reserves are reviewed regularly by a qualified actuary employed

by the Company.