Travelers 2005 Annual Report Download - page 157

Download and view the complete annual report

Please find page 157 of the 2005 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

|

|

THE ST. PAUL TRAVELERS COMPANIES, INC.AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

145

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Cont inued)

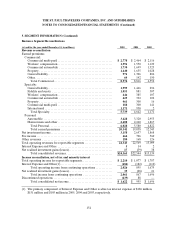

Net written premiums by market were as follows:

(for the year ended December 31, in millions) 2005 2004 2003

Bond.............................................. $1,267 $1,183 $ 781

Construction ....................................... 916 844 474

Financial andProfessional Services. ................... 850 636 —

Domestic Specialty Other............................ 1,605 1,186 —

Total Domestic Specialty .......................... 4,638 3,849 1,255

International Specialty............................... 1,091 922 3

Total Specialty ................................... $5,729 $4,771 $ 1 ,258

Personal

Personal writes virtually all types of property and casualty insurance covering personal risks. The

primary coverages in Personal are automobile and homeowners insurance sold to individuals. These

products are distributed through independent agents, sponsoring organizations such as employee and

affinity groups, and joint marketing arrangements with other insurers.

Automobile policies provide coverage for liability to others for both bodily injury and property

damage, and for physical damage to an insured’s own vehicle from collision and various other perils. In

addition, many states require policies to provide first-party personal injury protection, frequently referred

to as no-fault coverage.

Homeowners policies are available for dwellings, condominiums, mobile homes and rental property

contents. Protection against losses to dwellings and contents from a wide variety of perils is included in

these policies, as well as coverage for liability arising from ownership or occupancy.

Net written premiums by product line were as follows:

(for the year ended December 31, in millions) 2005 2004 2003

Automobile ........................................ $3,477 $3,433 $ 3 ,054

Homeowners and other.............................. 2,751 2,496 2,027

Total Personal.................................... $6,228 $5,929 $ 5 ,081

Catastrophe Exposure

The Company has geographic exposure to catastrophe losses in certain areas of the country.

Catastrophes can be caused by various natural and man-made events including hurricanes, windstorms,

earthquakes, hail, severe winter weather, explosions and fires. The incidence and severity of catastrophes

are inherently unpredictable. The extentof losses from a catastrophe is a function of both the total amount

of insured exposure in the area affected by the event and the severity of the event. Most catastrophes are

restricted to small geographic areas; however, hurricanes and earthquakes may produce significant damage

in larger areas, especially those that are heavily populated. The Company generally seeks to reduce its

exposure to catastrophes through individual risk selection and the purchase of catastrophe reinsurance.

There are risks which impact the estimation of ultimate costs for catastrophes. For example, the

estimation of reserves related to hurricanes can be affected by the inability of the Company and its