IBM 2015 Annual Report Download - page 93

Download and view the complete annual report

Please find page 93 of the 2015 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

|

|

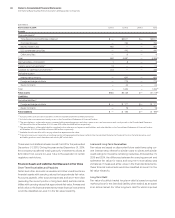

Notes to Consolidated Financial Statements

International Business Machines Corporation and Subsidiary Companies

91

securities that the company intends to sell or would more likely

than not be required to sell before the expected recovery of the

amortized cost basis are charged to other (income) and expense

in the period in which the loss occurs. For debt securities that the

company has no intent to sell and believes that it more likely than

not will not be required to sell prior to recovery, only the credit loss

component of the impairment is recognized in other (income) and

expense, while the remaining loss is recognized in OCI. The credit

loss component recognized in other (income) and expense is iden-

tified as the amount of the principal cash flows not expected to be

received over the remaining term of the debt security as projected

using the company’s cash flow projections.

Inventories

Raw materials, work in process and finished goods are stated at

the lower of average cost or market. Cash flows related to the

sale of inventories are reflected in net cash provided by operating

activities in the Consolidated Statement of Cash Flows.

Allowance for Credit Losses

Receivables are recorded concurrent with billing and shipment of

a product and/or delivery of a service to customers. A reasonable

estimate of probable net losses on the value of customer receiv-

ables is recognized by establishing an allowance for credit losses.

Notes and Accounts Receivable—Trade

An allowance for uncollectible trade receivables is estimated

based on a combination of write-off history, aging analysis and

any specific, known troubled accounts.

Financing Receivables

Financing receivables include sales-type leases, direct financing

leases and loans. Leases are accounted for in accordance with

lease accounting standards. Loan receivables are financial assets

recorded at amortized cost which approximates fair value. The

company determines its allowances for credit losses on financing

receivables based on two portfolio segments: lease receivables

and loan receivables. The company further segments the portfolio

into two classes: major markets and growth markets.

When calculating the allowances, the company considers its

ability to mitigate a potential loss by repossessing leased equip-

ment and by considering the current fair market value of any other

collateral. The value of the equipment is the net realizable value.

The allowance for credit losses for capital leases, installment sales

and customer loans includes an assessment of the entire balance

of the capital lease or loan, including amounts not yet due. The

methodologies that the company uses to calculate its receivables

reserves, which are applied consistently to its different portfolios,

are as follows:

Individually Evaluated—The company reviews all financing receiv-

ables considered at risk on a quarterly basis. The review primarily

consists of an analysis based upon current information available

about the client, such as financial statements, news reports, pub-

lished credit ratings, current market-implied credit analysis, as well

as the current economic environment, collateral net of reposses-

sion cost and prior collection history. For loans that are collateral

dependent, impairment is measured using the fair value of the col-

lateral when foreclosure is probable. Using this information, the

company determines the expected cash flow for the receivable

and calculates an estimate of the potential loss and the probabil-

ity of loss. For those accounts in which the loss is probable, the

company records a specific reserve.

Collectively Evaluated—The company records an unallocated

reserve that is calculated by applying a reserve rate to its differ-

ent portfolios, excluding accounts that have been specifically

reserved. This reserve rate is based upon credit rating, probabil-

ity of default, term, characteristics (lease/loan) and loss history.

Factors that could result in actual receivable losses that are mate-

rially different from the estimated reserve include sharp changes in

the economy, or a significant change in the economic health of a

particular client that represents a concentration in the company’s

receivables portfolio.

Other Credit-Related Policies

Non-Accrual—Certain receivables for which the company has

recorded a specific reserve may also be placed on non-accrual

status. Non-accrual assets are those receivables (impaired

loans or nonperforming leases) with specific reserves and other

accounts for which it is likely that the company will be unable to

collect all amounts due according to original terms of the lease

or loan agreement. Income recognition is discontinued on these

receivables. Cash collections are first applied as a reduction to

principal outstanding. Any cash received in excess of principal

payments outstanding is recognized as interest income. Receiv-

ables may be removed from non-accrual status, if appropriate,

based upon changes in client circumstances.

Write Off—Receivable losses are charged against the allow-

ance when management believes the uncollectibility of the

receivable is confirmed. Subsequent recoveries, if any, are cred-

ited to the allowance.

Past Due—The company views receivables as past due when

payment has not been received after 90 days, measured from the

original billing date.

Impaired Loans—As stated above, the company evaluates all

financing receivables considered at-risk, including loans, for

impairment on a quarterly basis. The company considers any

loan with an individually evaluated reserve as an impaired loan.

Depending on the level of impairment, loans will also be placed

on non-accrual status as appropriate. Client loans are primarily

for software and services and are unsecured. These loans are

subjected to credit analysis to evaluate the associated risk and,

when deemed necessary, actions are taken to mitigate risks in the

loan agreements which include covenants to protect against credit

deterioration during the life of the obligation.