IBM 2015 Annual Report Download - page 52

Download and view the complete annual report

Please find page 52 of the 2015 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

|

|

50 Management Discussion

International Business Machines Corporation and Subsidiary Companies

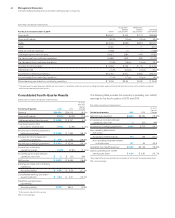

The company has a set of strategic imperatives for growth that

are focused on the market shifts in data, cloud and engagement.

The model for these combined strategic imperatives is to deliver

double-digit revenue growth. In 2014, revenue from cloud, ana-

lytics, mobile, social and security solutions combined, increased

16percent with double-digit growth in each quarter. In total, the

strategic imperatives generated $25billion in revenue, which

represented approximately 27percent of total revenue. Business

analytics revenue of $17billion increased 7percent year to year

with growth led by the consulting business, as the company helped

clients extract value from their data. Cloud revenue of $7billion

was up 60percent year to year as client demand grew for high-

er-value cloud solutions across public, private and hybrid clouds.

Cloud delivered as-a-Service revenue increased approximately

75percent to $3billion in 2014, and exited the year with an annual

run rate of $3.5billion. Cloud revenue also includes the compa-

ny’s foundational offerings where it provides software, hardware

and services to clients to build private clouds. In engagement, the

mobile business more than tripled year to year with strong growth

in MobileFirst driven by the integrated portfolio of offerings. Secu-

rity revenue increased 19percent year to year.

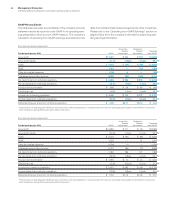

The company continued to shift its investments and resources

to the strategic imperatives and solutions that address clients’

most critical needs. During 2014, the company spent approxi-

mately 6percent of revenue in research and development and

invested approximately $4billion on capital investments—support-

ing actions in a number of areas that will yield financial benefits in

the future. For example:

• Launched Bluemix, the company’s cloud Platform-as-a-

Service for the enterprise.

• Invested to globally expand the SoftLayer cloud datacenters.

• Invested to bring Watson’s capabilities to the enterprise and

to build a partner ecosystem, effectively creating a market for

cognitive computing.

• Introduced cloud application innovations around Watson

Analytics and Verse.

• Launched POWER8, and building the OpenPOWER

consortium.

• Formed a partnership with Apple for enterprise mobility, with

Twitter for big data, and with SAP and Tencent for cloud.

The recurring core franchises include the annuity businesses, and

the highly recurring portions of the transactions business, such as

mainframe revenue from the largest clients. This content has annu-

ity characteristics, and in many cases, it supports mission-critical

processes for clients. The model for these combined businesses

is to have stable revenue, with improving margins. In 2014, reve-

nue was down approximately 3percent with a modest decline in

margin. The decline was primarily driven by the mainframe product

cycle and currency.

The company’s high-value transactional businesses include

project-based work in services, transactional software, Power

Systems and Storage—in areas other than the strategic imper-

atives. The objective for these businesses is to optimize the

business model and maintain margins. In 2014, revenue declined

year to year, with gross margins over 40percent. Performance

reflected the secular challenges faced in some parts of the hard-

ware business.

In 2014, the company divested businesses that no longer fit

its strategic profile—Systemx and the customer care business

process outsourcing services and it announced the divestiture of

the Microelectronics business. These three businesses generated

approximately $7billion of revenue when reported in 2013, but

had a pre-tax loss of approximately $500million. The divestitures

reduce revenue but improve the company’s profit profile, consis-

tent with the shift to higher value.

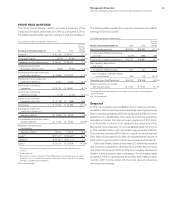

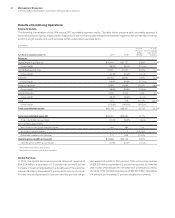

From a segment perspective, Global Services revenue declined

3.5percent as reported, but increased 1percent adjusted for the

divestitures (2points) and currency (2points). Global Technology

Services declined 0.8percent as reported, but increased 2per-

cent adjusted for currency (2points) and divestitures with growth

in outsourcing and ITS on an adjusted basis. Global Business

Services revenue decreased 8.0percent and 1percent adjusted

for divestitures (5points) and currency (2points). Software reve-

nue declined 1.9percent (1percent adjusted for currency). Total

middleware revenue was flat as reported, but increased 1percent

at constant currency. Systems Hardware revenue decreased

23.0percent as reported and 17percent adjusted for the divested

Systemx business (5points) and currency (1point). Performance

reflected the impact of the zSystems product cycle as well as

declines in Power Systems and Storage. In 2014, the company took

significant actions to reposition the Systems Hardware business

for higher value, and reinforced its commitment to driving innova-

tion in high-end systems and storage.

Revenue from the major markets declined 4.3percent as

reported and 1percent adjusted for the divestitures (2points) and

currency (1point). Growth markets revenue decreased 9.9percent

as reported and 3percent adjusted for the divestitures (3points)

and currency (4points) compared to 2013.

The consolidated gross profit margin of 50.0percent improved

0.5points year to year. The operating (non-GAAP) gross margin

of 50.6percent increased 0.1points compared to 2013 primarily

driven by an improved mix toward Software.