IBM 2015 Annual Report Download - page 92

Download and view the complete annual report

Please find page 92 of the 2015 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

|

|

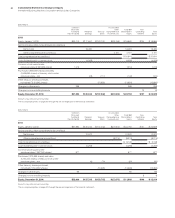

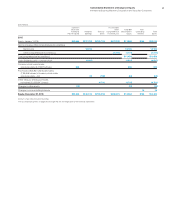

Notes to Consolidated Financial Statements

International Business Machines Corporation and Subsidiary Companies

90

currency denominated debt (included in the company’s debt risk

management program as addressed in noteD, “Financial Instru-

ments,” on pages 101 through 105), cash flows directly associated

with the settlement of the principal element of these swaps are

reported in payments to settle debt in cash flows from financing

activities in the Consolidated Statement of Cash Flows.

Financial Instruments

In determining the fair value of its financial instruments, the com-

pany uses a variety of methods and assumptions that are based

on market conditions and risks existing at each balance sheet

date. See noteD, “Financial Instruments,” on pages 100 to 101

for further information. All methods of assessing fair value result

in a general approximation of value, and such value may never

actually be realized.

Fair Value Measurement

Accounting guidance defines fair value as the price that would be

received to sell an asset or paid to transfer a liability in an orderly

transaction between market participants at the measurement date.

Under this guidance, the company is required to classify certain

assets and liabilities based on the following fair value hierarchy:

• Level1—Quoted prices (unadjusted) in active markets

for identical assets or liabilities that can be accessed at the

measurement date;

• Level2—Inputs other than quoted prices included within

Level1 that are observable for the asset or liability, either

directly or indirectly; and

• Level3—Unobservable inputs for the asset or liability.

The guidance requires the use of observable market data if such

data is available without undue cost and effort.

When available, the company uses unadjusted quoted market

prices in active markets to measure the fair value and classifies

such items within Level1. If quoted market prices are not available,

fair value is based upon internally developed models that use cur-

rent market-based or independently sourced market parameters

such as interest rates and currency rates. Items valued using inter-

nally generated models are classified according to the lowest level

input or value driver that is significant to the valuation.

The determination of fair value considers various factors includ-

ing interest rate yield curves and time value underlying the financial

instruments. For derivatives and debt securities, the company uses

a discounted cash flow analysis using discount rates commensu-

rate with the duration of the instrument.

In determining the fair value of financial instruments, the com-

pany considers certain market valuation adjustments to the “base

valuations” calculated using the methodologies described below

for several parameters that market participants would consider in

determining fair value:

• Counterparty credit risk adjustments are applied to financial

instruments, taking into account the actual credit risk of a

counterparty as observed in the credit default swap market

to determine the true fair value of such an instrument.

• Credit risk adjustments are applied to reflect the company’s

own credit risk when valuing all liabilities measured at fair

value. The methodology is consistent with that applied in

developing counterparty credit risk adjustments, but incor-

porates the company’s own credit risk as observed in the

credit default swap market.

As an example, the fair value of derivatives is derived utilizing a

discounted cash flow model that uses observable market inputs

such as known notional value amounts, yield curves, spot and

forward exchange rates as well as discount rates. These inputs

relate to liquid, heavily traded currencies with active markets which

are available for the full term of the derivative.

Certain financial assets are measured at fair value on a non-

recurring basis. These assets include equity method investments

that are recognized at fair value at the measurement date to the

extent that they are deemed to be other-than-temporarily impaired.

Certain assets that are measured at fair value on a recurring basis

can be subject to nonrecurring fair value measurements. These

assets include available-for-sale equity investments that are

deemed to be other-than-temporarily impaired. In the event of an

other-than-temporary impairment of a financial instrument, fair

value is measured using a model described above.

Accounting guidance permits the measurement of eligible

financial assets, financial liabilities and firm commitments at fair

value, on an instrument-by-instrument basis, that are otherwise not

permitted to be accounted for at fair value under other account-

ing standards. This election is irrevocable. The company has not

applied the fair value option to any eligible assets or liabilities.

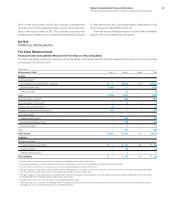

Cash Equivalents

All highly liquid investments with maturities of three months or

less at the date of purchase are considered to be cash equivalents.

Marketable Securities

Debt securities included in current assets represent securities that

are expected to be realized in cash within one year of the balance

sheet date. Long-term debt securities that are not expected to be

realized in cash within one year and alliance equity securities are

included in investments and sundry assets. Debt and marketable

equity securities are considered available for sale and are reported

at fair value with unrealized gains and losses, net of applicable

taxes, in OCI. The realized gains and losses for available-for-sale

securities are included in other (income) and expense in the Con-

solidated Statement of Earnings. Realized gains and losses are

calculated based on the specific identification method.

In determining whether an other-than-temporary decline in

market value has occurred, the company considers the duration

that, and extent to which, the fair value of the investment is below

its cost, the financial condition and near-term prospects of the

issuer or underlying collateral of a security; and the company’s

intent and ability to retain the security in order to allow for an antic-

ipated recovery in fair value. Other-than-temporary declines in fair

value from amortized cost for available-for-sale equity and debt