IBM 2015 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2015 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

|

|

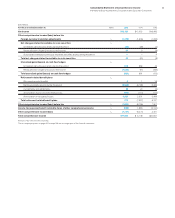

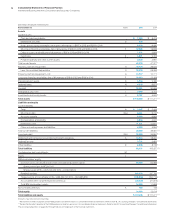

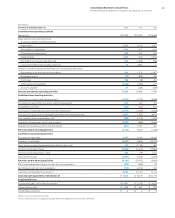

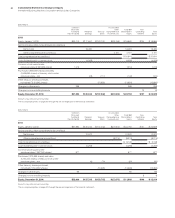

Notes to Consolidated Financial Statements

International Business Machines Corporation and Subsidiary Companies

84

The company performs ongoing profitability analyses of its

services contracts accounted for under the POC method in order

to determine whether the latest estimates of revenues, costs and

profits require updating. If at any time these estimates indicate that

the contract will be unprofitable, the entire estimated loss for the

remainder of the contract is recorded immediately. For non-POC

method services contracts, any losses are recorded as incurred.

In some services contracts, the company bills the client prior

to recognizing revenue from performing the services. Deferred

income of $6,039 million and $6,352 million at December31, 2015

and 2014, respectively, is included in the Consolidated Statement

of Financial Position. In other services contracts, the company

performs the services prior to billing the client. Unbilled accounts

receivable of $1,630 million and $1,833 million at December31, 2015

and 2014, respectively, is included in notes and accounts receiv-

able-trade in the Consolidated Statement of Financial Position.

Billings usually occur in the month after the company performs

the services or in accordance with specific contractual provisions.

Unbilled receivables are expected to be billed within four months.

Hardware

The company’s hardware offerings include the sale or lease of

system servers, storage solutions and the sale of semiconductors.

The company also offers installation services for its more complex

hardware products.

Revenue from hardware sales and sales-type leases is rec-

ognized when risk of loss has transferred to the client and there

are no unfulfilled company obligations that affect the client’s final

acceptance of the arrangement. Any cost of standard warranties

and remaining obligations that are inconsequential or perfunc-

tory are accrued when the corresponding revenue is recognized.

Revenue from rentals and operating leases is recognized on a

straight-line basis over the term of the rental or lease.

Software

Revenue from perpetual (one-time charge) license software is

recognized at the inception of the license term if all revenue rec-

ognition criteria have been met. Revenue from term (recurring

license charge) license software is recognized on a straight-line

basis over the period that the client is entitled to use the license.

Revenue from post-contract support, which may include unspec-

ified upgrades on a when-and-if-available basis, is recognized

on a straight-line basis over the period such items are delivered.

Revenue from software hosting or Software-as-a-Service arrange-

ments is recognized as the service is delivered, generally on a

straight-line basis, over the longer of the term of the arrangement

or the expected period of the customer relationship. In software

hosting arrangements, the rights provided to the customer (e.g.,

ownership of a license, contract termination provisions and the

feasibility of the customer to operate the software) are consid-

ered in determining whether the arrangement includes a license.

In arrangements which include a software license, the associated

revenue is recognized according to whether the license is perpet-

ual or term, subject to the guidance above.

In multiple-deliverable arrangements that include software

that is more than incidental to the products or services as a

whole (software multiple-deliverable arrangements), software

and software-related elements are accounted for in accordance

with software revenue recognition guidance. Software-related

elements include software products and services for which a soft-

ware deliverable is essential to its functionality. Tangible products

containing software components and non-software components

that function together to deliver the tangible product’s essential

functionality are not within the scope of software revenue recog-

nition guidance and are accounted for based on other applicable

revenue recognition guidance.

A software multiple-deliverable arrangement is separated

into more than one unit of accounting if all of the following criteria

are met:

• The functionality of the delivered element(s) is not dependent

on the undelivered element(s);

• There is vendor-specific objective evidence (VSOE) of fair

value of the undelivered element(s). VSOE of fair value is based

on the price charged when the deliverable is sold separately

by the company on a regular basis and not as part of the

multiple-deliverable arrangement; and

• Delivery of the delivered element(s) represents the culmina-

tion of the earnings process for that element(s).

If any one of these criteria is not met, the arrangement is accounted

for as one unit of accounting which would result in revenue being

recognized ratably over the contract term or being deferred until

the earlier of when such criteria are met or when the last undeliv-

ered element is delivered. If these criteria are met for each element

and there is VSOE of fair value for all units of accounting in an

arrangement, the arrangement consideration is allocated to the

separate units of accounting based on each unit’s relative VSOE

of fair value. There may be cases, however, in which there is VSOE

of fair value of the undelivered item(s) but no such evidence for

the delivered item(s). In these cases, the residual method is used

to allocate the arrangement consideration. Under the residual

method, the amount of consideration allocated to the delivered

item(s) equals the total arrangement consideration less the aggre-

gate VSOE of fair value of the undelivered elements.

The company’s multiple-deliverable arrangements may have

a stand-alone software deliverable that is subject to the existing

software revenue recognition guidance. The revenue for these

multiple-deliverable arrangements is allocated to the software

deliverable and the non-software deliverables based on the rela-

tive selling prices of all of the deliverables in the arrangement using

the hierarchy: VSOE, third-party evidence (TPE) or best estimate of

selling price (BESP). In circumstances where the company cannot

determine VSOE or TPE of the selling price for all of the delivera-

bles in the arrangement, including the software deliverable, BESP

is used for the purpose of performing this allocation.