IBM 2011 Annual Report Download - page 135

Download and view the complete annual report

Please find page 135 of the 2011 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

-

147

-

148

|

|

Notes to Consolidated Financial Statements

International Business Machines Corporation and Subsidiary Companies 133

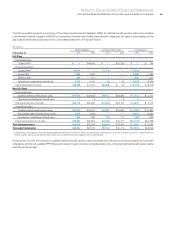

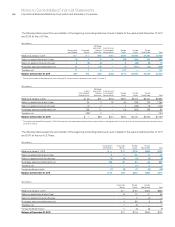

Valuation Techniques

The following is a description of the valuation techniques used to

measure plan assets at fair value. There were no changes in valuation

techniques during 2011 and 2010.

Equity securities are valued at the closing price reported on the

stock exchange on which the individual securities are traded. IBM

common stock is valued at the closing price reported on the New

York Stock Exchange. Equity commingled/mutual funds are typically

valued using the net asset value (NAV) provided by the administrator

of the fund and reviewed by the company. The NAV is based on the

value of the underlying assets owned by the fund, minus liabilities

and divided by the number of shares or units outstanding. These

assets are classified as Level 1, Level 2 or Level 3 depending on

availability of quoted market prices.

The fair value of fixed income securities is typically estimated

using pricing models, quoted prices of securities with similar

characteristics or discounted cash flows and are generally classified

as Level 2. If available, they are valued using the closing price reported

on the major market on which the individual securities are traded.

Cash includes money market accounts that are valued at their

cost plus interest on a daily basis, which approximates fair value.

Short-term investments represent securities with original maturities

of one year or less. These assets are classified as Level 1 or Level 2.

Private equity and private real estate partnership valuations

require significant judgment due to the absence of quoted market

prices, the inherent lack of liquidity and the long-term nature of such

assets. These assets are initially valued at cost and are reviewed

periodically utilizing available and relevant market data to determine

if the carrying value of these assets should be adjusted. These

investments are classified as Level 3. The valuation methodology is

applied consistently from period to period.

Exchange traded derivatives are valued at the closing price

reported on the exchange on which the individual securities are

traded, while forward contracts are valued using a mid-close price.

Over-the-counter derivatives are typically valued using pricing

models. The models require a variety of inputs, including, for example,

yield curves, credit curves, measures of volatility and foreign exchange

rates. These assets are classified as Level 1 or Level 2 depending

on availability of quoted market prices.

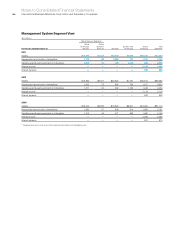

Expected Contributions

Defined Benefit Pension Plans

It is the company’s general practice to fund amounts for pensions

sufficient to meet the minimum requirements set forth in applicable

employee benefits laws and local tax laws. From time to time, the

company contributes additional amounts as it deems appropriate.

The company contributed $728 million and $801 million in cash

to non-U.S. defined benefit pension plans and $70 million and

$64 million in cash to non-U.S. multi-employer plans during the

years ended December 31, 2011 and 2010, respectively. The cash

contributions to multi-employer plans represent the annual cost

included in net periodic (income)/cost recognized in the Consolidated

Statement of Earnings. The company has no liability for participants

in multi-employer plans other than its own employees. As a result,

the company’s participation in multi-employer plans has no material

impact on the company’s financial statements.

In 2012, the company is not legally required to make any

contributions to the U.S. defined benefit pension plans. However,

depending on market conditions, or other factors, the company

may elect to make discretionary contributions to the Qualified PPP

during the year.

The Pension Protection Act of 2006 (the Act), enacted into law

in 2006, is a comprehensive reform package that, among other

provisions, increases pension funding requirements for certain U.S.

defined benefit plans, provides guidelines for measuring pension

plan assets and pension obligations for funding purposes and raises

tax deduction limits for contributions to retirement-related benefit

plans. The additional funding requirements by the Act apply to plan

years beginning after December 31, 2007. The Act was updated by

the Worker, Retiree and Employer Recovery Act of 2008, which

revised the funding requirements in the Act by clarifying that pension

plans may smooth the value of pension plans over 24 months. At

December 31, 2011, no mandatory contribution is required for 2012.

In 2012, the company estimates contributions to its non-U.S.

defined benefit and multi-employer plans to be approximately

$800 million, which will be mainly contributed to defined benefit

pension plans in Japan, Switzerland and the U.K. This amount

represents the legally mandated minimum contributions. Financial

market performance in 2012 could increase the legally mandated

minimum contribution in certain countries which require monthly or

daily remeasurement of the funded status. The company could also

elect to contribute more than the legally mandated amount based

on market conditions or other factors.

Nonpension Postretirement Benefit Plans

The company contributed $362 million and $363 million to the

nonpension postretirement benefit plans during the years ended

December 31, 2011 and 2010. These contribution amounts exclude

the Medicare-related subsidy discussed on page 134.