ADT 2002 Annual Report Download - page 166

Download and view the complete annual report

Please find page 166 of the 2002 ADT annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

-

178

-

179

-

180

-

181

-

182

|

|

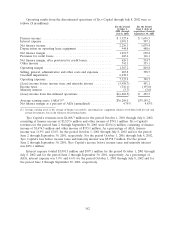

Management’s objective in performing the SFAS 142 first step analysis was to obtain relevant

market-based data to calculate the estimated fair value of CIT as of March 31, 2002 based on its

projected earnings and market factors expected to be used by market participants in ascribing value to

CIT in the planned separation of CIT from Tyco. Management obtained relevant market data from our

financial advisors regarding the range of price to earnings multiples and market condition discounts

applicable to CIT as of March 31, 2002 and applied these market data to CIT’s projected annual

earnings as of March 31, 2002 to calculate an estimated fair value and any resulting goodwill

impairment. The estimated fair value was compared to the corresponding carrying value of CIT at

March 31, 2002. As a result, we recorded a $4,512.7 million impairment charge as of March 31, 2002,

which is included in discontinued operations.

SFAS 142 requires a second step analysis whenever a reporting unit’s book value exceeds estimated

fair value. This analysis requires that we estimate the fair value of the reporting unit’s individual assets

and liabilities to complete the analysis of goodwill as of March 31, 2002. We completed this second step

analysis for CIT during the quarter ended June 30, 2002 and, as a result, recorded an additional

goodwill impairment of $132.0 million. During the June 30, 2002 quarter, CIT experienced further

credit downgrades and the business environment and other factors continued to negatively impact the

likely proceeds of the IPO. As a result, we performed another first step and second step analysis as of

June 30, 2002 in a manner consistent with the March 2002 process described above. Each of these

analyses was based upon updated market data at June 30, 2002 and through the period immediately

following the IPO, including the IPO proceeds. These analyses resulted in a goodwill impairment of

$1,867.0 million, which is also included in discontinued operations as of June 30, 2002. We also

recorded an additional impairment charge of $126.4 million in order to write-down its investment in

CIT to fair value for a total CIT goodwill impairment charge of $2,125.4 million for the quarter ended

June 30, 2002. This write-down was based upon net IPO proceeds of approximately $4.4 billion, after

deducting estimated out of pocket expenses, and is included in the $6,282.5 million loss from

discontinued operations. During the fourth quarter of fiscal 2002, Tyco recorded a loss on the sale of

Tyco Capital of $58.8 million.

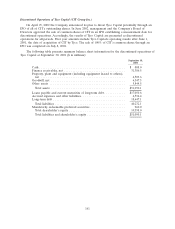

Liquidity and Capital Resources

The following table summarizes the sources of our cash flow from operating activities and the use

of a portion of that cash in our operations in fiscal 2002, fiscal 2001 and fiscal 2000. We refer to the

net amount of cash generated from operating activities, less capital expenditures, dividends and

increases or decreases associated with the sale of accounts receivable program, as ‘‘free cash flow.’’

Management believes operating cash flow and free cash flow are important measures of operating

performance. However, free cash flow as determined below is not a measure of financial performance

under GAAP, should not be considered a substitute for cash flows from operating activities as

determined in accordance with GAAP as a measure of liquidity, and may not be comparable to

similarly titled measures reported by other companies.

164