SunTrust 2011 Annual Report Download - page 98

Download and view the complete annual report

Please find page 98 of the 2011 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

|

|

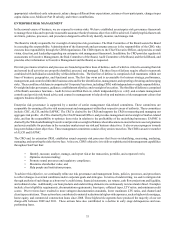

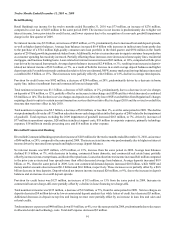

82

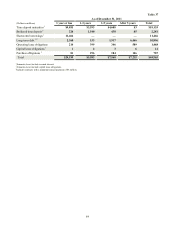

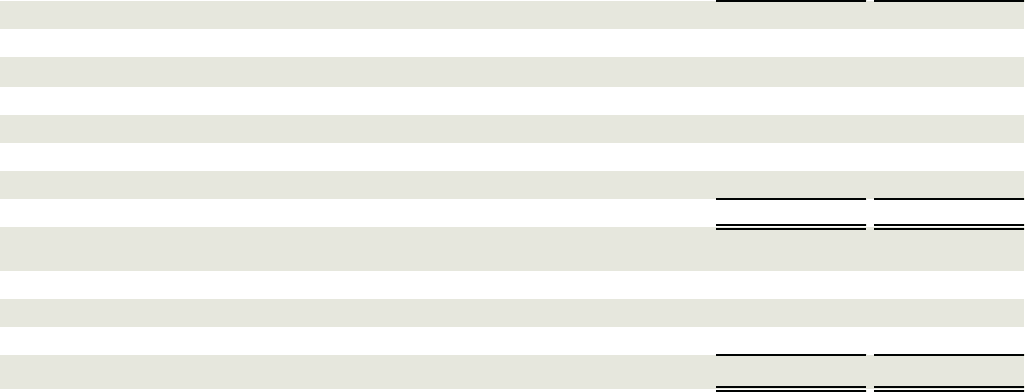

Unfunded Lending Commitments

(Dollars in millions)

Unused lines of credit:

Commercial

Mortgage commitments 1

Home equity lines

Commercial real estate

CP conduit

Credit card

Total unused lines of credit

Letters of credit:

Financial standby

Performance standby

Commercial

Total letters of credit

December 31,

2011

$35,685

7,833

12,730

1,465

765

3,526

$62,004

$5,081

70

55

$5,206

Table 36

December 31,

2010

$34,363

9,159

13,557

1,579

1,091

3,561

$63,310

$6,263

108

68

$6,439

1Includes IRLC contracts with notional balances of $4.9 billion and $4.2 billion as of December 31, 2011 and 2010, respectively.

Other Market Risk

Other sources of market risk include the risk associated with holding residential and commercial mortgage loans prior to selling

them into the secondary market, commitments to clients to make mortgage loans that will be sold to the secondary market, and

our investment in MSRs. We manage the risks associated with the residential and commercial mortgage loans classified as held

for sale (i.e., the warehouse) and our IRLCs on residential loans intended for sale. The warehouses and IRLCs consist primarily

of fixed and adjustable rate single family residential and commercial real estate. The risk associated with the warehouses and

IRLCs is the potential change in interest rates between the time the customer locks in the rate on the anticipated loan and the time

the loan is sold on the secondary market, which is typically 60-150 days.

We manage interest rate risk predominantly with interest rate swaps, futures, and forward sale agreements, where the changes in

value of the instruments substantially offset the changes in value of the warehouse and the IRLCs. The IRLCs on residential

mortgage loans intended for sale are classified as free standing derivative financial instruments and are not designated as hedge

accounting relationships.

MSRs are the present value of future net cash flows that are expected to be received from the mortgage servicing portfolio. The

value of MSRs is highly dependent upon the assumed prepayment speed of the mortgage servicing portfolio which is driven by

the level of certain key interest rates, primarily the 30-year current coupon par mortgage rate. Future expected net cash flows from

servicing a loan in the mortgage servicing portfolio would not be realized if the loan pays off earlier than anticipated. The average

prepayment speed for 2011 remained relatively unchanged compared with 2010. There was a slight increase in prepayments toward

the end of the year as mortgage interest rates declined.

MSRs, which are carried at fair value, totaled $921 million and $1.4 billion as of December 31, 2011 and 2010, respectively, are

managed within established risk limits and are monitored as part of various governance processes. We recorded decreases of $733

million and $513 million in the fair value of our MSRs for the years ended December 31, 2011 and 2010, respectively. Increases

or decreases in fair value include the decay resulting from the realization of expected monthly net servicing cash flows. For the

years ended December 31, 2011 and 2010, we originated MSRs with fair values at the time of origination of $224 million and

$289 million, respectively. New originations during 2011 more than offset the decrease in MSR value attributed to decay. An all-

time low in mortgage rates accounted for the majority of the decline in fair value of our MSRs during 2011. Also contributing $38

million to the decline in the fair value of MSRs was an increase in prepayment assumptions attributable to anticipated refinancing

activity from the HARP 2.0 program.

For the years ended December 31, 2011 and 2010, we recorded losses related to MSRs of $161 million and $69 million (including

decay of $200 million and $240 million), respectively, inclusive of the mark to market adjustments on the related hedges. We

continue to evaluate the impact that the Consent Order may have, and we currently do not expect the impact to be material unless

third party price indications reflect lower market valuations.