SunTrust 2011 Annual Report Download - page 78

Download and view the complete annual report

Please find page 78 of the 2011 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

|

|

62

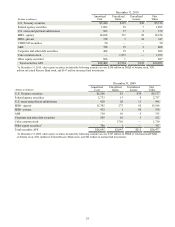

to the current U.S. regulatory standards. Also, Tier 1 Common and Tier 1 Capital ratios continue to be well above both Basel

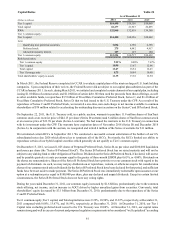

I and Basel III regulatory requirements.

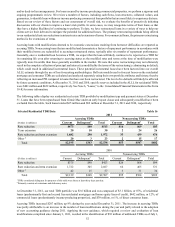

During the year ended December 31, 2011, we declared and paid common dividends totaling $64 million, or $0.12 per common

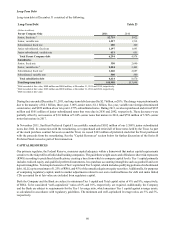

share, compared with $20 million, or $0.04 per common share during the same period in 2010. Additionally, we declared and

paid dividends payable of $7 million for both years ended December 31, 2011 and 2010 on our Series A Preferred Stock.

Further, during the years ended December 31, 2011 and 2010, we declared and paid dividends payable of $60 million and

$242 million, respectively, to the U.S. Treasury on the Series C and D Preferred Stock.

Our Board approved an increase in the quarterly dividend to $0.05 per share, which was paid on September 15, 2011, to

shareholders of record at the close of business on September 1, 2011. However, we remain subject to certain restrictions on

our ability to increase our dividend. If we increase our quarterly dividend above $0.54 per share prior to the tenth anniversary

of our participation in the CPP, then the exercise price and the number of shares to be issued upon exercise of the warrants

issued in connection with our participation in the CPP will be proportionately adjusted. See Part I, Item 1A, “Risk Factors,”

in this Form 10-K for additional considerations regarding the level of future dividends. Additionally, limits exist on the ability

of the Bank to pay dividends to the Parent Company. Substantially all of our retained earnings are undistributed earnings of

the Bank, which are restricted by various regulations administered by federal and state bank regulatory authorities. There was

no capacity for payment of cash dividends to the Parent Company under these regulations at December 31, 2011. However,

at January 1, 2012, retained earnings of the Bank available for payment of cash dividends to the Parent Company under these

regulations totaled approximately $697 million.

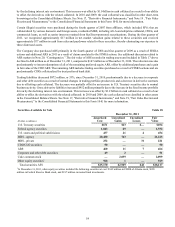

Basel III

In September 2010, the BCBS announced new regulatory capital requirements (commonly referred to as “Basel III”) aimed

at substantially strengthening existing capital requirements, through a combination of higher minimum capital requirements,

new capital conservation buffers, and more stringent definitions of capital and exposure. Basel III would impose a new "Tier

1 common" equity requirement of 7%, comprised of a minimum of 4.5% plus a capital conservation buffer of 2.5%. The

BCBS has also stated that from time to time it may require an additional, counter-cyclical capital buffer on top of Basel III

standards. As this would only be included in periods of above-average lending activity, it is not included in our calculations.

It is anticipated that U.S. regulators will adopt new regulatory capital requirements similar to those proposed by the BCBS.

We monitor our capital structure as to compliance with current regulatory and prescribed operating levels and take into account

these new regulations as they are published and become applicable to us in our capital planning.

The composition of our capital elements is likely to be impacted by the Dodd-Frank Act in at least two ways over the next

several years. First, the Dodd-Frank Act authorizes the Federal Reserve to enact “prudential” capital requirements which

may require greater capital levels than presently required and which may vary among financial institutions based on size, risk,

complexity, and other factors. We expect the Federal Reserve to use this authority to implement the Basel III capital

requirements, although this authority is not limited to the Basel III requirements. Second, a portion of the Dodd-Frank Act

(sometimes referred to as the Collins Amendment) directs the Federal Reserve to adopt new capital requirements for certain

bank holding companies, including us, which are at least as stringent as those applicable to insured depositary institutions,

such as SunTrust Bank. We expect that the Federal Reserve will apply these to us over a 3-year period beginning January 1,

2013 and that, as a result, as of December 31, 2015, approximately $1.9 billion in principal amount of Parent Company trust

preferred and other hybrid capital securities currently outstanding, will no longer qualify for Tier 1 capital treatment at that

time. We will consider changes to our capital structure as these new regulations are published and become applicable to us.

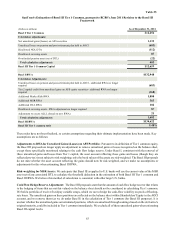

The concept of Tier 1 common equity, the portion of Tier 1 capital that is common equity, was first introduced in the 2009

SCAP. Our regulator, rather than GAAP, defines Tier 1 common equity and the Tier 1 common equity ratio. As a result, our

calculation of these measures may be different than those of other financial service companies who calculate them. However,

Tier 1 common equity and the Tier 1 common equity ratio continue to be important factors which regulators examine in

evaluating financial institutions; therefore, we present these measures to allow for evaluations of our capital.

The transition period for banks to meet the revised common equity requirement will begin in 2013, with full implementation

in 2019. Details for estimation of the Basel III Tier 1 common equity ratio are as follows: