SunTrust 2011 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2011 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

|

|

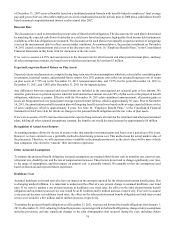

67

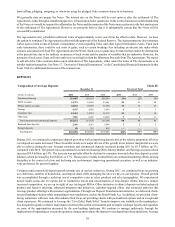

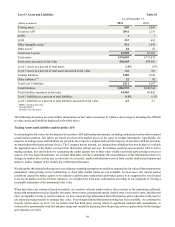

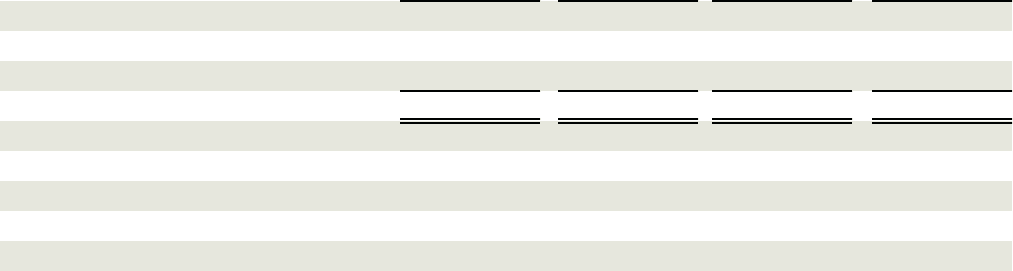

The previous table presented historical information regarding the population of defaulted loans and repurchase request rates. The

following table presents historical information regarding the repurchase rates and loss severity for loans sold between 2006 to

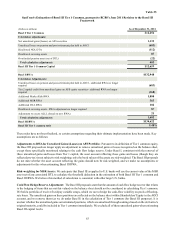

2008.

Repurchase Rates and Loss Severity

(Dollars in billions)

Repurchased

Cured

Pending

Total repurchase requests received

Repurchase rate

Losses recognized

Loss severity

Loss severity last 12 months

2006

$0.8

0.7

0.1

$1.6

53%

$0.3

42%

56%

2007

$1.2

0.8

0.3

$2.3

61%

$0.6

51%

57%

2008

$0.2

0.2

0.1

$0.5

60%

$0.1

48%

48%

Table 28

Total

$2.2

1.7

0.5

$4.4

58%

$1.0

47%

55%

Some of the assumptions used in the reserve process contain a level of uncertainty since they are largely derived from historical

experience that has been limited and highly variable. As such, provision expense will vary as the estimates used to measure the

liability continue to be updated based on the level of repurchase requests, the latest experience gained on repurchase requests, and

other relevant facts and circumstances. One of the most critical and judgmental assumptions is the repurchase request rate because

it requires us to make assessments regarding the actions that will be taken by third party investors in the context of the highly

variable history we have experienced with their current volume and timing of requests.

Once we estimate the level of requests that we expect to receive by vintage, we apply factors for the probability that a loan will

be repurchased as well as the loss severity expected. Our life-to-date repurchase rates are consistent with future expectations;

however, given changes in housing prices over the past several years, we believe the loss severity over the past 12 months will be

more indicative of our future loss severity rate.

Our current estimated liability for contingent losses related to loans sold was $320 million as of December 31, 2011. The liability

is recorded in other liabilities in the Consolidated Balance Sheets, and the related repurchase provision is recognized in mortgage

production related (loss)/income in the Consolidated Statements of Income/(Loss). Various factors could potentially impact the

accuracy of the assumptions underlying our mortgage repurchase reserve estimate. As previously discussed, the level of repurchase

requests we receive is dependent upon the actions of third parties and could differ from the assumptions that we have made.

Delinquency levels, delinquency roll rates, and our loss severity assumptions are all highly dependent upon economic factors

including changes in real estate values and unemployment levels which are, by nature, difficult to predict. Loss severity assumptions

could also be negatively impacted by delays in the foreclosure process which is a heightened risk in some of the states where our

loans sold were originated. Approximately 16% of the population of total loans sold between January 1, 2006 and December 31,

2008 were sold to non-agency investors, some in the form of securitizations. Due to the nature of these structures and the indirect

ownership interests, the potential exists that investors, over time, will become more successful in forcing additional repurchase

demands. While we have used the best information available in estimating the mortgage repurchase reserve liability, these and

other factors, along with the discovery of additional information in the future could result in changes in our assumptions which

could materially impact our results of operations.

See "Noninterest Income" in this MD&A and Note 18, “Reinsurance Arrangements and Guarantees - Loan Sales,” to the

Consolidated Financial Statements in this Form 10-K for further discussion.

Legal and Regulatory Matters

We are parties to numerous claims and lawsuits arising in the course of our normal business activities, some of which involve

claims for substantial amounts, and the outcomes of which are not within our complete control or may not be known for prolonged

periods of time. Management is required to assess the probability of loss and amount of such loss, if any, in preparing our financial

statements.