SunTrust 2011 Annual Report Download - page 192

Download and view the complete annual report

Please find page 192 of the 2011 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

|

|

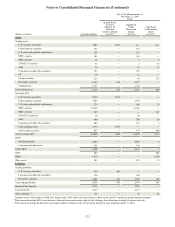

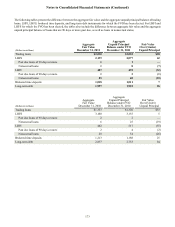

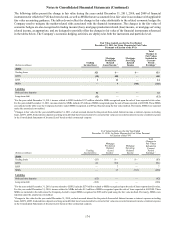

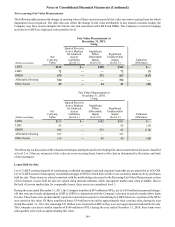

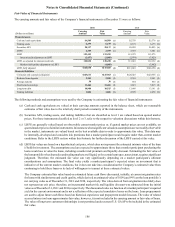

Notes to Consolidated Financial Statements (Continued)

176

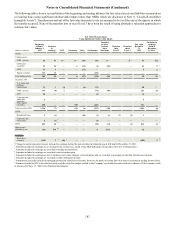

Level 3 municipal securities includes ARS purchased since the auction rate market began failing in February 2008 and

have been considered level 3 securities due to the significant decrease in the volume and level of activity in these markets,

which has necessitated the use of significant unobservable inputs into the Company’s valuations. Municipal ARS are

classified as securities AFS. These securities were valued using comparisons to similar ARS for which auctions are

currently successful and/or to longer term, non-ARS issued by similar municipalities. The Company also evaluated the

relative strength of the municipality and made appropriate downward adjustments in price based on the credit rating of

the municipality as well as the relative financial strength of the insurer on those bonds. Although auctions for several

municipal ARS have been operating successfully, ARS owned by the Company at December 31, 2011 continued to be

classified as level 3 as they are those ARS for which the auctions continued to fail; accordingly, due to the uncertainty

around the success rates for auctions and the absence of any successful auctions for these identical securities, the Company

continued to price the ARS below par.

Level 3 AFS municipal bond securities also include bonds that are only redeemable with the issuer at par and cannot be

traded in the market. As such, no significant observable market data for these instruments is available. In order to estimate

pricing on these securities, the Company utilized a third party municipal bond yield curve for the lowest investment grade

bonds (BBB rated) and priced each bond based on the yield associated with that maturity.

MBS – agency

MBS – agency includes pass-through securities and collateralized mortgage obligations issued by GSEs and U.S.

government agencies, such as Fannie Mae, Freddie Mac, and Ginnie Mae. Each security contains a guarantee by the

issuing GSE or agency. For agency MBS, the Company estimated fair value based on pricing from observable trading

activity for similar securities or obtained fair values from a third party pricing service; accordingly, the Company has

classified these as level 2.

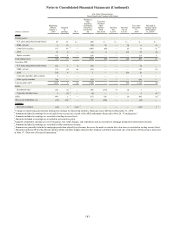

MBS – private

Private MBS includes purchased interests in third party securitizations as well as retained interests in Company-sponsored

securitizations of residential mortgages. In 2010, the Company also had approximately $9 million of private label CMBS

in trading assets that were received as part of a SIV liquidation (see CDO/CLO discussion below). Generally, the Company

attempts to obtain pricing for its securities from an independent pricing service or third party brokers who have experience

in valuing certain investments. This pricing may be used as either direct support for the Company’s valuations or used

to validate outputs from its own proprietary models. The Company evaluates third party pricing to determine the

reasonableness of the information relative to changes in market data, such as any recent trades, market information

received from outside market participants and analysts, and/or changes in the underlying collateral performance. For a

de minimis amount of private MBS, the Company uses industry-standard or proprietary models to estimate fair value

and considers assumptions that are generally not observable in the current markets or that are not specific to the securities

that the Company owns, such as relevant market indices that correlate to the underlying collateral, prepayment speeds,

default rates, loss severity rates, and discount rates. As liquidity returns to these markets, the Company has seen more

pricing information from third parties and a reduction in the need to use pricing models to estimate fair value. Even

though limited third party pricing has been available, the Company continued to classify private MBS as level 3, as the

Company believes that this third party pricing relied on significant unobservable assumptions, as evidenced by a

persistently wide bid-ask price range and variability in pricing from the pricing services, particularly for the vintage and

exposures held by the Company.

For the private CMBS held at December 31, 2010, the Company was able to obtain pricing information as part of the

foreclosure sale at liquidation and was also able to obtain at least two different pricing sources that were within narrow

price range. As such, the Company classified these securities as level 2. Certain vintages of private RMBS have suffered

from deterioration in credit quality leading to downgrades. At December 31, 2011, the Company's private RMBS contained

2006 to 2007 vintage securities AFS and trading securities. At December 31, 2010, private RMBS also included 2003

vintage securities classified as AFS. All but a de minimis amount of the 2006 and 2007 vintage securities AFS and trading

securities had been downgraded to non-investment grade levels by at least one nationally recognized rating agency. The

vast majority of these securities had high investment grade ratings at the time of origination or purchase. The 2006 to

2007 vintage collateral is predominantly comprised of prime jumbo fixed and floating rate loans. The 2003 vintage

securities are interests retained from a securitization of prime first lien fixed and floating rate loans and are primarily all

investment grade rated, with the exception of a small amount of support bonds. The majority of these securities had

maintained their original ratings, with a small amount of upgrades and only one bond downgraded since inception of the

deal. During 2011, the Company's remaining interests of $49 million in the 2003 securitization were liquidated through

the exercise of the Company's clean up call rights on the underlying collateral. See Note 11, "Certain Transfers of Financial

Assets and Variable Interest Entities."