SunTrust 2011 Annual Report Download - page 58

Download and view the complete annual report

Please find page 58 of the 2011 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

|

|

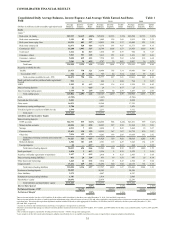

42

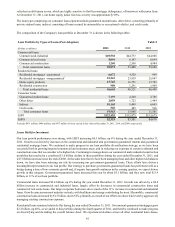

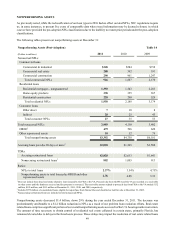

refreshed credit bureau scores, which are highly sensitive to first lien mortgage delinquency, of borrowers with junior liens.

At December 31, 2011, our home equity junior lien loss severity was approximately 90%.

The loan types comprising our consumer loan segment include guaranteed student loans, other direct, consisting primarily of

private student loans, indirect, consisting of loans secured by automobiles or recreational vehicles, and credit cards.

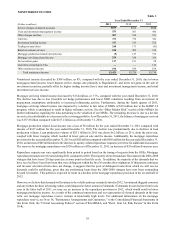

The composition of the Company's loan portfolio at December 31 is shown in the following tables:

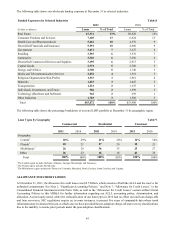

Loan Portfolio by Types of Loans (Post-Adoption)

(Dollars in millions)

Commercial loans:

Commercial & industrial

Commercial real estate

Commercial construction

Total commercial loans

Residential loans:

Residential mortgages - guaranteed

Residential mortgages - nonguaranteed1

Home equity products

Residential construction

Total residential loans

Consumer loans:

Guaranteed student loans

Other direct

Indirect

Credit cards

Total consumer loans

LHFI

LHFS

2011

$49,538

5,094

1,240

55,872

6,672

23,243

15,765

980

46,660

7,199

2,059

10,165

540

19,963

$122,495

$2,353

2010

$44,753

6,167

2,568

53,488

4,520

23,959

16,751

1,291

46,521

4,260

1,722

9,499

485

15,966

$115,975

$3,501

Table 5

2009

$44,008

6,694

4,984

55,686

949

25,847

17,783

1,909

46,488

2,786

1,484

6,665

566

11,501

$113,675

$4,670

1Includes $431 million, $488 million, and $437 million of loans carried at fair value at December 31, 2011, 2010, and 2009, respectively.

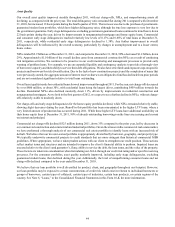

Loans Held for Investment

Our loan growth performance was strong, with LHFI increasing $6.5 billion, up 6% during the year ended December 31,

2011. Growth was driven by increases in the commercial and industrial and government-guaranteed student and guaranteed

residential mortgage loans. We continued to make progress in our loan portfolio diversification strategy, as we have been

successful both in growing targeted commercial and consumer areas, and in reducing our exposure to certain residential and

construction areas that we consider to be higher risk. Continuing to manage down our commercial and residential construction

portfolios has resulted in a combined $1.6 billion decline in these portfolios during the year ended December 31, 2011, and

a $7.8 billion decrease since the end of 2008. At the same time that we have been managing these and other higher risk balances

down, we have also been reducing our risk by increasing our government-guaranteed loans. These efforts have driven a

meaningful improvement in our risk profile. Our strategy to purchase government-guaranteed loans has performed well as a

bridge during a time of low economic growth and, if organic loan growth continues in the coming quarters, we expect slower

growth in this category. Government-guaranteed loans increased this year by about $5.1 billion, and they now total $13.9

billion, or 11% of our loan portfolio.

Commercial loans increased $2.4 billion, up 4% during the year ended December 31, 2011. Growth was driven by a $4.8

billion increase in commercial and industrial loans, largely offset by decreases in commercial construction loans and

commercial real estate loans. Our larger corporate borrowers drove much of the 11% increase in commercial and industrial

loans. Growth came across most industry verticals, with healthcare and energy contributing the most. Meanwhile, commercial

construction loans decreased by $1.3 billion, down 52%, primarily as a result of our efforts to reduce risk levels by aggressively

managing existing construction exposure.

Residential loans remained relatively flat during the year ended December 31, 2011. Government-guaranteed mortgages grew

$2.2 billion, up 48%, as we added to this portfolio during the fourth quarter of 2011, and thereby continued to make progress

on diversifying and de-risking the overall balance sheet. We experienced declines across all other residential loan classes,