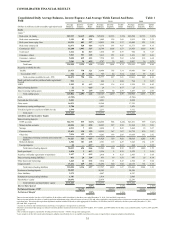

SunTrust 2011 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 2011 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

|

|

41

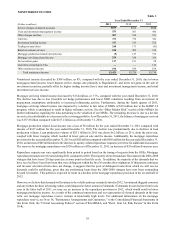

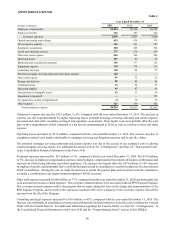

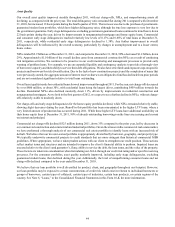

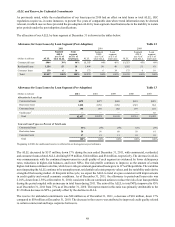

Regulatory assessments expense increased by $35 million, or 13%, compared with the year ended December 31, 2010. The

increase was the result of the change in the assessment base for FDIC insurance premiums that took effect at the beginning

of the second quarter of 2011.

Net losses on debt extinguishment decreased by $73 million, compared with the year ended December 31, 2010. Net losses

on debt extinguishment in the prior year were primarily due to early termination fees on the extinguishment of $1.7 billion

in FHLB borrowings, as well as the fees paid to repurchase $750 million of our debt in a tender offer.

Other real estate expense decreased by $36 million, or 12%, compared with the year ended December 31, 2010. The decrease

was predominantly due to less loss provisioning as sales of owned properties increased while inflows of new properties

decreased. Over time, as the economic environment improves, we expect that other real estate expense will continue to improve,

but will likely remain elevated compared with the levels realized prior to the economic recession.

PROVISION FOR INCOME TAXES

The provision for income taxes includes both federal and state income taxes. For the year ended December 31, 2011, the

provision for income taxes was $79 million, resulting in an effective tax rate of 10.9%. The effective tax rate was primarily

a result of positive pre-tax earnings adjusted for net favorable permanent tax items, such as interest income from lending to

tax-exempt entities and federal tax credits from community reinvestment activities. For the year ended December 31, 2010,

we had an income tax benefit of $185 million which was primarily driven by the net favorable permanent tax items significantly

exceeding positive pre-tax earnings. See additional discussion related to the provision for income taxes in Note 15, “Income

Taxes,” to the Consolidated Financial Statements in this Form 10-K.

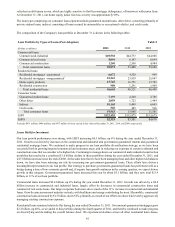

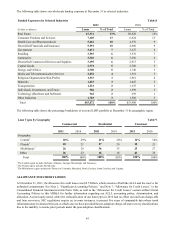

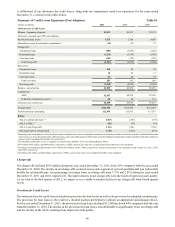

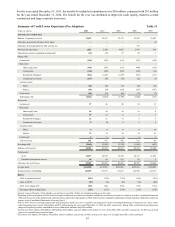

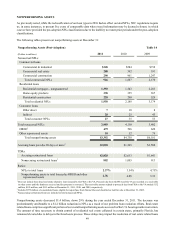

LOANS

In 2010, we adopted accounting guidance that requires additional disclosures about the credit quality of our loan portfolios

and the credit reserves held against them. These disclosures are intended to 1) describe the nature of credit risk inherent in

our loan portfolio, 2) provide information on how we analyze and assess that risk in arriving at an adequate and appropriate

ALLL, and 3) explain the changes in the ALLL and reasons for those changes. Additionally, the disclosures are required to

be made on a disaggregated basis by loan portfolio segment and/or by type of loan. A portfolio segment is defined as the level

at which we develop and document our method for determining our ALLL. Loan types are further categorizations of our

portfolio segments. In conjunction with adopting the accounting guidance, we adjusted 2009 loan classifications to align with

post-adoption loan classifications. While the reclassification had no effect on the carrying value of our LHFI or LHFS, SEC

regulations require us, in some instances, to present five years of comparable data where trend information may be deemed

relevant, in which case we have provided the pre-adoption loan classifications due to the inability to restate all prior periods

under the post-adoption loan classifications.

Under the post-adoption classification, we report our loan portfolio in three segments: commercial, residential, and consumer.

Loans are assigned to these segments based upon the type of borrower, collateral, and/or our underlying credit management

processes. Additionally, within each segment, we have identified loan types, or classes, which further identify loans based

upon common risk characteristics.

The commercial and industrial loan type includes loans secured by owner-occupied properties, corporate credit cards and

other wholesale lending activities. Commercial real estate and commercial construction loan types are based on investor

exposures where repayment is largely dependent upon the operation, refinance, or sale of the underlying real estate. Commercial

and construction loans secured by owner-occupied properties are classified as commercial and industrial loans, as the primary

source of loan repayment for owner-occupied properties is business income and not real estate operations.

Residential mortgages consist of loans secured by 1-4 family homes, mostly prime first-lien loans, both guaranteed and

nonguaranteed. Residential construction loans include residential lot loans and construction-to-perm loans. Home equity

products consist of equity lines of credit and closed-end equity loans that may be in either a first lien or junior lien position.

At December 31, 2011, 30% of our home equity products were in a first lien position and 70% were in a junior lien position.

For home equity products in a junior lien position, we service 32% of the loans that are senior to the home equity product.

Only a small percentage of home equity lines are scheduled to convert to amortizing in 2012 and 2013, with 90% of home

equity line balances scheduled to convert to amortization in 2014 or later. It should be noted that a majority of accounts do

not convert to amortizing. Based on historical trends, within 12 months of the end of their draw period, more than 75% of

accounts, and approximately 65% of accounts with a balance, closed or refinanced before, or soon after converting.We perform

credit management activities on home equity accounts to limit our loss exposure. These activities result in the suspension of

available credit of most home equity junior lien accounts when the first lien position is delinquent, including when the junior

lien is still current. We do not actively monitor the first lien delinquency status on an on-going basis when we do not own or

service the first lien position beyond the initial notification of the first lien becoming delinquent. However, we actively monitor