SunTrust 2011 Annual Report Download - page 173

Download and view the complete annual report

Please find page 173 of the 2011 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

|

|

Notes to Consolidated Financial Statements (Continued)

157

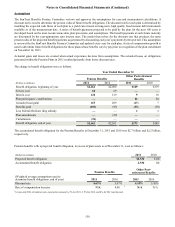

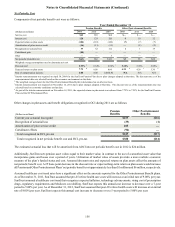

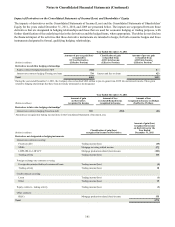

Due to changing medical inflation, it is important to understand the effect of a one-percent point change in assumed healthcare

cost trend rates. These amounts are shown below:

(Dollars in millions)

Effect on Other Postretirement Benefit obligation

Effect on total service and interest cost

1% Increase

$11

1

1% Decrease

$10

1

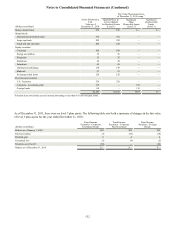

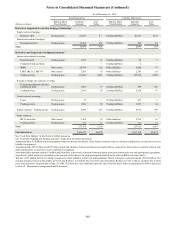

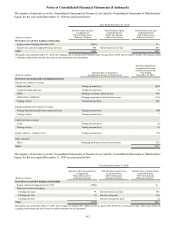

NOTE 17 - DERIVATIVE FINANCIAL INSTRUMENTS

The Company enters into various derivative financial instruments, both in a dealer capacity to facilitate client transactions and as

an end user as a risk management tool. When derivatives have been entered into with clients, the Company generally manages

the risk associated with these derivatives within the framework of its VAR approach that monitors total exposure daily and seeks

to manage the exposure on an overall basis. Derivatives are used as a risk management tool to hedge the Company’s balance sheet

exposure to changes in identified cash flow and fair value risks, either economically or in accordance with hedge accounting

provisions. The Company’s Corporate Treasury function is responsible for employing the various hedge accounting strategies to

manage these objectives and all derivative activities are monitored by ALCO. The Company may also enter into derivatives, on

a limited basis, in consideration of trading opportunities in the market. Additionally, as a normal part of its operations, the Company

enters into IRLCs on mortgage loans that are accounted for as freestanding derivatives and has certain contracts containing

embedded derivatives that are carried, in their entirety, at fair value. All freestanding derivatives and any embedded derivatives

that the Company bifurcates from the host contracts are carried at fair value in the Consolidated Balance Sheets in trading assets,

other assets, trading liabilities, or other liabilities. The associated gains and losses are either recognized in AOCI, net of tax, or

within the Consolidated Statements of Income/(Loss) depending upon the use and designation of the derivatives.

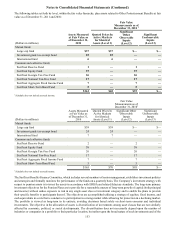

Credit and Market Risk Associated with Derivatives

Derivatives expose the Company to credit risk. The Company minimizes the credit risk of derivatives by entering into transactions

with high credit-quality counterparties with defined exposure limits that are reviewed periodically by the Company’s Credit Risk

Management division. The Company’s derivatives may also be governed by an ISDA, and depending on the nature of the derivative,

bilateral collateral agreements are typically in place as well. When the Company has more than one outstanding derivative

transaction with a single counterparty and there exists a legally enforceable master netting agreement with that counterparty, the

Company considers its exposure to the counterparty to be the net market value of all positions with that counterparty, if such net

value is an asset to the Company, and zero, if such net value is a liability to the Company. As of December 31, 2011, net derivative

asset positions to which the Company was exposed to risk of its counterparties were $2.4 billion, representing the net of $3.6

billion in net derivative gains, offset by counterparty where formal netting arrangements exist, adjusted for collateral of $1.2 billion

that the Company holds in relation to these gain positions. As of December 31, 2010, net derivative asset positions to which the

Company was exposed to risk of its counterparties were $1.6 billion, representing the net of $2.8 billion in net derivative gains

by counterparty, offset by counterparty where formal netting arrangements exist, adjusted for collateral of $1.2 billion that the

Company holds in relation to these gain positions.

Derivatives also expose the Company to market risk. Market risk is the adverse effect that a change in market factors, such as

interest rates, currency rates, equity prices, or implied volatility, has on the value of a derivative. The Company manages the market

risk associated with its derivatives by establishing and monitoring limits on the types and degree of risk that may be undertaken.

The Company continually measures this risk associated with its derivatives designated as trading instruments using a VAR

methodology.

Derivative instruments are primarily transacted in the institutional dealer market and priced with observable market assumptions

at a mid-market valuation point, with appropriate valuation adjustments for liquidity and credit risk. For purposes of valuation

adjustments to its derivative positions, the Company has evaluated liquidity premiums that may be demanded by market participants,

as well as the credit risk of its counterparties and its own credit. The Company has considered factors such as the likelihood of

default by itself and its counterparties, its net exposures, and remaining maturities in determining the appropriate fair value

adjustments to recognize. Generally, the expected loss of each counterparty is estimated using the Company’s proprietary internal

risk rating system. The risk rating system utilizes counterparty-specific probabilities of default and LGD estimates to derive the

expected loss. For counterparties that are rated by national rating agencies, those ratings are also considered in estimating the

credit risk. Additionally, counterparty exposure is evaluated by offsetting positions that are subject to master netting arrangements,

as well as considering the amount of marketable collateral securing the position. All counterparties are explicitly approved, as are

defined exposure limits. Counterparties are regularly reviewed and appropriate business action is taken to adjust the exposure to

certain counterparties, as necessary. This approach is also used by the Company to estimate its own credit risk on derivative liability

positions. The Company adjusted the net fair value of its derivative contracts for estimates of net counterparty credit risk by

approximately $36 million and $33 million as of December 31, 2011 and 2010, respectively.