SunTrust 2011 Annual Report Download - page 184

Download and view the complete annual report

Please find page 184 of the 2011 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

|

|

Notes to Consolidated Financial Statements (Continued)

168

related repurchase provision is recognized in mortgage production related (loss)/income in the Consolidated Statements of

Income/(Loss).

A significant degree of judgment is used to estimate the mortgage repurchase liability. This estimation process is inherently

uncertain and subject to imprecision; consequently, there is a range of reasonably possible loss in excess of the recorded

repurchase liability. Based on an analysis of the assumptions used to estimate the repurchase liability related to loans sold prior

to 2009, the Company estimates that it is reasonably possible that the estimated liability, as of December 31, 2011, could exceed

the current repurchase liability by $0 to $700 million. This estimate is subject to revision due to changes in borrower default

levels, investor request criteria and behavior, repurchase rates, and home values. This estimate of reasonably possible

incremental loss does not pertain to non-agency investors or to loans sold after 2008 due to the limited amount of historical

repurchase request and loss experience the Company has realized on these more recent vintages; therefore, the Company is

unable to estimate a reasonably possible range of loss for loans sold to non-agency investors or for loans sold subsequent to

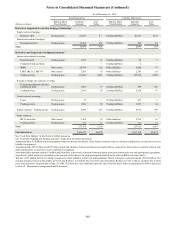

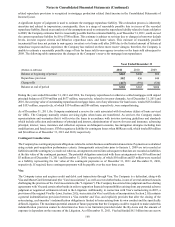

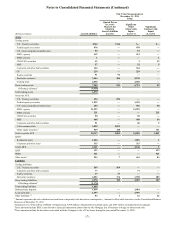

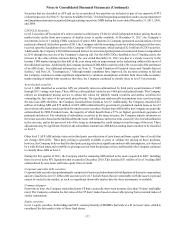

2008. The following table summarizes the changes in the Company’s reserve for mortgage loan repurchases:

(Dollars in millions)

Balance at beginning of period

Repurchase provision

Charge-offs

Balance at end of period

Year Ended December 31

2011

$265

502

(447)

$320

2010

$200

456

(391)

$265

2009

$92

444

(336)

$200

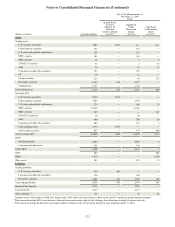

During the years ended December 31, 2011 and 2010, the Company repurchased or otherwise settled mortgages with unpaid

principal balances of $789 million and $677 million, respectively, related to investor demands. As of December 31, 2011 and

2010, the carrying value of outstanding repurchased mortgage loans, net of any allowance for loan losses, totaled $252 million

and $153 million, respectively, of which $134 million and $86 million, respectively, were nonperforming.

As of December 31, 2011, the Company maintained a reserve for costs associated with foreclosure delays of loans serviced

for GSEs. The Company normally retains servicing rights when loans are transferred. As servicer, the Company makes

representations and warranties that it will service the loans in accordance with investor servicing guidelines and standards

which include collection and remittance of principal and interest, administration of escrow for taxes and insurance, advancing

principal, interest, taxes, insurance and collection expenses on delinquent accounts, loss mitigation strategies including loan

modifications, and foreclosures. STM recognizes a liability for contingent losses when MSRs are sold, which totaled $8 million

and $6 million as of December 31, 2011 and 2010, respectively.

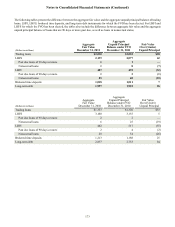

Contingent Consideration

The Company has contingent payment obligations related to certain business combination transactions. Payments are calculated

using certain post-acquisition performance criteria. Arrangements entered into prior to January 1, 2009 are not recorded as

liabilities until the contingency is resolved; whereas, arrangements entered into subsequent to that date are recorded as liabilities

at the fair value of the contingent payment. The potential obligation associated with these arrangements was $10 million and

$5 million as of December 31, 2011 and December 31, 2010, respectively, of which $10 million and $3 million were recorded

as a liability representing the fair value of the contingent payments as of December 31, 2011 and December 31, 2010,

respectively. If required, these contingent payments will be payable over the next three years.

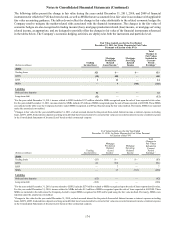

Visa

The Company issues and acquires credit and debit card transactions through Visa. The Company is a defendant, along with

Visa and MasterCard International (the “Card Associations”), as well as several other banks, in one of several antitrust lawsuits

challenging the practices of the Card Associations (the “Litigation”). The Company has entered into judgment and loss sharing

agreements with Visa and certain other banks in order to apportion financial responsibilities arising from any potential adverse

judgment or negotiated settlements related to the Litigation. Additionally, in connection with Visa’s restructuring in 2007, a

provision of the original Visa By-Laws, Section 2.05j, was restated in Visa’s certificate of incorporation. Section 2.05j contains

a general indemnification provision between a Visa member and Visa, and explicitly provides that after the closing of the

restructuring, each member’s indemnification obligation is limited to losses arising from its own conduct and the specifically

defined Litigation. The maximum potential amount of future payments that the Company could be required to make under this

indemnification provision cannot be determined as there is no limitation provided under the By-Laws and the amount of

exposure is dependent on the outcome of the Litigation. As of December 31, 2011, Visa had funded $8.1 billion into an escrow