SunTrust 2011 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2011 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

|

|

48

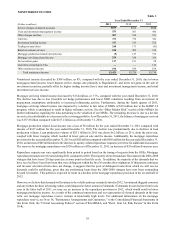

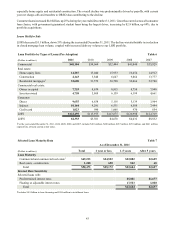

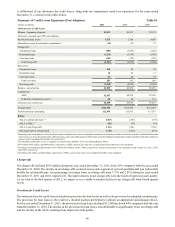

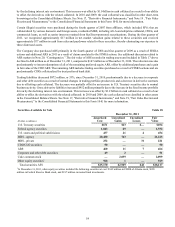

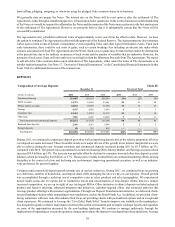

ALLL and Reserve for Unfunded Commitments

As previously noted, while the reclassification of our loan types in 2010 had no effect on total loans or total ALLL, SEC

regulations require us, in some instances, to present five years of comparable data where trend information may be deemed

relevant, in which case we have provided the pre-adoption ALLL by loan segment classifications due to the inability to restate

prior periods under the post-adoption classifications.

The allocation of our ALLL by loan segment at December 31 is shown in the tables below:

Allowance for Loan Losses by Loan Segment (Post-Adoption)

(Dollars in millions)

Commercial loans

Residential loans

Consumer loans

Total

2011

ALLL

$964

1,354

139

$2,457

Segment

ALLL

as a % of

total ALLL

39%

55

6

100%

Loan

segment

as a % of

total loans

46%

38

16

100%

2010

ALLL

$1,303

1,498

173

$2,974

Segment

ALLL

as a % of

total ALLL

44%

50

6

100%

Loan

segment

as a % of

total loans

46%

40

14

100%

2009

ALLL

$1,353

1,592

175

$3,120

Table 12

Segment

ALLL

as a % of

total ALLL

43%

51

6

100%

Loan

segment

as a % of

total loans

49%

41

10

100%

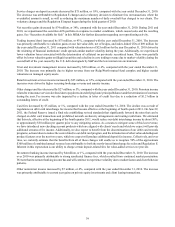

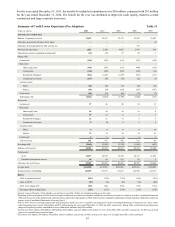

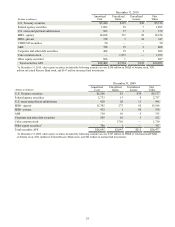

Allowance for Loan Losses by Loan Segment (Pre-Adoption)

(Dollars in millions)

Allocation by Loan Type

Commercial loans

Real estate loans

Consumer loans

Unallocated 1

Total

Year-end Loan Types as a Percent of Total Loans

Commercial loans

Real estate loans

Consumer loans

Total

2011

$479

1,820

158

—

$2,457

33%

50

17

100%

2010

$477

2,238

259

—

$2,974

29%

56

15

100%

2009

$650

2,268

202

—

$3,120

29%

60

11

100%

2008

$631

1,523

197

—

$2,351

32%

58

10

100%

Table 13

2007

$423

664

110

85

$1,282

29%

61

10

100%

1Beginning in 2008, the unallocated reserve is reflected in our homogeneous pool estimates.

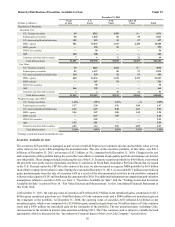

The ALLL decreased by $517 million, down 17% during the year ended December 31, 2011, with commercial, residential,

and consumer loans-related ALLL declining $339 million, $144 million, and $34 million, respectively. The decrease in ALLL

was commensurate with the continued improvement in credit quality of each segment as evidenced by lower delinquency

rates, reductions in higher-risk balances, and lower NPLs. Our risk profile continues to improve, as the amount of certain

higher-risk loans continue to decline, while lower-risk government guaranteed loans grew to 11% of the portfolio. The variables

most impacting the ALLL continue to be unemployment, residential real estate property values, and the variability and relative

strength of the housing market. At this point in the cycle, we expect the ALLL to trend at a pace consistent with improvements

in credit quality and overall economic conditions. As of December 31, 2011, the allowance to period-end loans ratio was

2.01%, down from 2.58% at December 31, 2010, consistent with our continued actions to reduce the risk of our loan portfolio

during the period coupled with an increase in total loans during 2011. The ratio of the ALLL to total NPLs improved to 85%

as of December 31, 2011 from 73% as of December 31, 2010. The improvement in this ratio was primarily attributable to the

$1.2 billion decrease in NPLs, partially offset by the decline in ALLL.

The reserve for unfunded commitments was $48 million as of December 31, 2011, a decrease of $10 million, down 17%

compared to $58 million at December 31, 2010. The decrease in the reserve was attributed to improved credit quality related

to certain commercial and large corporate borrowers.