SunTrust 2011 Annual Report Download - page 181

Download and view the complete annual report

Please find page 181 of the 2011 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

|

|

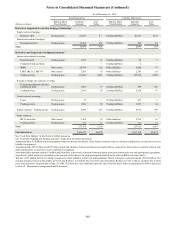

Notes to Consolidated Financial Statements (Continued)

165

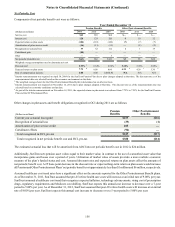

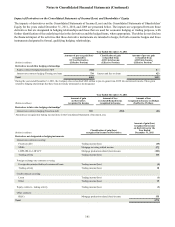

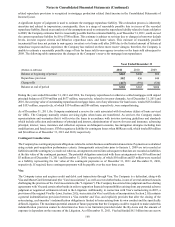

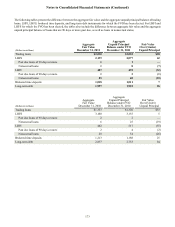

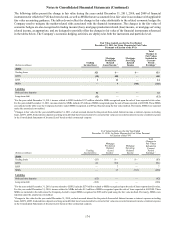

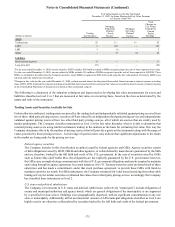

Fair Value Hedges

During 2011, the Company entered into interest rate swap agreements, as part of the Company’s risk management objectives for

hedging its exposure to changes in fair value due to changes in interest rates. These hedging arrangements include converting

Company issued fixed rate senior long-term debt and fixed rate U.S. Treasury securities AFS to floating rates. Consistent with

this objective, the Company reflects the accrued contractual interest on the hedged item and the related swaps as part of current

period interest. There were no components of derivative gains or losses excluded in the Company’s assessment of hedge

effectiveness related to the fair value hedges.

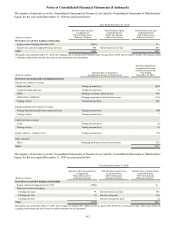

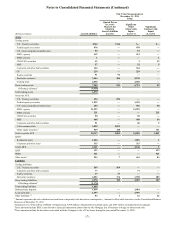

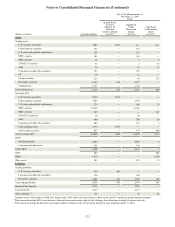

Economic Hedging and Trading Activities

In addition to designated hedging relationships, the Company also enters into derivatives as an end user as a risk management

tool to economically hedge risks associated with certain non-derivative and derivative instruments, along with entering into

derivatives in a trading capacity with its clients.

The primary risks that the Company economically hedges are interest rate risk, foreign exchange risk, and credit risk. Economic

hedging objectives are accomplished by entering into offsetting derivatives either on an individual basis, or collectively on a macro

basis, and generally accomplish the Company’s goal of mitigating the targeted risk. To the extent that specific derivatives are

associated with specific hedged items, the notional amounts, fair values, and gains/(losses) on the derivatives are illustrated in the

tables in this footnote.

• The Company utilizes interest rate derivatives to mitigate exposures from various instruments.

The Company is subject to interest rate risk on its fixed rate debt. As market interest rates move, the fair value

of the Company’s debt is affected. To protect against this risk on certain debt issuances that the Company has

elected to carry at fair value, the Company has entered into pay variable-receive fixed interest rate swaps that

decrease in value in a rising rate environment and increase in value in a declining rate environment.

The Company is exposed to risk on the returns of certain of its brokered deposits that are carried at fair value.

To hedge against this risk, the Company has entered into interest rate derivatives that mirror the risk profile

of the returns on these instruments.

The Company is exposed to interest rate risk associated with MSRs, which the Company hedges with a

combination of mortgage and interest rate derivatives, including forward and option contracts, futures, and

forward rate agreements.

The Company enters into mortgage and interest rate derivatives, including forward contracts, futures, and

option contracts to mitigate interest rate risk associated with IRLCs, mortgage LHFS, and mortgage LHFI

reported at fair value.

• The Company is exposed to foreign exchange rate risk associated with certain senior notes denominated in euros and

pound sterling. This risk is economically hedged with cross currency swaps, which receive either euros or pound sterling

and pay U.S. dollars. Interest expense on the Consolidated Statements of Income/(Loss) reflects only the contractual

interest rate on the debt based on the average spot exchange rate during the applicable period, while fair value changes

on the derivatives and valuation adjustments on the debt are both recognized within trading income/(loss).

• The Company enters into CDS to hedge credit risk associated with certain loans held within its CIB line of business.

• Trading activity, as illustrated in the tables within this footnote, primarily includes interest rate swaps, equity derivatives,

CDS, futures, options and foreign currency contracts. These derivatives are entered into in a dealer capacity to facilitate

client transactions or are utilized as a risk management tool by the Company as an end user in certain macro-hedging

strategies. The macro-hedging strategies are focused on managing the Company’s overall interest rate risk exposure

that is not otherwise hedged by derivatives or in connection with specific hedges and, therefore, the Company does

not specifically associate individual derivatives with specific assets or liabilities.