SunTrust 2011 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2011 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

|

|

58

from selling, pledging, assigning, or otherwise using the pledged Coke common shares in its business.

We generally may not prepay the Notes. The interest rate on the Notes will be reset upon or after the settlement of The

Agreements, either through a remarketing process, or based upon dealer quotations. In the event of an unsuccessful remarketing

of the Notes, we would be required to collateralize the Notes and the maturity of the Notes may accelerate to the first anniversary

of the settlement of The Agreements. However, we presently believe that it is substantially certain that the Notes will be

successfully remarketed.

The Agreements carry scheduled settlement terms of approximately seven years from the effective date. However, we have

the option to terminate The Agreements earlier with the approval of the Federal Reserve. The Agreements may also terminate

earlier upon certain events of default, extraordinary events regarding Coke, and other typical termination events. Upon such

early termination, there could be exit costs or gains, such as certain breakage fees including an interest rate make-whole

amount, associated with both The Agreements and the Notes. Such costs or gains may be material but cannot be determined

at the present time due to the unlikely occurrence of such events and the number of variables that are unknown. However, the

payment of such costs, if any, will not result in us receiving less than the Minimum Proceeds from The Agreements. We expect

to sell all of the Coke common shares upon settlement of The Agreements, either under the terms of The Agreements or in

another market transaction. See Note 17, “Derivative Financial Instruments,” to the Consolidated Financial Statements in this

Form 10-K for additional discussion of the transactions.

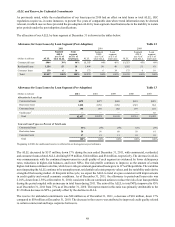

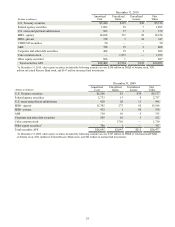

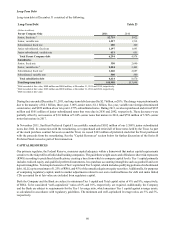

DEPOSITS

Composition of Average Deposits

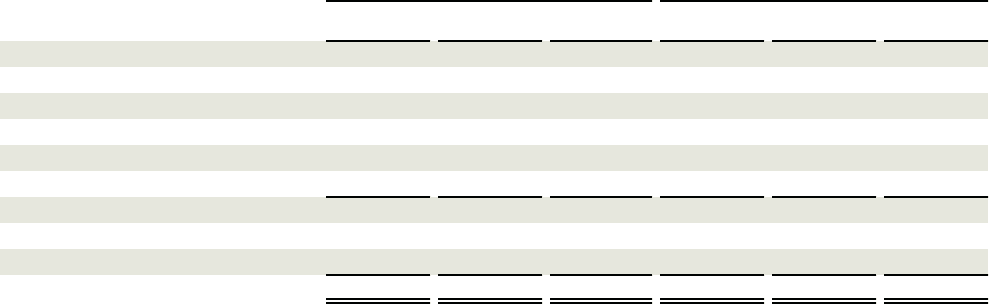

(Dollars in millions)

Noninterest-bearing

NOW accounts

Money market accounts

Savings

Consumer time

Other time

Total consumer and commercial deposits

Brokered time deposits

Foreign deposits

Total deposits

December 31

2011

$31,045

24,751

42,854

4,535

12,451

7,036

122,672

2,306

80

$125,058

2010

$26,103

24,668

38,893

4,028

14,232

9,205

117,129

2,561

355

$120,045

2009

$24,249

23,601

31,864

3,664

16,718

13,068

113,164

5,648

434

$119,246

Percent of Total

2011

25%

20

34

4

10

5

98

2

—

100%

2010

22%

21

32

3

12

8

98

2

—

100%

Table 20

2009

20%

20

27

3

14

11

95

5

—

100%

During 2011, we continued to experience deposit growth as well as improving deposit mix as the relative proportion of lower

cost deposit accounts increased. These favorable trends were major drivers of the growth in net interest margin that we were

able to achieve during the year. Average consumer and commercial deposits increased during 2011 by $5.5 billion, up 5%,

compared with 2010. The growth was concentrated in noninterest bearing DDA, Money Market, and Savings accounts which

increased $9.4 billion, up 14%. The increase was partially offset by declines in consumer time and other time deposit account

balances which decreased by $4.0 billion, or 17%. These positive trends resulted from our continued marketing efforts, pricing

discipline in the context of a low and declining rate environment, improving operational execution, as well as an industry-

wide preference for greater liquidity.

Consumer and commercial deposit growth remains one of our key initiatives. During 2011, we continued focus on growing

our client base, number of households, and deposit share while managing the rates we pay on our deposits. Overall growth

was accomplished through a judicious use of competitive rates in select products and select geographies. We experienced

mixed results across our 16 regions due to competitive forces and concentrations of time deposit clients; however, despite

increased competition, we are up in eight of our ten largest MSAs. Other initiatives to attract deposits included enhanced

product and features offerings, enhanced programs and initiatives, customer-targeted offers, and advanced analytics that

leverage product offerings with customer segmentation. Through our Deposit Transformation initiative, we delivered client-

focused banking solutions while responding to new regulations, such as the Dodd-Frank Act. In addition, we provided client-

facing teammates with new tools that enhance their focus on providing clients with personalized options and an exceptional

client experience. We continued to leverage the “Live Solid. Bank Solid.” brand to improve our visibility in the marketplace.

It is designed to speak to what is important to clients in the current environment and to inspire customer loyalty and capitalize

on some of the opportunities presented by the new banking landscape. We continue to manage judiciously through the

implications of impending or executed regulatory change and evaluate the impacts to our deposit products and clients. Average