SunTrust 2011 Annual Report Download - page 105

Download and view the complete annual report

Please find page 105 of the 2011 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

|

|

89

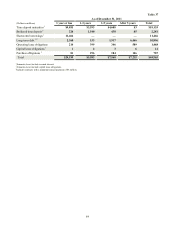

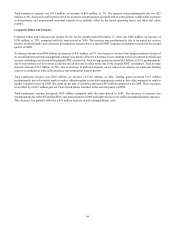

Total noninterest income was $100 million, an increase of $12 million, or 14%, from the same period in 2010. The increase was

the result of a gain from the sale of a SunTrust Community Capital property, gains from the sale of state tax credits, and higher

income related to Affordable Housing.

Total noninterest expense was $448 million, a decrease of $21 million, or 4%, over the same period in 2010. The decrease was

driven by lower credit-related expenses, staff expense, and Affordable Housing-related expense. Partially offsetting these decreases

were higher allocated administrative expenses.

Corporate and Investment Banking

CIB's net income for the twelve months ended December 31, 2011 was $355 million, an increase of $35 million, or 11%, compared

to the same period in 2010. The increase was driven by higher net interest income and a decline in provision for credit losses,

which were partially offset by an increase in noninterest expense.

Net interest income was $501 million, an increase of $119 million, or 31%, from the prior year. The increase was primarily driven

by a $2.8 billion, or 26%, increase in average loan balances. The increase in loan balances was largely the result of a $0.7 billion

increase in Three Pillars, our CP conduit, a $0.3 billion increase in asset-based lending loans, additional increases in term loans,

and an increase of line of credit utilization. The increase in average loan balances, as well as higher loan spreads, resulted in a $90

million, or 37%, increase in loan-related income. Total average customer deposits increased $1.8 billion, or 27%, with growth

concentrated in DDAs, NOW accounts, and money market accounts. Higher deposit volumes resulted in increased net interest

income of $28 million.

Provision for loan losses for 2011 was a net recovery of $10 million, compared to net charge-offs of $50 million from the prior

year. Lower net charge-offs related to large corporate borrowers operating in economically sensitive industries drove the decline.

Total noninterest income was $636 million, a decrease of $36 million, or 5%, compared to the prior year. The decrease is

predominantly due to performance in Three Pillars, equity and fixed income derivatives, and taxable fixed income sales and trading;

but is partially offset by improved performance in loan syndications and structured lending, lower derivative counterparty reserves,

and a decline in valuation related losses associated with the deterioration of collateral on previously securitized loans.

Total noninterest expense was $587 million, an increase of $89 million, or 18%. The increase was predominantly due to higher

operating losses tied to increased legal-related expenses. Additionally, higher staff expense associated with additional investments

in personnel, as well as compensation accruals tied to our Merchant Banking business along with increased operating costs tied

to growth in loans and deposits, contributed to higher overall expense.

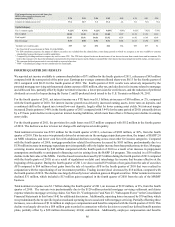

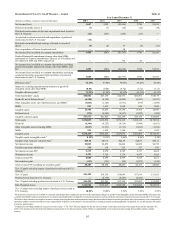

Mortgage

Mortgage reported a net loss of $693 million for the year ended December 31, 2011, an improvement of $94 million, or 12%,

compared to the same period in 2010. The improvement was driven by lower provision for credit losses that was partially offset

by lower production income, lower MSR net hedge performance, and higher expenses.

Net interest income was $492 million, up $34 million, or 7%, over the prior year. The increase was predominantly due to higher

net interest income on loans, which increased $55 million, due to improved spreads. Total average loans, primarily residential

mortgages were relatively consistent with prior year, increasing $85 million. The improvement in net interest income on loans

was partially offset by lower income on LHFS, which declined $31 million due to lower volumes and spreads.

Provision for credit losses was $693 million, a decrease of $490 million, or 41%, from the same period in 2010. The decline was

driven by a $403 million decline in residential mortgage net charge-offs. Net charge-offs included $10 million and $51 million of

charge-offs related to NPL sales in 2011 and 2010, respectively.

Noninterest income was $241 million in 2011, down $280 million, or 54%, from 2010. Total mortgage production income for the

year was a loss of $19 million, down $133 million from the prior year as loan production volume of $23.1 billion was down $6.2

billion, or 21%, from the prior year resulting in lower gain on sale and fee income. Mortgage loan repurchase provision was up

$46 million over the prior year due to higher agency-related repurchase requests.

Mortgage servicing income was down $134 million, or 37%, compared to 2010 due to less favorable net hedge performance,

which was negatively impacted by $38 million due to an increase in prepayment assumptions attributable to anticipated refinancing

activity arising from the HARP 2.0 program. Total loans serviced at December 31, 2011 were $157.8 billion compared with $167.2

billion the prior year, down 6%.