SunTrust 2011 Annual Report Download - page 175

Download and view the complete annual report

Please find page 175 of the 2011 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

|

|

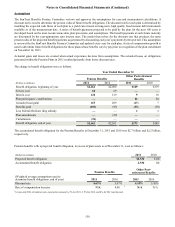

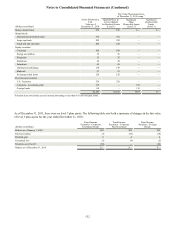

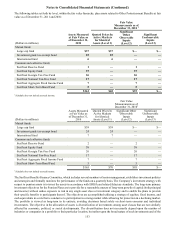

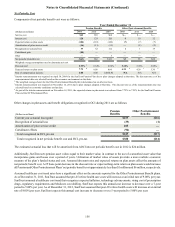

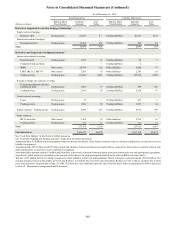

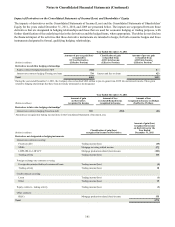

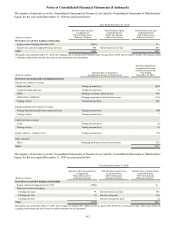

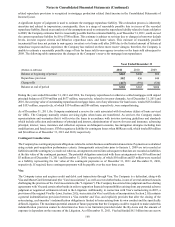

Notes to Consolidated Financial Statements (Continued)

159

(Dollars in millions)

Derivatives designated in cash flow hedging relationships 2

Equity contracts hedging:

Securities AFS

Interest rate contracts hedging:

Floating rate loans

Total

Derivatives designated in fair value hedging relationships 3

Interest rate contracts covering:

Securities AFS

Fixed rate debt

Total

Derivatives not designated as hedging instruments 4

Interest rate contracts covering:

Fixed rate debt

MSRs

LHFS, IRLCs, LHFI-FV

Trading activity

Foreign exchange rate contracts covering:

Foreign-denominated debt and

commercial loans

Trading activity

Credit contracts covering:

Loans

Trading activity

Equity contracts - Trading activity

Other contracts:

IRLCs and other

Trading activity

Total

Total derivatives

As of December 31, 20111

Asset Derivatives

Balance Sheet

Classification

Trading assets

Trading assets

Trading assets

Trading assets

Trading assets

Other assets

Other assets

Trading assets

Trading assets

Trading assets

Trading assets

Trading assets

Trading assets

Other assets

Trading assets

Notional

Amounts

$1,547

14,850

16,397

—

1,000

1,000

437

28,800

2,657

113,420

33

2,532

45

1,841

10,168

4,909

207

165,049

$182,446

6

7

6

Fair

Value

$—

1,057

1,057

—

56

56

13

472

19

6,226

1

127

1

28

1,013

84

23

8,007

$9,120

Liability Derivatives

Balance Sheet

Classification

Trading liabilities

Trading liabilities

Trading liabilities

Trading liabilities

Trading liabilities

Other liabilities

Other liabilities

Trading liabilities

Trading liabilities

Trading liabilities

Trading liabilities

Trading liabilities

Trading liabilities

Other liabilities

Trading liabilities

Notional

Amounts

$1,547

—

1,547

450

—

450

60

2,920

6,228

101,042

460

2,739

308

1,809

10,445

139

203

126,353

$128,350

5

7

8

Fair

Value

$189

—

189

1

—

1

9

29

54

5,847

129

125

3

23

1,045

22

23

7,309

$7,499

8

1 During 2011, the Company began offsetting cash collateral paid to and received from derivative counterparties when the derivative contracts are subject to ISDA

master netting arrangements and meet the derivatives accounting requirements. The effects of offsetting on the Company's Consolidated Balance Sheets as of

December 31, 2011 are presented in Note 19, "Fair Value Election and Measurement."

2 See “Cash Flow Hedges” in this Note for further discussion.

3 See “Fair Value Hedges” in this Note for further discussion.

4 See “Economic Hedging and Trading Activities” in this Note for further discussion.

5 Amount includes $1.2 billion of notional amounts related to interest rate futures. These futures contracts settle in cash daily and therefore, no derivative asset or

liability is recognized.

6 Amounts include $16.7 billion and $0.6 billion of notional related to interest rate futures and equity futures, respectively. These futures contracts settle in cash

daily and therefore, no derivative asset or liability is recognized.

7 Asset and liability amounts include $2 million and $6 million, respectively, of notional from purchased and written credit risk participation agreements, respectively,

which notional is calculated as the notional of the derivative participated adjusted by the relevant RWA conversion factor.

8 Includes a $22 million derivative liability recognized in other liabilities in the Consolidated Balance Sheets, related to a notional amount of $134 million. The

notional amount is based on the number of Visa Class B shares, 3.2 million, the conversion ratio from Class B shares to Class A shares, and the Class A share

price at the derivative inception date of May 28, 2009. This derivative was established upon the sale of Class B shares in the second quarter of 2009 as discussed

in Note 18, “Reinsurance Arrangements and Guarantees.”