SunTrust 2011 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2011 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

|

|

51

is filed as Exhibit 10.25 to this Form 10-K. The Consent Order requires us to improve certain processes and to retain an

independent consultant to conduct a review of residential foreclosure actions pending during 2009 and 2010 to identify any

errors, misrepresentations or deficiencies, determine whether any instances so identified resulted in financial injury, and then

make any appropriate remediation, reimbursement, or adjustment. Additionally, borrowers who had a residential foreclosure

action pending during this two-year review period have been solicited through advertising and direct mailings to request a

review by the independent consultant of their case if they believe they incurred a financial injury as a result of errors,

misrepresentations or other deficiencies in the foreclosure process. A direct mail solicitation was completed on November

28, 2011. The deadline for submitting requests for review is July 31, 2012. These requirements prescribed by the Consent

Order may result in additional delays in the foreclosure process at a time when the time required for foreclosure upon residential

real estate collateral in certain states, primarily Florida, continues to be elevated. These delays in the foreclosure process have

adversely affected us by increasing our expenses related to carrying such assets, such as taxes, insurance, and other carrying

costs, and by exposing us to losses as a result of potential additional declines in the value of such collateral. These delays

have also resulted, in some cases, in an inability to meet certain investor foreclosure timelines for loans we service for others,

which has resulted, and is expected to continue to result, in the assessment of compensatory fees. Noninterest expense in our

Mortgage line of business increased in 2011 as a result of the additional resources necessary to perform the foreclosure process

assessment, revise affidavit filings and make any other operational changes. Additionally, continued and evolving changes

in the regulatory environment and industry standards have increased our default servicing costs. Finally, the time to complete

foreclosure sales has increased, and this has resulted in an increase in nonperforming assets and servicing advances, and has

adversely impacted the collectability of such advances. Accordingly, additional delays in foreclosure sales, including any

delays beyond those currently anticipated, our process enhancements, and any issues that may arise out of alleged irregularities

in our foreclosure processes, could further increase the costs associated with our mortgage operations. See additional discussion

in Part I, Item 1A, "Risk Factors" in this Form 10-K.

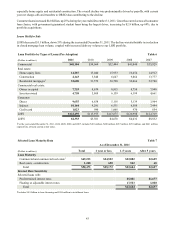

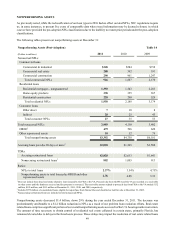

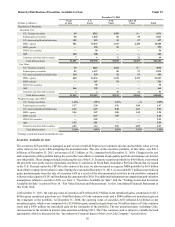

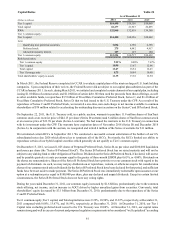

Nonperforming Assets (Pre-Adoption)

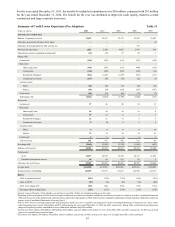

(Dollars in millions)

Nonaccrual/NPLs:

Commercial

Real estate:

Construction loans

Residential mortgages

Home equity lines

Commercial real estate

Consumer loans

Total nonaccrual/NPLs

OREO1

Other repossessed assets

Total nonperforming assets

Accruing loans past due 90 days or more2

TDRs:

Accruing restructured loans

Nonaccruing restructured loans3

Ratios:

NPLs to total loans

Nonperforming assets to total loans plus OREO

and other repossessed assets

2011

$127

390

1,655

273

431

27

2,903

479

10

$3,392

$2,028

$2,820

802

2.37%

2.76

2010

$255

1,013

1,988

285

531

38

4,110

596

52

$4,758

$1,565

2,613

1,005

3.54%

4.08

2009

$484

1,484

2,716

289

392

37

5,402

620

79

$6,101

$1,500

1,641

913

4.75%

5.33

2008

$322

1,277

1,847

272

177

45

3,940

500

16

$4,456

$1,032

463

268

3.10%

3.49

Table 15

2007

$75

295

841

136

44

39

1,430

184

12

$1,626

$611

30

—

1.17%

1.33

1Does not include foreclosed real estate related to serviced loans insured by the FHA or the VA. Insurance proceeds due from the FHA and the VA are recorded

as a receivable in other assets until the funds are received and the property is conveyed.

2Includes $979 million, $494 million, and $236 million of consolidated loans eligible for repurchase from Ginnie Mae and classified as held for sale at

December 31, 2009, 2008, and 2007, respectively.

3Nonaccruing restructured loans are included in total nonaccrual/NPLs.

Restructured Loans

To maximize the collection of loan balances, we evaluate troubled loans on a case-by-case basis to determine if a loan

modification would be appropriate. We pursue loan modifications when there is a reasonable chance that an appropriate

modification would allow our client to continue servicing the debt. For loans secured by residential real estate, if the client

demonstrates a loss of income such that the client cannot reasonably support even a modified loan, we may pursue short sales