SunTrust 2011 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2011 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

|

|

70

As certain markets recover, we are able to reduce our exposure to many of our level 3 instruments through sales, maturities, or

other distributions at prices approximating our previous estimates; thereby corroborating the valuation approaches used. Many of

our remaining level 3 securities, however, will be held until final distribution or maturity. While it is difficult to accurately predict

the ultimate cash value of these securities, we believe the amount that would be ultimately realized if the securities were held to

settlement or maturity will generally be similar to or greater than the current fair value of the securities classified as level 3. This

assessment is based on the current performance of the underlying collateral, which is experiencing elevated losses but generally

not to the degree that correlates to current market values, which reflect downward pressure due to liquidity issues and other broader

macro-economic conditions. It is reasonably likely that market volatility for certain instruments will continue as a result of a

variety of external factors. This lack of liquidity has caused us to evaluate the performance of the underlying collateral and to use

a discount rate commensurate with the rate a market participant would use to value the instrument in an orderly transaction, but

that also acknowledges illiquidity premiums and required investor rates of return that would be demanded under current market

conditions. The discount rate considered the capital structure of the instrument, market indices, and the relative yields of instruments

for which third party pricing information and/or market activity was available. In certain instances, the interest rate and credit risk

components of the valuation indicated a full return of expected principal and interest; however, the lack of liquidity resulted in

wide ranges of discounts in valuing certain level 3 instruments. The illiquidity that continues to persist in certain markets requires

discounts of this degree to drive a market competitive yield, as well as to account for the anticipated extended tenor. The discount

rates selected derived reasonable prices when compared to (i) observable transactions, when available, (ii) other securities on a

relative basis, (iii) the bid/ask spread of non-binding broker indicative bids and/or (iv) our professional judgment.

All of the techniques used and information obtained in the valuation process provides a range of estimated values, which were

evaluated and compared in order to establish an estimated value that, based on management's judgment, represented a reasonable

estimate of the instrument's fair value. It was not uncommon for the range of value of these instruments to vary widely; in such

cases, we selected an estimated value that we believed was the best indication of value based on the yield a market participant in

this current environment would expect. Due to the continued illiquidity and credit risk of level 3 securities, these market values

are highly sensitive to assumption changes and market volatility. Improvements may be made to our pricing methodologies on an

ongoing basis as observable and relevant information becomes available to us. See Note 19, “Fair Value Election and Measurement,”

to the Consolidated Financial Statements in this Form 10-K for a detailed discussion regarding level 2 and 3 securities and valuation

methodologies for each class of securities.

Most derivative instruments are level 1 or level 2 instruments, except for the IRLCs, the Visa litigation related derivative, discussed

below, and The Agreements we entered into related to our investment in Coke common stock, which are level 3 instruments.

Because the value of The Agreements is primarily driven by the embedded equity collars on the Coke common shares, a Black-

Scholes model is the appropriate valuation model. Most of the assumptions are directly observable from the market, such as the

per share market price of Coke common stock, interest rates, and the dividend rate on Coke common stock. Volatility is a significant

assumption and is impacted both by the unusually large size of the trade and the long tenor until settlement. The Agreements carry

scheduled terms of approximately six and a half and seven years from the effective date, and as such, the observable and active

options market on Coke does not provide for any identical or similar instruments. As a result, we receive estimated market values

from a market participant who is knowledgeable about Coke equity derivatives and is active in the market. Based on inquiries of

the market participant as to their procedures as well as our own valuation assessment procedures, we have satisfied ourselves that

the market participant is using methodologies and assumptions that other market participants would use in arriving at the fair value

of The Agreements. At December 31, 2011, the Coke derivative liability was valued at $189 million and was included within the

level 3 trading liabilities portfolio.

At December 31, 2011, level 3 trading assets and level 3 securities AFS totaled $49 million and $1.0 billion, respectively. Our

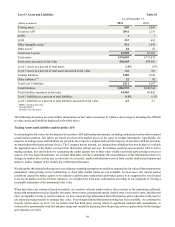

level 3 securities AFS portfolio included FHLB and Federal Reserve Bank stock, as well as certain municipal bond securities,

some of which are only redeemable with the issuer at par and cannot be traded in the market; as such, no significant observable

market data for these instruments is available. These nonmarketable securities AFS totaled approximately $770 million at

December 31, 2011. The remaining level 3 securities, both trading assets and securities AFS, are predominantly private ABS and

MBS and CDOs, including interests retained from Company-sponsored securitizations or purchased from third party securitizations.

We also have exposure to bank trust preferred CDOs, student loan ABS, and municipal securities due to our purchase of certain

ARS as a result of failed auctions. For all level 3 securities, little or no market activity exists for either the security or the underlying

collateral and therefore the significant assumptions used to value the securities are not market observable.

Level 3 trading assets declined by $160 million, or 77%, during the year ended December 31, 2011, primarily due to sales,

paydowns, redemptions, and maturities of securities, partially offset by net unrealized mark to market gains and a small amount

of purchases. Level 3 securities AFS declined by $95 million, or 8%, during the year ended December 31, 2011, due to continued

paydowns and redemptions by issuers of securities, partially offset by net unrealized mark to market gains and a small amount of

FHLB of Atlanta stock purchases. During the year ended December 31, 2011, we recognized through earnings $44 million in net

gains related to trading assets and liabilities and securities AFS classified as level 3.