SunTrust 2011 Annual Report Download - page 54

Download and view the complete annual report

Please find page 54 of the 2011 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

|

|

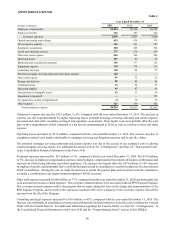

38

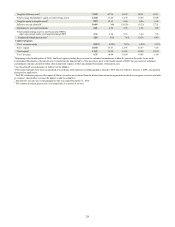

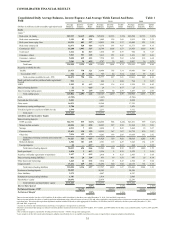

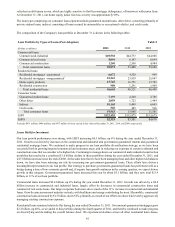

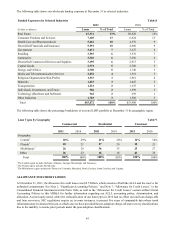

NONINTEREST INCOME

(Dollars in millions)

Service charges on deposit accounts

Trust and investment management income

Other charges and fees

Card fees

Investment banking income

Trading income/(loss)

Retail investment services

Mortgage production related (loss)/income

Mortgage servicing related income

Net securities gains

Gain from ownership in Visa

Other noninterest income

Total noninterest income

Year Ended December 31

2011

$685

531

507

371

317

248

230

(5)

224

117

—

196

$3,421

2010

$760

503

534

376

313

173

205

127

358

191

—

189

$3,729

Table 3

2009

$848

486

523

324

272

(41)

218

376

330

98

112

164

$3,710

Noninterest income decreased by $308 million, or 8%, compared with the year ended December 31, 2010, due to lower

mortgage-related income, lower deposit service charges due primarily to Regulation E, and lower net gains on the sale of

investment securities, partially offset by higher trading income/(loss), trust and investment management income, and retail

investment services income.

Mortgage servicing related income decreased by $134 million, or 37%, compared with the year ended December 31, 2010.

The decline was due to less favorable net hedge performance and lower MSR valuations resulting from an increase in

prepayment assumptions attributable to increased refinancing activity. Furthermore, during the fourth quarter of 2011,

mortgage servicing related income was impacted by a decline in fair value of MSRs of $38 million due to the HARP 2.0

program, which is anticipated to result in higher refinance activity. See the “Other Market Risk” section of this MD&A for

further information regarding the risks pertaining to the valuation of our MSRs. The remaining decrease is due to a decline

in service fees attributable to a decrease in the servicing portfolio. As of December 31, 2011, the balance of mortgages serviced

was $157.8 billion compared with $167.2 billion as of December 31, 2010.

Mortgage production related (loss)/income was a loss of $5 million for the year ended December 31, 2011 compared with

income of $127 million for the year ended December 31, 2010. The decline was predominantly due to declines in loan

production volume. Loan production volume of $23.1 billion in 2011 was down $6.2 billion, or 21%, from the prior year,

coupled with lower margins, which resulted in lower gain on sale and fee income. Additionally, the mortgage repurchase

provision for the year ended December 31, 2011 was $502 million compared with $456 million for the year ended December 31,

2010, an increase of $46 million due to the increase in agency-related repurchase requests (see below for additional discussion).

The reserves for mortgage repurchases was $320 million as of December 31, 2011, an increase of $55 million from prior year.

Repurchase requests can vary significantly from period to period based on the timing of requests from the GSEs. Mortgage

repurchase demands were elevated during 2011 compared to 2010. The majority of our demands are from loans in the 2006-2008

vintages that have been 120 days past due at some point in their life cycle. In addition, the majority of the demands that we

have received have been from loans that were delinquent within the first 36 months after origination. If this pattern continues

and investor selection criteria does not change, it suggests that the pool of delinquent loans from which we will receive

demands could be stabilizing, given that any performing loans from the 2006-2008 vintages have now been outstanding

beyond 36 months. This pattern is expected to result in a decline in the mortgage repurchase provision in the second half of

2012.

However, we believe that demands will continue to be volatile and may remain elevated in 2012. A continued sluggish economy

and any further declines in housing values could impact the future amount of demands. If demands do not decline from levels

seen in the latter half of 2011, we may see an increase in the repurchase provision in 2012, which would result in lower

mortgage production income. As a result of the continued uncertainty and our expectation of elevated demands in the near

term, our mortgage repurchase reserve remains at historically high levels. For additional information on the mortgage

repurchase reserve, see Note 18, "Reinsurance Arrangements and Guarantees," to the Consolidated Financial Statements in

this Form 10-K, the "Critical Accounting Policies" section of this MD&A, and "Part I, Item 1A, Risk Factors" in this Form

10-K.