SunTrust 2011 Annual Report Download - page 174

Download and view the complete annual report

Please find page 174 of the 2011 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

|

|

Notes to Consolidated Financial Statements (Continued)

158

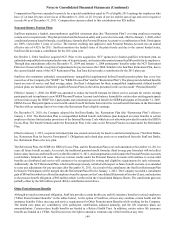

The majority of the Company’s derivatives contain contingencies that relate to the creditworthiness of the Bank. These

contingencies, which are contained in industry standard master trading agreements, may be considered events of default. Should

the Bank be in default under any of these provisions, the Bank’s counterparties would be permitted under such master agreements

to close-out net at amounts that would approximate the then-fair values of the derivatives and the offsetting of the amounts would

produce a single sum due by one party to the other. The counterparties would have the right to apply any collateral posted by the

Bank against any net amount owed by the Bank. Additionally, certain of the Company’s derivative liability positions, totaling $1.2

billion and $1.1 billion in fair value at December 31, 2011 and 2010, respectively, contain provisions conditioned on downgrades

of the Bank’s credit rating. These provisions, if triggered, would either give rise to an ATE that permits the counterparties to close-

out net and apply collateral or, where a CSA is present, require the Bank to post additional collateral. Collateral posting requirements

generally result from differences in the fair value of the net derivative liability compared to specified collateral thresholds at

different ratings levels of the Bank, both of which are negotiated provisions within each CSA. At December 31, 2011, the Bank

carried senior long-term debt ratings of A3/BBB+ from three of the major ratings agencies. At the current rating level, ATEs have

been triggered for approximately $9 million in fair value liabilities as of December 31, 2011. For illustrative purposes, if the Bank

were downgraded to Baa3/BBB-, ATEs would be triggered in derivative liability contracts that had a total fair value of $5 million

at December 31, 2011, against which the Bank had posted collateral of $3 million; ATEs do not exist at lower ratings levels. At

December 31, 2011, $1.2 billion in fair value of derivative liabilities were subject to CSAs, against which the Bank has posted

$1.2 billion in collateral, primarily in the form of cash. If requested by the counterparty pursuant to the terms of the CSA, the Bank

would be required to post estimated additional collateral against these contracts at December 31, 2011 of $16 million if the Bank

were downgraded to Baa3/BBB-, and any further downgrades to Ba1/BB+ or below would require the posting of an additional

$10 million. Such collateral posting amounts may be more or less than the Bank’s estimates based on the specified terms of each

CSA as to the timing of a collateral calculation and whether the Bank and its counterparties differ on their estimates of the fair

values of the derivatives or collateral.

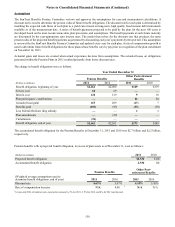

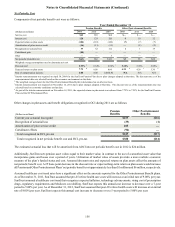

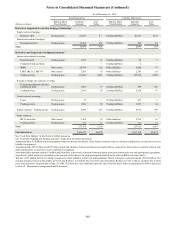

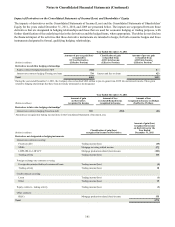

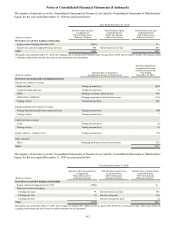

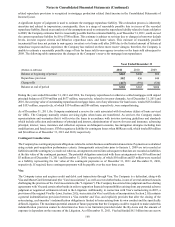

Notional and Fair Value of Derivative Positions

The following tables present the Company’s derivative positions at December 31, 2011 and 2010. The notional amounts in the

tables are presented on a gross basis and have been classified within Asset Derivatives or Liability Derivatives based on the

estimated fair value of the individual contract at December 31, 2011 and 2010. Gross positive and gross negative fair value amounts

associated with respective notional amounts are presented without consideration of any netting agreements. For contracts

constituting a combination of options that contain a written option and a purchased option (such as a collar), the notional amount

of each option is presented separately, with the purchased notional amount generally being presented as an Asset Derivative and

the written notional amount being presented as a Liability Derivative. The fair value of a combination of options is generally

presented as a single value with the purchased notional amount if the combined fair value is positive, and with the written notional

amount, if the combined fair value is negative.