SunTrust 2011 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2011 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

|

|

50

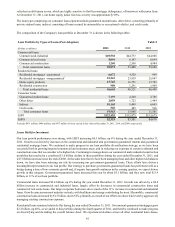

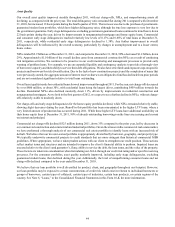

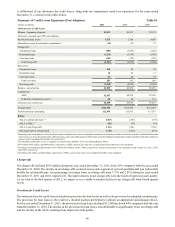

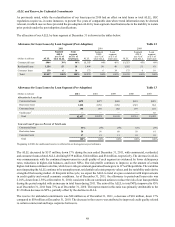

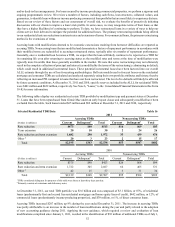

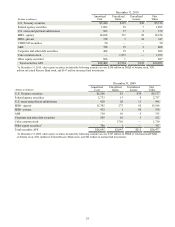

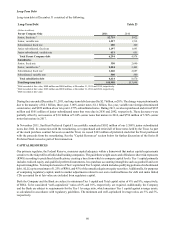

within the nonperforming assets portfolio. Overall, NPL declines in recent quarters have been driven by commercial loans,

as the higher-risk commercial construction portfolio has been reduced, while the commercial and industrial loans have generally

performed well. As we look to the first quarter of 2012, we expect the recent quarterly trends to continue, with a continued

decline in NPLs.

Nonperforming Loans

Nonperforming commercial loans decreased $961 million, down 51% during the year ended December 31, 2011, driven by

a $671 million decrease in commercial construction NPLs and a $236 million decrease in commercial and industrial NPLs.

We expect NPLs to continue to decline in the first quarter of 2012; however, we continue to expect some variability in inflows

of commercial real estate NPLs as we move through the current commercial real estate cycle.

Nonperforming residential loans declined $238 million, down 11% during the year ended December 31, 2011, largely due to

a $151 million decrease in nonguaranteed residential mortgage NPLs, along with a $70 million decline in residential

construction NPLs. The $151 million decrease was partially attributable to the reclassification of certain nonperforming

residential mortgages as held for sale to reflect our intention to sell these mortgages. We recorded an incremental charge-off

of $10 million in the first quarter in connection with the decision to transfer and sell these mortgages. Approximately $34

million of these reclassified NPLs were sold during the second quarter; the remaining $13 million were transferred back to

LHFI as they were no longer deemed marketable for sale. The remaining decrease was attributable to lower net charge-offs

and inflows of NPLs. We expect some variability in inflows of nonperforming residential loans during 2012 related to mortgage

loan repurchases from investors. See additional discussion of mortgage loan repurchases in Note 18, "Reinsurance

Arrangements and Guarantees," to the Consolidated Financial Statements in this Form 10-K.

Nonperforming consumer loans decreased $8 million, down 23% during the year ended December 31, 2011, largely as a result

of a $5 million decrease in indirect consumer NPLs. The decrease was driven by net charge-offs of existing nonperforming

consumer loans during the year, largely offset by the migration of delinquent consumer loans to nonaccrual status.

Interest income on consumer and residential nonaccrual loans, if recognized, is recognized on a cash basis. Interest income

on commercial nonaccrual loans is not recognized until after the principal has been reduced to zero. We recognized $34 million

and $39 million of interest income related to nonaccrual loans for the years ended December 31, 2011 and 2010, respectively.

If all such loans had been accruing interest according to their original contractual terms, estimated interest income of $246

million and $340 million for the years ended December 31, 2011 and 2010, respectively, would have been recognized.

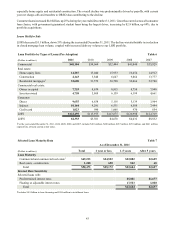

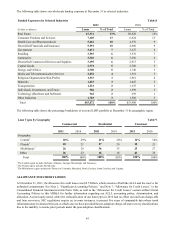

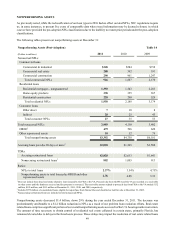

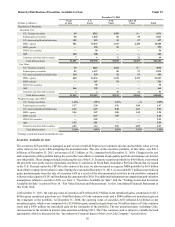

Other Nonperforming Assets

OREO decreased $117 million, down 20% during the year ended December 31, 2011. The decline consisted of net decreases

of $124 million in residential homes and $24 million in residential construction related properties, partially offset by a $31

million increase in commercial properties. During the years ended December 31, 2011 and 2010, sales of OREO resulted in

proceeds of $619 million and $769 million, respectively, and net losses on sales of OREO of $4 million and $25 million,

respectively, inclusive of valuation reserves, primarily attributed to lots and land evaluated under the pooled approach. Sales

of OREO and the related gains or losses are highly dependent on our disposition strategy and buyer opportunities. See Note

19, “Fair Value Election and Measurement,” to the Consolidated Financial Statements in this Form 10-K for more information.

Gains and losses on sale of OREO are recorded in other real estate expense in the Consolidated Statements of Income/(Loss).

Geographically, most of our OREO properties are located in Georgia, Florida, and North Carolina. Residential properties and

land comprised 38% and 40%, respectively, of OREO; the remainder is related to commercial and other properties. Upon

foreclosure, the values of these properties were reevaluated and, if necessary, written down to their then-current estimated

value, less costs to sell. Further declines in home prices could result in additional losses on these properties. We are actively

managing and disposing of these foreclosed assets to minimize future losses.

Other repossessed assets decreased by $42 million, down 81% during the year ended December 31, 2011. The decrease was

largely attributable to the sale of repossessed assets during the year.

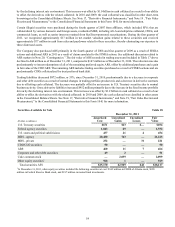

The majority of our past due accruing loans are residential mortgages and student loans that are fully guaranteed by a federal

agency. Accruing loans past due ninety days or more increased by $463 million, up 30% during the year ended December 31,

2011, essentially all of which was attributable to guaranteed residential mortgages and student loans. At December 31, 2011

and 2010, $57 million and $84 million, respectively, of past due accruing loans were not guaranteed.

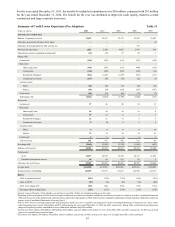

At the end of 2010, we completed an internal review of STM’s residential foreclosure processes. In 2011, we continued to

improve upon our processes as a result of our review. In addition, following the Federal Reserve's horizontal review of the

nation’s largest mortgage loan servicers, SunTrust and other servicers entered into Consent Orders with the FRB. We describe

the Consent Order in Note 20, “Contingencies,” to the Consolidated Financial Statements in this Form 10-K and a copy of it