SunTrust 2011 Annual Report Download - page 79

Download and view the complete annual report

Please find page 79 of the 2011 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

|

|

63

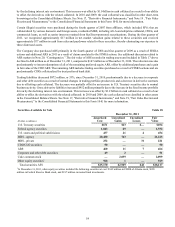

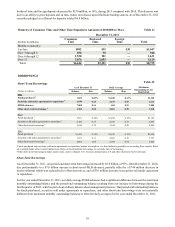

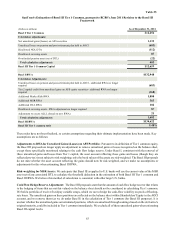

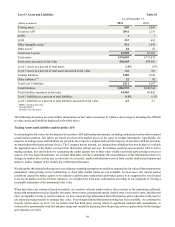

SunTrust's Estimation of Basel III Tier 1 Common, pursuant to BCBS's June 2011 Revision to the Basel III

Framework

(Dollars in millions)

Basel I Tier 1 Common

Calculation adjustments:

Net unrealized gains/(losses) on AFS securities

Unrealized losses on pension and post-retirement plan held in AOCI

Disallowed NOL DTA

Disallowed servicing assets

Overfunded pension asset (net of DTL)

Total calculation adjustments

Basel III Tier 1 Common Capital

Basel I RWA

Calculation Adjustments:

Unrealized losses on pension and post-retirement plan held in AOCI - additional RWA no longer

required

Tier 2 capital credit from unrealized gains on AFS equity securities - additional RWA no longer

required

Additional Market Risk RWA

Additional MSR RWA

Additional DTA RWA

Disallowed servicing assets - RWA adjustment no longer required

Adjustment to excess ALLL (based on new RWA)

Total calculation adjustments

Basel III RWA

Basel III Tier 1 common ratio

Table 25

As of December 31, 2011

$12,254

1,135

(683)

(112)

87

(22)

405

$12,659

$132,940

(683)

(368)

1,880

563

182

87

21

1,682

$134,622

9.40%

These rules have not been finalized, so certain assumptions regarding their ultimate implementation have been made. Key

assumptions are as follows:

Adjustments to RWA for Unrealized Gains/(Losses) on AFS Portfolio: Pursuant to its definition of Tier 1 common equity,

the Basel III proposals no longer apply an adjustment to remove unrealized gains or losses recognized on the balance sheet,

except those specifically mentioned relating to the cash flow hedge reserve. Under Basel I, consistent with the removal of

these unrealized gains and losses from Tier 1 capital, the asset account reflecting these gains and losses (though they are

reflected pre-tax) is not subject to risk weighting; only the book values of the assets are risk-weighted. The Basel III proposals

do not state whether the asset account reflecting the gains should now be risk-weighted, and we make no assumptions or

adjustments for this when estimating Basel III RWA.

Risk-weighting for MSR Assets: We anticipate that Basel III as applied to U.S. banks will use the current value of the MSR

asset net of any associated DTL to calculate the threshold deduction in the estimation of both Basel III Tier 1 common and

Basel III RWA. We believe this method of calculation is consistent with other large U.S. banks.

Cash Flow Hedge Reserve Adjustment: The Basel III proposals state that the amount of cash flow hedge reserve that relates

to the hedging of items that are not fair valued on the balance sheet should not be considered in calculating Tier 1 common.

We hold a portfolio of receive fixed/pay variable swaps, which we use to hedge the cash-flow volatility on pools of floating-

rate loans. The unrealized gains on these positions are reflected on the balance sheet within Shareholders' Equity in the AOCI

account, and we remove them (as we do under Basel I) in the calculation of Tier 1 common (for Basel III purposes). It is

unclear whether the unrealized gains on terminated positions, which are amortized through earnings based on the derivative's

original maturity, could be included in Tier 1 common immediately. We exclude all of these unrealized gains when estimating

Basel III capital levels.