SunTrust 2011 Annual Report Download - page 150

Download and view the complete annual report

Please find page 150 of the 2011 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

|

|

Notes to Consolidated Financial Statements (Continued)

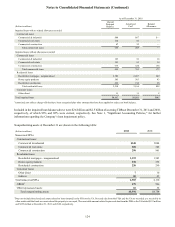

134

were $2.0 billion and $1.9 billion, respectively, at December 31, 2011, and $2.1 billion and $2.0 billion, respectively, at

December 31, 2010. The Company is not obligated to provide any support to these entities, nor has it previously provided

support to these entities. No events occurred during the year ended December 31, 2011 that would change the Company’s

previous conclusion that it is not the primary beneficiary of any of these securitization entities.

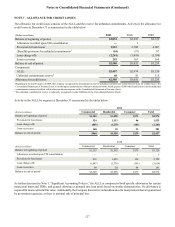

Student Loans

In 2006, the Company completed a securitization of government-guaranteed student loans through a transfer of loans to

a securitization SPE, which previously qualified as a QSPE, and retained the related residual interest in the SPE. The

Company, as master servicer of the loans in the SPE, has agreed to service each loan consistent with the guidelines

determined by the applicable government agencies in order to maintain the government guarantee. The Company and

the SPE have entered into an agreement to have the loans subserviced by an unrelated third party.

The Company concluded that this securitization of government-guaranteed student loans (the “Student Loan entity”)

should be consolidated as it has both power over the entity through its role as master servicer and the obligation to absorb

losses or the right to receive benefits through the retention of the residual interest. Accordingly, the Company consolidated

the Student Loan entity at its unpaid principal amount as of September 30, 2010, resulting in incremental total assets and

total liabilities of approximately $490 million and an immaterial impact on shareholders’ equity. The consolidation of

the Student Loan entity had no impact on the Company’s earnings or cash flows that results from its involvement with

this VIE. The primary balance sheet impacts from consolidating the Student Loan entity were increases in LHFI, the

related ALLL, and long-term debt. Additionally, the Company’s ownership of the residual interest in the SPE, previously

classified in trading assets, was eliminated upon consolidation and the assets and liabilities of the Student Loan entity

are recorded on a cost basis. At December 31, 2011 and 2010, the Company’s Consolidated Balance Sheets reflected

$438 million and $479 million, respectively, of assets held by the Student Loan entity and $433 million and $474 million,

respectively, of debt issued by the Student Loan entity.

Payments from the assets in the SPE must first be used to settle the obligations of the SPE, with any remaining payments

remitted to the Company as the owner of the residual interest. To the extent that losses occur on the SPE’s assets, the

SPE has recourse to the federal government as the guarantor up to a maximum guarantee amount of 97%. Losses in

excess of the government guarantee reduce the amount of available cash payable to the Company as the owner of the

residual interest. To the extent that losses result from a breach of the master servicer’s servicing responsibilities, the SPE

has recourse to the Company; the SPE may require the Company to repurchase the loan from the SPE at par value. If the

breach was caused by the subservicer, the Company has recourse to seek reimbursement from the subservicer up to the

guaranteed amount. The Company’s maximum exposure to loss related to the SPE is represented by the potential losses

resulting from a breach of servicing responsibilities. To date, all loss claims filed with the guarantor that have been denied

due to servicing errors have either been cured or reimbursement has been provided to the Company by the subservicer.

The Company is not obligated to provide any noncontractual support to this entity, and it has not provided any such

support.

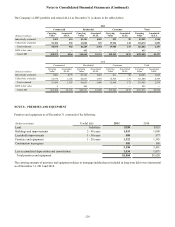

CDO Securities

The Company has transferred bank trust preferred securities in securitization transactions. The majority of these transfers

occurred between 2002 and 2005 with one transaction completed in 2007. The Company retained equity interests in

certain of these entities and also holds certain senior interests that were acquired during 2008 and 2011 in conjunction

with its acquisition of assets from the ARS transactions discussed in Note 20, “Contingencies.” The Company is not

obligated to provide any support to these entities and its maximum exposure to loss at December 31, 2011 and 2010

includes current senior interests held in trading securities, which had a fair value of $43 million as of December 31, 2011

and $29 million as of December 31, 2010.

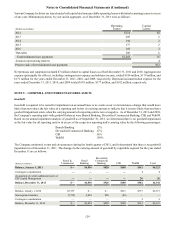

The assumptions and inputs considered by the Company in valuing this retained interest include prepayment speeds,

credit losses, and the discount rate. While all the underlying collateral is currently eligible for repayment by the obligor,

given the nature of the collateral and the current repricing environment, the Company assumed no prepayment would

occur before the final maturity, which is approximately 22 years on a weighted average basis. Due to the seniority of the

interests in the structure, current estimates of credit losses in the underlying collateral could withstand a 20% adverse

change in the default assumption without the securities incurring a valuation loss assuming all other assumptions remain

constant. Therefore, the key assumption in valuing these securities was the assumed discount rate, which was estimated

to range from 8% to 12% over LIBOR at December 31, 2011 compared to 14% to 16% over LIBOR at December 31,

2010. This significant change in the discount rate was supported by a return to liquidity in the market for similar interests.

At December 31, 2011 and 2010, a 20% adverse change in the assumed discount rate results in declines of approximately

$8 million and $5 million, respectively, in the fair value of these securities. Although the impact of each assumption

change in isolation is minimal, the underlying collateral of the VIEs is highly concentrated and as a result, the default or