SunTrust 2011 Annual Report Download - page 136

Download and view the complete annual report

Please find page 136 of the 2011 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

|

|

Notes to Consolidated Financial Statements (Continued)

120

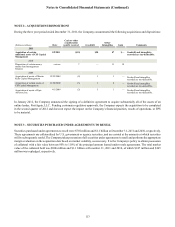

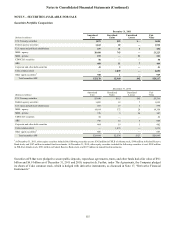

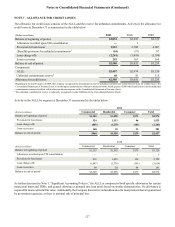

NOTE 6 - LOANS

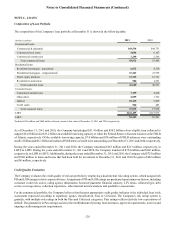

Composition of Loan Portfolio

The composition of the Company's loan portfolio at December 31 is shown in the following table:

(Dollars in millions)

Commercial loans:

Commercial & industrial

Commercial real estate

Commercial construction

Total commercial loans

Residential loans:

Residential mortgages - guaranteed

Residential mortgages - nonguaranteed1

Home equity products

Residential construction

Total residential loans

Consumer loans:

Guaranteed student loans

Other direct

Indirect

Credit cards

Total consumer loans

LHFI

LHFS

2011

$49,538

5,094

1,240

55,872

6,672

23,243

15,765

980

46,660

7,199

2,059

10,165

540

19,963

$122,495

$2,353

2010

$44,753

6,167

2,568

53,488

4,520

23,959

16,751

1,291

46,521

4,260

1,722

9,499

485

15,966

$115,975

$3,501

1Includes $431 million and $488 million of loans carried at fair value at December 31, 2011 and 2010, respectively.

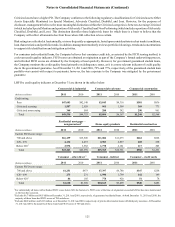

As of December 31, 2011 and 2010, the Company had pledged $51.4 billion and $50.2 billion of net eligible loan collateral to

support $34.8 billion and $31.2 billion in available borrowing capacity at either the Federal Reserve discount window or the FHLB

of Atlanta, respectively. Of the available borrowing capacity, $7.0 billion and $34 million of FHLB advances were outstanding

and $1.8 billion and $6.1 billion of undrawn FHLB letters of credit were outstanding as of December 31, 2011 and 2010, respectively.

During the years ended December 31, 2011 and 2010, the Company transferred $63 million and $213 million, respectively, in

LHFS to LHFI. During the years ended December 31, 2011 and 2010, the Company transferred $754 million and $346 million,

respectively, in LHFI to LHFS. Additionally, during the years ended December 31, 2011 and 2010, the Company sold $725 million

and $740 million in loans and leases that had been held for investment at December 31, 2011 and 2010 for gains of $22 million

and $6 million, respectively.

Credit Quality Evaluation

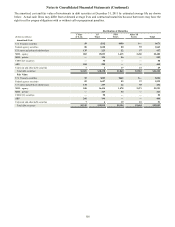

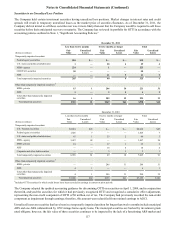

The Company evaluates the credit quality of its loan portfolio by employing a dual internal risk rating system, which assigns both

PD and LGD ratings to derive expected losses. Assignment of PD and LGD ratings are predicated upon numerous factors, including

consumer credit risk scores, rating agency information, borrower/guarantor financial capacity, LTV ratios, collateral type, debt

service coverage ratios, collection experience, other internal metrics/analysis and qualitative assessments.

For the commercial portfolio, the Company believes that the most appropriate credit quality indicator is the individual loan’s risk

assessment expressed according to regulatory agency classification, Pass or Criticized. The Company's risk rating system is

granular, with multiple risk ratings in both the Pass and Criticized categories. Pass ratings reflect relatively low expectations of

default. The granularity in Pass ratings assists in the establishment of pricing, loan structures, approval requirements, reserves and

ongoing credit management requirements.