SunTrust 2011 Annual Report Download - page 97

Download and view the complete annual report

Please find page 97 of the 2011 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

|

|

81

As mentioned above, the Bank and Parent Company maintain programs to access the debt capital markets. The Parent Company

maintains an SEC shelf registration statement from which it may issue senior or subordinated notes and various capital securities

such as common or preferred stock. Our Board has authorized the issuance of up to $5 billion of such securities, of which

approximately $2.2 billion of issuance capacity remains available. The most recent issuance from this shelf occurred on October

27, 2011, when we issued $750 million of 3.50% senior Parent Company notes due January 20, 2017. The Bank also maintains a

Global Bank Note program under which it may issue senior or subordinated debt with various terms. As of December 31, 2011,

the Bank had $33.8 billion of remaining board authority to issue notes under the program. Our issuance capacity under these

programs refers to authorization granted by our Board and does not refer to a commitment to purchase by any investor. Debt and

equity securities issued under these programs are designed to appeal primarily to domestic and international institutional investors.

Institutional investor demand for these securities is dependent upon numerous factors, including but not limited to our credit ratings

and investor perception of financial market conditions and the health of the banking sector.

Parent Company Liquidity. Our primary measure of Parent Company liquidity is the length of time the Parent Company can meet

its existing and certain forecasted obligations using its present balance of cash and liquid securities without the support of dividends

from the Bank or new debt issuance. In accordance with risk limits established by ALCO and the Board, we manage the Parent

Company’s liquidity by structuring its maturity schedule to minimize the amount of debt maturing within a short period of time.

During the year ended December 31, 2011, we had no Parent Company debt that matured, and approximately $1 billion of Parent

Company debt is scheduled to mature in 2012. Also during 2011, we repurchased $395 million of Parent Company junior

subordinated notes that were due in 2036. A majority of the Parent Company’s liabilities are long-term in nature, coming from the

proceeds of our capital securities and long-term senior and subordinated notes.

The primary uses of Parent Company liquidity include debt service, dividends on capital instruments, the periodic purchase of

investment securities, and loans to our subsidiaries. We fund corporate dividends primarily with dividends from our banking

subsidiary. We are subject to both state and federal banking regulations that limit our ability to pay common stock dividends in

certain circumstances.

Recent Developments. Numerous legislative and regulatory proposals currently outstanding may have an effect on our liquidity

if they become effective, the potential impact of which cannot be presently quantified. However, we believe that we will be well

positioned to comply with new standards as they become effective as a result of our strong core banking franchise and liquidity

management practices. See discussion of certain current legislative and regulatory proposals within the “Executive Overview”

section of this MD&A.

On December 20, 2011, the Federal Reserve published proposed measures to strengthen regulation and supervision of large bank

holding companies and systemically important nonbank financial firms, pursuant to sections 165 and 166 of the Dodd-Frank Act.

These proposed regulations include a number of requirements related to liquidity that would be instituted in phases. The first phase

encompasses largely qualitative liquidity risk management practices, including internal liquidity stress testing. The second phase

would include certain quantitative liquidity requirements related to the proposed Basel III liquidity standards. We believe that the

Company is well positioned to demonstrate compliance with these new requirements and standards if and when they are adopted.

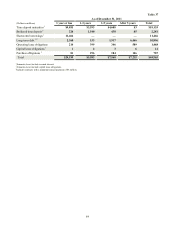

Other Liquidity Considerations. As presented in Table 36, we had an aggregate potential obligation of $62.0 billion to our clients

in unused lines of credit at December 31, 2011. Commitments to extend credit are arrangements to lend to clients who have

complied with predetermined contractual obligations. We also had $5.2 billion in letters of credit as of December 31, 2011, most

of which are standby letters of credit, which require that we provide funding if certain future events occur. Approximately $3.1

billion of these letters as of December 31, 2011 supported variable rate demand obligations.

As of December 31, 2011, our liability for UTBs was $133 million. The liability for interest related to these UTBs was $21 million

as of December 31, 2011. The UTBs represent the difference between tax positions taken or expected to be taken in our tax returns

and the benefits recognized and measured in accordance with the relevant accounting guidance for income taxes. The UTBs are

based on various tax positions in several jurisdictions, and if taxes related to these positions are ultimately paid, the payments

would be made from our normal operating cash flows, likely over multiple years.