SunTrust 2011 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2011 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

|

|

29

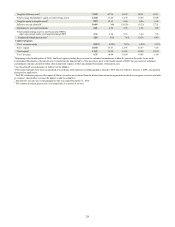

Item 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND

RESULTS OF OPERATIONS

Important Cautionary Statement About Forward-Looking Statements

This report may contain forward-looking statements. Statements regarding the impact of (i) actions taken to mitigate the

effects of the Durbin Amendment and Regulation E, the Volcker Rule, lower provision expense on net income available to

common shareholders as credit quality improves, and the impact of U.S. government programs on our student loan portfolio;

(ii) future levels of credit-related expenses, mortgage repurchase provision, net charge-offs, NPLs, net interest margin,

repurchase demands, other real estate expenses, compensatory fees related to foreclosure delays, and the size of our securities

portfolio; and (iii) expected changes in the size of or growth of our government guaranteed portfolios, NPLs, the ALLL,

changes in commercial real estate NPLs, and future income streams from new products and services, are forward-looking

statements. Also, any statement that does not describe historical or current facts is a forward-looking statement. These

statements often include the words “believes,” “expects,” “anticipates,” “estimates,” “intends,” “plans,” “targets,” “initiatives,”

“potentially,” “probably,” “projects,” “outlook” or similar expressions or future conditional verbs such as “may,” “will,”

“should,” “would,” and “could.” Such statements are based upon the current beliefs and expectations of management and on

information currently available to management. Such statements speak as of the date hereof, and we do not assume any

obligation to update the statements made herein or to update the reasons why actual results could differ from those contained

in such statements in light of new information or future events.

Forward-looking statements are subject to significant risks and uncertainties. Investors are cautioned against placing undue

reliance on such statements. Actual results may differ materially from those set forth in the forward-looking statements. Factors

that could cause actual results to differ materially from those described in the forward-looking statements can be found in

Item 1A of Part I of this report and include risks discussed in this MD&A and in other periodic reports that we file with the

SEC. Those factors include: as one of the largest lenders in the Southeast and Mid-Atlantic U.S. and a provider of financial

products and services to consumers and businesses across the U.S., our financial results have been, and may continue to be,

materially affected by general economic conditions, particularly unemployment levels and home prices in the U.S., and a

deterioration of economic conditions or of the financial markets may materially adversely affect our lending and other

businesses and our financial results and condition; legislation and regulation, including the Dodd-Frank Act, as well as future

legislation and/or regulation, could require us to change certain of our business practices, reduce our revenue, impose additional

costs on us or otherwise adversely affect our business operations and/or competitive position; we are subject to capital adequacy

and liquidity guidelines and, if we fail to meet these guidelines, our financial condition would be adversely affected; loss of

customer deposits and market illiquidity could increase our funding costs; we rely on the mortgage secondary market and

GSEs for some of our liquidity; we are subject to credit risk; our ALLL may not be adequate to cover our eventual losses; we

may have more credit risk and higher credit losses to the extent our loans are concentrated by loan type, industry segment,

borrower type, or location of the borrower or collateral; we will realize future losses if the proceeds we receive upon liquidation

of nonperforming assets are less than the carrying value of such assets; a downgrade in the U.S. government's sovereign credit

rating, or in the credit ratings of instruments issued, insured or guaranteed by related institutions, agencies or instrumentalities,

could result in risks to us and general economic conditions that we are not able to predict; the failure of the European Union

to stabilize the fiscal condition and creditworthiness of its weaker member economies, such as Greece, Portugal, Spain,

Hungary, Ireland, and Italy, could have international implications potentially impacting global financial institutions, the

financial markets, and the economic recovery underway in the U.S.; weakness in the real estate market, including the secondary

residential mortgage loan markets, has adversely affected us and may continue to adversely affect us; we are subject to certain

risks related to originating and selling mortgages, and may be required to repurchase mortgage loans or indemnify mortgage

loan purchasers as a result of breaches of representations and warranties, borrower fraud, or as a result of certain breaches of

our servicing agreements, and this could harm our liquidity, results of operations, and financial condition; financial difficulties

or credit downgrades of mortgage and bond insurers may adversely affect our servicing and investment portfolios; we may

be terminated as a servicer or master servicer, be required to repurchase a mortgage loan or reimburse investors for credit

losses on a mortgage loan, or incur costs, liabilities, fines and other sanctions if we fail to satisfy our servicing obligations,

including our obligations with respect to mortgage loan foreclosure actions; we are subject to risks related to delays in the

foreclosure process; we may continue to suffer increased losses in our loan portfolio despite enhancement of our underwriting

policies and practices; our mortgage production and servicing revenue can be volatile; as a financial services company, adverse

changes in general business or economic conditions could have a material adverse effect on our financial condition and results

of operations; changes in market interest rates or capital markets could adversely affect our revenue and expense, the value

of assets and obligations, and the availability and cost of capital and liquidity; changes in interest rates could also reduce the

value of our MSRs and mortgages held for sale, reducing our earnings; the fiscal and monetary policies of the federal

government and its agencies could have a material adverse effect on our earnings; depressed market values for our stock may

require us to write down goodwill; clients could pursue alternatives to bank deposits, causing us to lose a relatively inexpensive

source of funding; consumers may decide not to use banks to complete their financial transactions, which could affect net

income; we have businesses other than banking which subject us to a variety of risks; hurricanes and other disasters may