SunTrust 2011 Annual Report Download - page 137

Download and view the complete annual report

Please find page 137 of the 2011 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

|

|

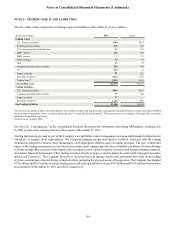

Notes to Consolidated Financial Statements (Continued)

121

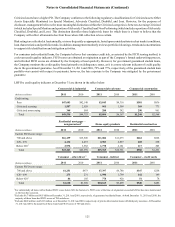

Criticized assets have a higher PD. The Company conforms to the following regulatory classifications for Criticized assets: Other

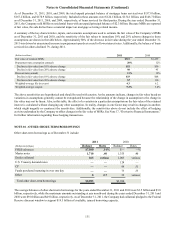

Assets Especially Mentioned (or Special Mention), Adversely Classified, Doubtful, and Loss. However, for the purposes of

disclosure, management believes the most meaningful distinction within the Criticized categories is between Accruing Criticized

(which includes Special Mention and a portion of Adversely Classified) and Non-Performing (which includes a portion of Adversely

Classified, Doubtful, and Loss). This distinction identifies those higher risk loans for which there is a basis to believe that the

Company will collect all amounts due from those where full collection is less certain.

Risk ratings are refreshed at least annually, or more frequently as appropriate, based upon considerations such as market conditions,

loan characteristics and portfolio trends. In addition, management routinely reviews portfolio risk ratings, trends and concentrations

to support risk identification and mitigation activities.

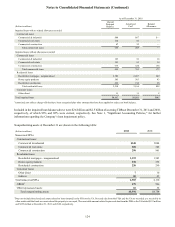

For consumer and residential loans, the Company believes that consumer credit risk, as assessed by the FICO scoring method, is

a relevant credit quality indicator. FICO scores are obtained at origination as part of the Company’s formal underwriting process,

and refreshed FICO scores are obtained by the Company at least quarterly. However, for government guaranteed student loans,

the Company monitors the credit quality based primarily on delinquency status, as it is a more relevant indicator of credit quality

due to the government guarantee. As of December 31, 2011 and 2010, 79% and 77%, respectively, of the guaranteed student loan

portfolio was current with respect to payments; however, the loss exposure to the Company was mitigated by the government

guarantee.

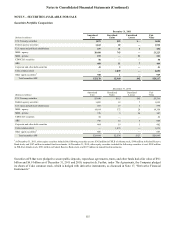

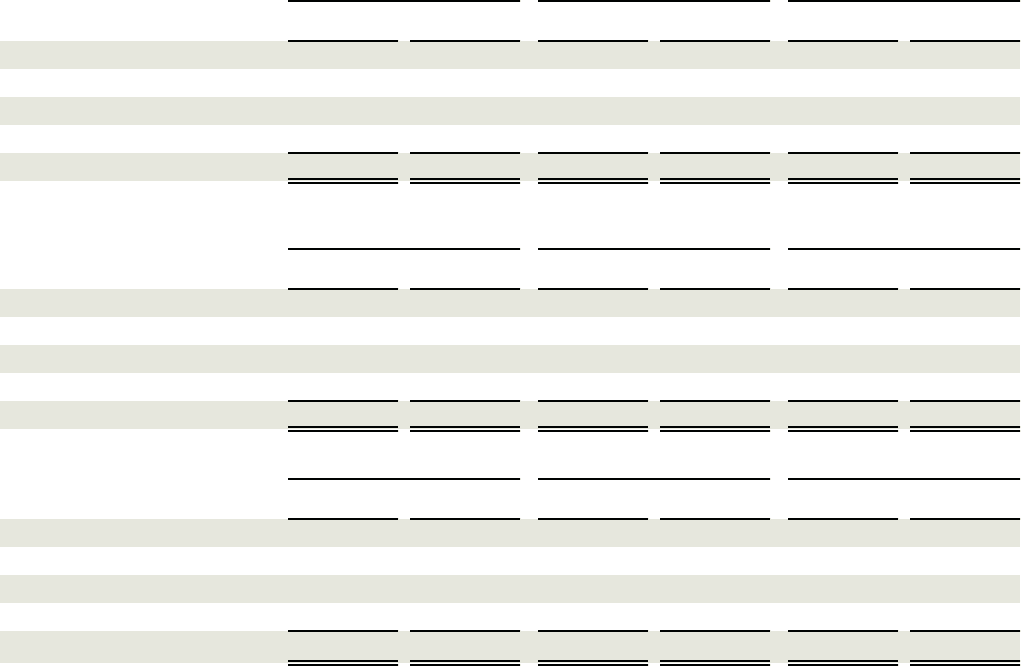

LHFI by credit quality indicator at December 31 are shown in the tables below:

(Dollars in millions)

Credit rating:

Pass

Criticized accruing

Criticized nonaccruing

Total

Commercial & industrial

2011

$47,683

1,507

348

$49,538

2010

$42,140

2,029

584

$44,753

Commercial real estate

2011

$3,845

961

288

$5,094

2010

$4,316

1,509

342

$6,167

Commercial construction

2011

$581

369

290

$1,240

2010

$836

771

961

$2,568

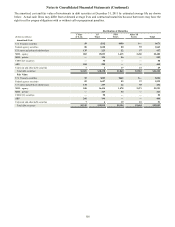

(Dollars in millions)

Current FICO score range:

700 and above

620 - 699

Below 6201

Total

Residential mortgages -

nonguaranteed 2

2011

$16,139

4,132

2,972

$23,243

2010

$15,920

4,457

3,582

$23,959

Home equity products

2011

$11,084

2,903

1,778

$15,765

2010

$11,673

2,897

2,181

$16,751

Residential construction

2011

$661

202

117

$980

2010

$828

258

205

$1,291

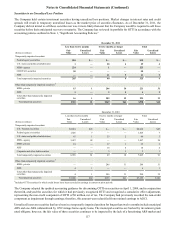

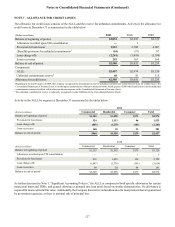

(Dollars in millions)

Current FICO score range:

700 and above

620 - 699

Below 6201

Total

Consumer - other direct 3

2011

$1,251

273

86

$1,610

2010

$973

231

105

$1,309

Consumer - indirect

2011

$7,397

1,990

778

$10,165

2010

$6,780

1,799

920

$9,499

Consumer - credit cards

2011

$347

142

51

$540

2010

$258

149

78

$485

1For substantially all loans with refreshed FICO scores below 620, the borrower’s FICO score at the time of origination exceeded 620 but has since deteriorated

as the loan has seasoned.

2Excludes $6.7 billion and $4.5 billion at December 31, 2011 and 2010, respectively, of guaranteed residential loans. At both December 31, 2011 and 2010, the

majority of these loans had FICO scores of 700 and above.

3Excludes $449 million and $413 million as of December 31, 2011 and 2010, respectively, of private-label student loans with third party insurance. At December

31, 2011 and 2010, the majority of these loans had FICO scores of 700 and above.